Uganda is paying heavily to keep cash alive.

Every year, trillions of shillings are absorbed into an economy still built around physical currency through the systems that print, transport, secure, store, and replace notes and coins.

Bank of Uganda spent UGX 212.6 billion managing currency in 2025, up from UGX 203.1 billion the previous year.

Beneath that 4.7% increase lies a deeper story about how Ugandans use money and the growing cost of keeping cash alive.

At the centre of it all is note printing, which surged by more than 11% to UGX 193.8 billion, accounting for more than 90% of total currency management costs.

The spike suggests sustained demand for physical cash despite years of digital financial expansion. Whether driven by population growth, inflation, or the continued dominance of informal transactions, cash remains king.

That reality also helps explain why the debate over taxing withdrawals has become so contentious.

The Ministry of Finance recently dropped plans to tax all cash withdrawals after pushback from stakeholders.

The proposed 0.25% levy had been framed as a way to boost revenue and support a cashless economy. For now, the idea is shelved, though not entirely off the table, according to Finance Ministry Permanent Secretary Ramathan Ggoobi.

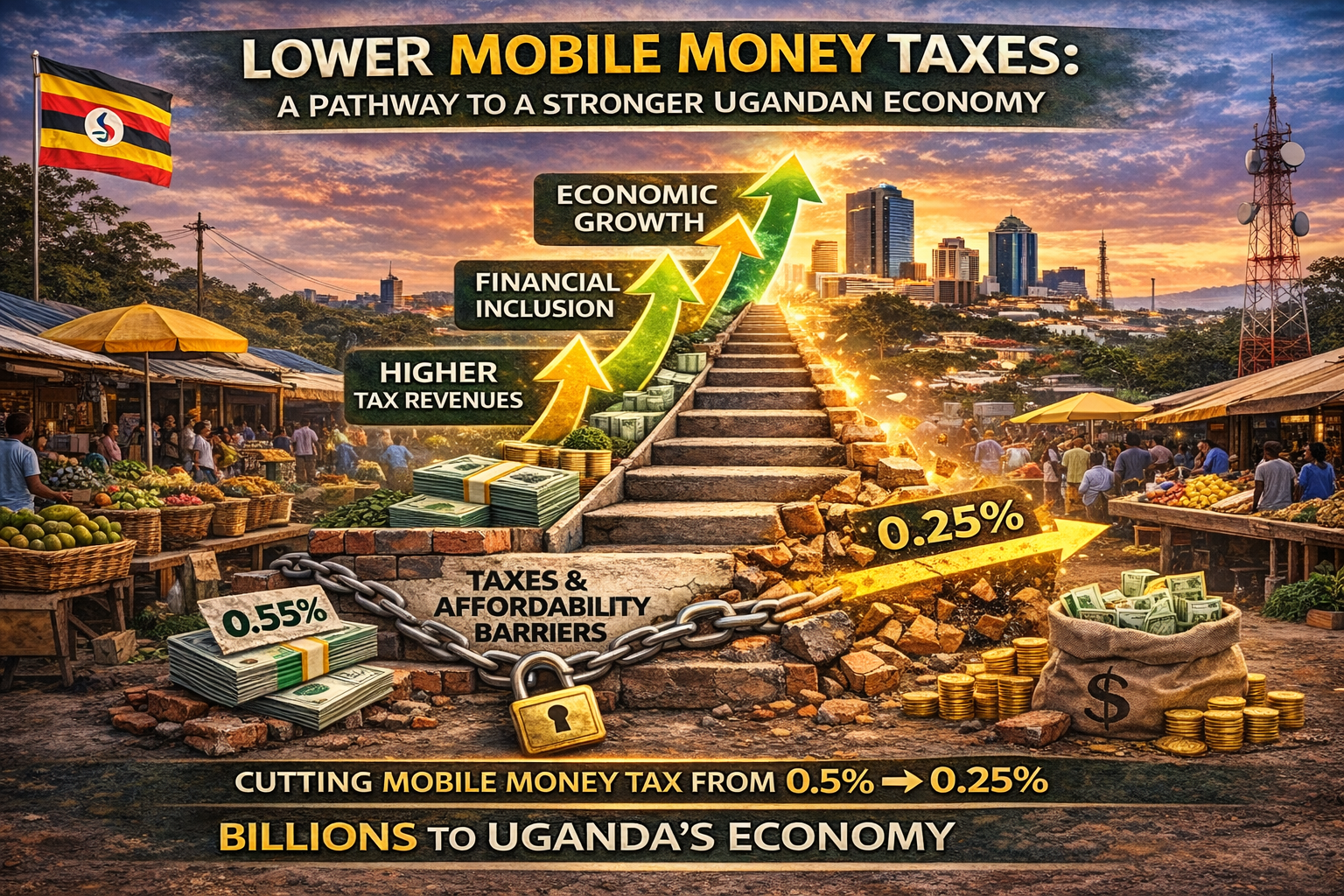

Even so, the wider argument has not disappeared. The real policy question is no longer whether mobile money should carry a 0.5% tax on withdrawals. It is whether reducing that burden to 0.25%, while broadening it across the entire financial system, could become a more workable step in the right direction.

