This week, WPP ScanGroup, some would say East Africa’s leading integrated marketing communications group, and the regional arm of global advertising giant WPP, announced its 2025 full-year results.

The Group reported yet another year of deepening losses and raising fresh questions about the pace and credibility of its turnaround.

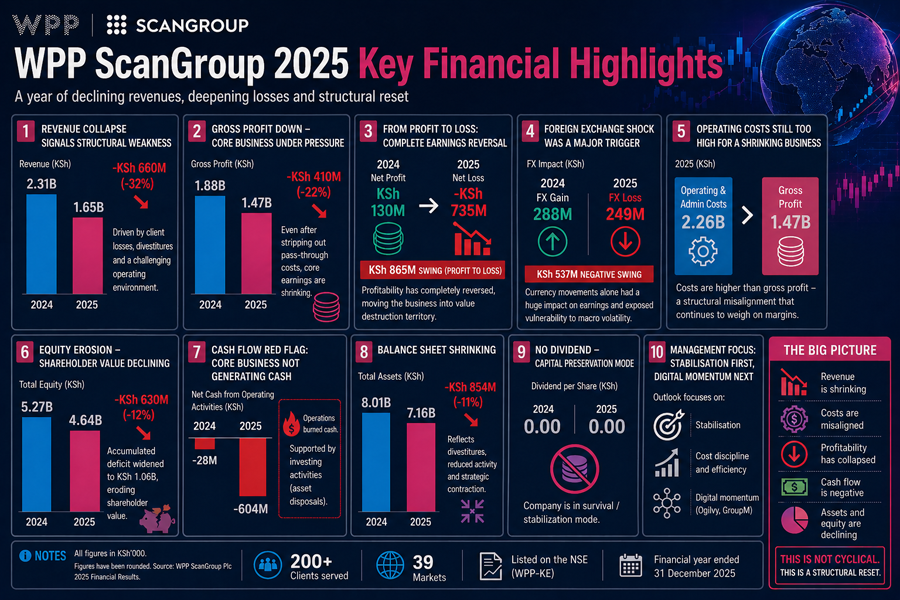

For the year ended December 2025, the Group posted a net loss of approximately KSh735 million (UGX 20.6 billion), widening from the KSh 507 million (UGX 14.2 billion) in 2024 and marking a sharp reversal from the KSh 130 million (UGX 3.6 billion) profit in 2023.

In just two years, ScanGroup has now accumulated losses exceeding KSh 1.2 billion (UGX 33.6 billion), underscoring the scale of the earnings erosion confronting management.

The deterioration is even more pronounced at the revenue level. Group turnover fell to about KSh 1.65 billion (UGX 46.2 billion) in 2025, down from KSh 2.44 billion (UGX 68.3 billion) in 2024, representing a steep 32% year-on-year decline.

Gross profit followed the same downward trajectory, dropping from KSh 2.01 billion (UGX 56.3 billion) to approximately KSh 1.47 billion (UGX 41.2 billion), reflecting weaker client activity and declining billings across key markets.

At the heart of this collapse is a combination of client attrition, structural industry shifts, and intensifying competition, forces that are converging at speed.

The most visible trigger has been the loss of major accounts. The exit of Airtel Africa, which accounted for nearly 20% of ScanGroup’s revenues, was a defining blow.

But it has not been an isolated case. Other key clients, including Isuzu and KCB, have also moved on, signalling not just episodic churn, but a broader reallocation of market share.

Shrinking revenues, lost clients, rising pressure

The loss of these accounts tells a deeper story about the changing nature of the industry. Clients are no longer tied to legacy agency relationships as they once were. Instead, they are increasingly seeking speed, flexibility, and measurable value, often at a lower cost.

And they are finding it elsewhere. A growing number of mandates are shifting toward smaller, more agile agencies, leaner teams that are willing to do more for less, unburdened by the cost structures of large networks.

In many cases, these firms are entering pitches aggressively, offering more output for lower fees, and forcing incumbents into a race to defend margins.

At the same time, the rapid rise of AI-driven marketing tools is further levelling the playing field.

Campaign development, content production, and performance optimisation, once the preserve of large agencies with scale, are now increasingly automated, faster, and more cost-efficient.