That is where the debate has sharpened: not around whether government needs revenue, but around how to raise it without slowing the digital transition it says it wants to accelerate.

At the same time, Uganda is taxing one of the most viable alternatives to cash: mobile money.

That is the contradiction at the centre of the country’s financial architecture. On one side is a cash economy that is expensive to sustain. On the other is a digital financial ecosystem that has already transformed how money moves across the country, but whose growth and efficiency are being constrained by policy choices that raise the cost of using it.

Mobile money sits at the centre of that question.

Over the past decade, it has transformed how Ugandans send, receive, store, and use money. It has reduced the need for physical travel, enabled instant transfers, and expanded financial access far beyond the reach of traditional banking infrastructure. It has also built one of the most extensive financial networks in the country.

MTN Uganda says its mobile money agent network has grown by 156%, from 94,000 in 2019 to 241,000 in 2025, while active customers rose from 7.4 million to 14.6 million over the same period.

Julius Mukunda, Executive Director of CSBAG, reinforces the point from the inclusion point of view.

The 2023 FinScope survey shows that 64% of adults use mobile money, while only 14% use banks, and mobile money’s reach extends into villages that banks do not serve.

Bank of Uganda data show how quickly the wider ecosystem is expanding. By June 30, 2025, 18 licensed entities were operating as e-money issuers, including MTN Mobile Money, Airtel Mobile Commerce, Stanbic Bank’s Flexipay, PostBank, and several other providers.

Together, they had enlisted 1,016,914 agents, up 27% from 775,294 a year earlier.

Over the same period, the value of electronic money transactions rose by 28.6%, from UGX 253.7 trillion to UGX 326.3 trillion, while volumes increased by 20.6%, from 7 billion to 8.4 billion transactions.

That is not just growth in usage. Electronic money is becoming more embedded in business transactions and everyday commerce across the economy.

That broader structural point is also echoed by Trevor Lukanga, Associate Director at PwC Uganda.

In his view, Uganda’s ambition to build a cashless, digitally inclusive economy could be undermined by the very tax policies designed to raise revenue.

His warning goes to the heart of the debate: if the country wants digital adoption at scale, it cannot keep making the most widely used digital rail more expensive at the point where ordinary users actually feel the cost.

The International Growth Centre’s 2025 report, Financial Inclusion versus Financial Development: Evidence Using Transaction-Level Data – The Case of Uganda, backs up that concern with unusually detailed behavioural evidence from Uganda’s 2018 tax episode.

Using transaction-level data, the report shows that when the cost of mobile money rose, user behaviour shifted quickly and persistently away from digital channels.

With that scale in mind, the economics become much clearer. Cash-based systems require physical infrastructure at every stage. Branches, ATMs, cash-handling facilities, transport logistics, and security systems all come at a cost.

Every transaction involving physical cash carries a hidden expense. Digital systems operate differently.

Once the infrastructure is in place, the marginal cost of transactions falls sharply. Transfers happen without physical movement. Value can stay within the system. Efficiency increases.

That is where the potential savings emerge. Reducing reliance on cash can lower the cost of printing currency, shorten the replacement cycle of worn notes and coins, and reduce the logistical burden of distributing and managing cash across the country.

Uthman Mayanja, PwC Country Senior Partner, made the same point in broader policy terms in an interview published in Daily Monitor.

Mobile money, he said, has become a major vehicle for financial inclusion, but high transaction costs and taxes continue to limit how fully it can serve as an affordable financial lifeline.

How the tax changed behaviour

But that transition is not automatic. It depends on usage, and usage is influenced by cost.

Uganda’s mobile money tax structure is central to the story. As the IGC report recounts, the July 2018 tax was initially imposed at 1% on all mobile money transactions, including deposits, withdrawals, and transfers, before public backlash forced a revision to 0.5% on withdrawals only.

Even after that retreat, the report finds that the policy introduced lasting uncertainty and friction into a system that had become central to household finance.

That is why the 0.25% discussion matters. On the surface, reducing the mobile money withdrawal tax from 0.5% to 0.25% appears to offer relief to users who have long faced higher charges.

As a narrow correction to an already distortionary tax, it can be read as a step in the right direction.

But once the same rate is extended across the broader financial system, the question changes. The issue is no longer simply whether government is easing pressure on mobile money users.

It becomes whether a lower rate, applied more widely, solves the underlying distortion or simply redistributes it.

Government’s proposal to introduce a 0.25% tax on cash withdrawals appeared to be driven primarily by revenue mobilisation, with a target of raising roughly UGX 250 billion, while also presenting the measure as more equitable by spreading the burden across the broader financial sector, including digital transactions.

Lukanga reflects on that history in similarly direct terms: Uganda’s tax structure for the digital economy still lags behind countries like Kenya and Tanzania. His point is not simply that the tax exists, but that the way it is structured leaves Uganda out of step with regional peers that have been more deliberate about supporting digital adoption.

MTN’s submission makes the burden especially concrete. A Ugandan withdrawing UGX 500,000 pays UGX 2,500 in excise duty on the transaction value alone, on top of 15% tax on the service fee.

CSBAG pushes that comparison even further. Its position paper notes that withdrawing UGX 1 million attracts just UGX 315 in tax on bank or ATM fees, but UGX 6,630 in total tax on a mobile money withdrawal.

That means the mobile money user pays about 21 times more tax for accessing the same amount of their own money.

That is not a minor distortion. It is a structural tax penalty on the channel used most by low-income and rural Ugandans.

CSBAG’s central argument is not only that the tax is high, but that it is regressive. Mobile money users, the paper argues, most of whom are low-income earners, bear the heavier burden, while bank withdrawals are taxed only through VAT on bank fees.

CSBAG, therefore, describes the current framework as economically inefficient, socially regressive, and inconsistent with regional practice.

Thus, Julius Mukunda argues that government must stop treating mobile money “as a cash cow” and instead see it as part of the country’s economic bloodstream.

Emmanuel Ssemugenyi, Tax Partner at Pizca Consult Company and a lecturer at Kyambogo University, adds another caution.

In his view, reducing the mobile money withdrawal tax to 0.25% may relieve users who have long carried the heavier burden.

However, applying that same rate across the entire financial system could make formal financial transactions more expensive overall and push some Ugandans back toward informal methods of storing and moving money, including cash hoarding.

That, he argues, would run directly against the stated goal of financial inclusion.

While relatively small in percentage terms, this tax affects user behaviour, with the IGC data showing the effect is measurable and immediate.

In the period after the tax shock, the report found that users held lower balances in mobile money wallets and that activity weakened in ways that were visible in transaction data.

MTN’s own historical series points in the same direction. Cash withdrawal transaction values grew from UGX 9.86 trillion in 2015/16 to UGX 12.99 trillion in 2017/18, then stalled at UGX 12.04 trillion in 2018/19, the period when the excise duty on transaction volumes was introduced, first at 1%, then revised to 0.5% after public backlash.

The market later recovered, but MTN argues that the levy continues to act as a drag on what could otherwise have been faster expansion.

By June 2024/25, withdrawal values had risen to UGX 29 trillion, generating UGX 145 billion in excise collections at the 0.5%.

CSBAG places that behavioural response in a wider welfare frame. Its paper points to Uganda’s 2018 tax experience as a warning, citing a 40% drop in mobile money usage after the tax changes and arguing that for every 10% increase in price, usage falls by 20%.

It also cites IMF analysis suggesting the tax creates 33 to 35% economic waste, meaning the economic damage exceeds the fiscal gain.

Whether one uses the language of elasticity, deadweight loss, or welfare loss, the implication is the same: a tax on a price-sensitive platform can destroy more value than it raises.

Lukanga’s analysis lands in the same place from a policy angle. If you impose a charge on withdrawals, he argues, you are not incentivising usage; you are punishing people who are already using digital platforms.

A government that says it wants inclusion is taxing one of the very behaviours it says it wants to scale.

Ssemugenyi pushes the argument further into macroeconomic territory. He warns that taxing transactions rather than income or profits can have wider economic consequences because it reduces liquidity, dampens spending and investment, and can ultimately slow growth.

His concern is that once transaction volumes fall, profitability across banks, telecoms, and agent banking networks can also come under pressure, with consequences for income tax collections as well as sector growth and innovation.

The tax creates an incentive to withdraw cash less frequently but in larger amounts, or to exit the digital system entirely where possible.

In effect, it pulls value out of the digital ecosystem. That has broader implications. When money remains within the digital system, it circulates more efficiently.

25% Profit Growth, 46% Deposit Surge, 29% Asset Expansion: Inside David Wandera’s Breakout Year at Absa Uganda

25% Profit Growth, 46% Deposit Surge, 29% Asset Expansion: Inside David Wandera’s Breakout Year at Absa UgandaTransactions can be tracked, services can be layered, and economic activity becomes more visible. When money is withdrawn into cash, that visibility is reduced. The efficiency gains of digitisation are partially lost.