As Miriam Kaggwa, WPP ScanGroup’s chief operating officer and former interim Group CEO, told the CEO East Africa Magazine in a July 2025 interview, the industry is undergoing a fundamental shift in both capability and pricing dynamics.

Agencies are being pushed to deliver more for less, with discounts of up to 25% year-on-year becoming part of the competitive reality. Meanwhile, client budgets are steadily shifting toward digital and data-led channels, away from traditional media models. The result is a market where scale alone is no longer a competitive advantage.

A rival born from within

But perhaps the most immediate and strategic threat facing ScanGroup is not just external, it is internalised.

The emergence of The Partnership Africa (TPA), a fast-growing, pan-African agency with operations in Nairobi, Lagos, and Kampala, has introduced a new and more sophisticated layer of competition.

Founded by former WPP-Scanad executives Sandeep Madan, Deepesh Jha, and Sally Sawe, the firm is built on deep insider knowledge of the very system it now seeks to disrupt.

At the time of its formation, the trio held senior, client-facing leadership roles across key WPP agencies, including Scanad Africa and J. Walter Thompson Kenya, giving them intimate access to client relationships, institutional knowledge, and long-standing account equity.

Lean, agile, and designed for a digital-first, cost-sensitive market, TPA has quickly positioned itself as a credible alternative for major clients. It understands the pricing structures, the operational complexities, and, critically, the client expectations that define ScanGroup’s core business.

The shift of the Airtel Africa account to this breakaway network was more than a commercial loss; it marked a transfer of trust, capability, and strategic alignment.

It also opened the floodgates. With KCB and Isuzu now among the clients that have moved to TPA, the trend is becoming clear: this is not isolated churn, but a systematic reallocation of key accounts.

And Airtel may only be the beginning. With deep client relationships and a model built for speed and efficiency, TPA and firms like it are well-positioned to compete for, and win, more mandates from the same pool of multinational and regional clients.

Leadership in transition

It is into this environment that Akua Owusu-Nartey stepped in as Group CEO in November 2025, following a period of leadership transition that saw the exit of Patricia Ithau earlier in the year.

Owusu-Nartey brought over 18 years of experience in integrated marketing, brand transformation, and pan-African business leadership, much of it within the WPP ecosystem.

She had held senior roles across multiple markets, led complex client portfolios, and built a reputation for revitalising underperforming operations and driving integration across fragmented structures.

Her track record includes leading the integration of agency operations in West Africa and managing cross-market teams in highly competitive environments, experience that now becomes critical as she takes on one of the toughest assignments in the region’s advertising industry.

Yet, the scale of the challenge she faces is arguably greater than anything before. Despite its current struggles, ScanGroup remains a formidable platform.

The company still serves over 200 clients across 39 markets, retains strong positions in Kenya, Ghana, and Uganda, and continues to benefit from the global backing of WPP.

But the market it once dominated has fundamentally changed.

A structural reset, not a cyclical dip

For Owusu-Nartey, the task ahead is clear and unforgiving. She inherited a business with deep institutional strengths, scale, talent, and global backing, but one that must now reinvent itself in a fragmented, digital-first, and relentlessly price-driven market.

Yet, if there is a leader built for this moment, it is one forged in integration, client leadership, and turnaround execution.

From unifying operations in Ghana to managing complex, multi-market client portfolios across Africa, Owusu-Nartey has built a reputation for stepping into underperforming environments and restoring coherence, discipline, and growth.

That experience will now be tested at scale. The path forward will hinge on rebuilding a revenue base shaken by major client exits, re-anchoring the business around high-value, integrated offerings, and accelerating the shift toward digital and data-led solutions.

At the same time, she must impose cost discipline on a structure that has struggled to align expenses with shrinking income.

But more than strategy, this moment demands execution, fast, precise, and sustained.

Because for WPP ScanGroup, this is no longer just a downturn. It is a structural reset.

And in the hot seat, Owusu-Nartey is not just expected to steady the ship; she is expected to redesign it, reposition it, and return it to profitable growth.

The market is no longer waiting for intent. It is waiting for results.