Lukanga points to the friction in simple, everyday terms: if someone sends UGX 100,000, the recipient receives less. A digital system cannot deepen trust and convenience if the value transferred is visibly eroded at the point of use.

Stephen Obeli, proprietor of Kweli.Shop, makes a related argument from the merchant’s point of view. In his view, current efforts to push Uganda toward a digital economy risk backfiring because they increase the cost of doing business without making digital alternatives more efficient.

The problem is not only the tax itself. It is the wider transaction environment in which every digital step seems to introduce another deduction, delay, or operational complication.

CSBAG makes the same point more politically and socially. It argues that the tax directly hits essential household spending, including healthcare, food, transport, and school fees, because mobile money is the primary service people use where banks are distant or administratively inaccessible.

Its proposed reform, therefore, goes beyond a simple rate cut. It calls for reducing the withdrawal tax from 0.5% to 0.25%, introducing a maximum cap of UGX 5,000 per transaction, exempting small withdrawals of UGX 20,000 and below, and, over time, shifting taxation away from the value withdrawn and toward transaction fees only.

That matters because it grounds the reform debate not just in macroeconomics, but in how ordinary people actually use money day-to-day.

Ssemugenyi’s concern fits directly into that same inclusion question. One mitigation, he suggests, would be a minimum threshold so that transactions below UGX 10,000 are exempted, protecting low-income earners and small-scale users.

Without that kind of design feature, a broader tax may end up looking more even on paper than it feels in practice.

That is why this debate cannot be reduced to a revenue line in the budget. It is about whether policy is reinforcing the country’s most scalable financial rails or weakening them at the point where users convert digital value into everyday utility.

What replaced mobile money, and why that matters

The immediate issue is not only that mobile money usage fell. It is also what replaced it.

The IGC report shows clear substitution away from mobile money and toward banks, banking agents, and cash.

That substitution was not evenly distributed. It was stronger in areas that already had better physical and financial infrastructure. In practice, once costs rose on digital channels, some users did not stop moving money. They simply moved it differently.

This is where the hidden cost of cash becomes more visible.

When users move from mobile money to banking agents and then to ATM withdrawals, Uganda is not simply changing channels. It is reintroducing physical cash into the payment chain. And that reintroduction brings back the very costs digital systems are supposed to reduce.

The policy problem, then, is not simply that digital services are being taxed. It is that a tax placed at a critical friction point, withdrawals, can distort the entire direction of system evolution.

The IGC report calls Uganda’s experience a warning about how even small frictions can trigger large and persistent behavioural change when they affect essential transactions.

It also notes that mobile money’s comparative advantage rested on three pillars: low transaction costs, high geographic reach through agents, and minimal onboarding friction. By taxing withdrawals, the policy weakened exactly those pillars.

Lukanga’s concern about the cash question sits directly inside that dilemma. People still need cash in Uganda today, he argues. The real question is whether government should discourage cash by taxing people who are already using digital platforms, or instead incentivise those who are already in the cashless system.

His position is firm: it is easier to support those who have already transitioned than to frustrate them.

Obeli reaches a similar conclusion from the business side. He argues for a more holistic policy approach, one focused not only on taxes but also on reducing transaction costs, improving the speed and reliability of transfers, and strengthening interoperability across payment systems.

Ssemugenyi’s warning runs parallel, but at the level of system design and state oversight. A tax designed to broaden revenue collection may end up weakening the very transaction trail that makes digital finance valuable to policymakers in the first place.

CSBAG adds an important comparative layer here, noting that Uganda is the only East African country taxing mobile money withdrawals in this way, while neighbouring countries generally tax fees rather than the full value withdrawn.

That means Uganda is imposing a heavier tax at exactly the point where users leave digital rails and re-enter cash, even though national policy says it wants the opposite outcome: more digital usage and less cash dependence.

The case for lower taxes and a bigger digital economy

This is where the proposal to reduce the withdrawal tax from 0.5% to 0.25% becomes relevant.

The argument is not simply about reducing costs for users. It is about changing incentives.

Lowering the tax could encourage more transactions to remain within the digital system. It could increase transaction volumes, expand usage, and support a shift away from cash.

Over time, this could lead to greater efficiency and potentially higher overall tax revenue through increased economic activity. It is a shift from taxing transactions to enabling them.

MTN’s paper makes a parallel argument in explicitly fiscal terms. It argues that excise duties work best on goods with relatively inelastic demand, such as alcohol, tobacco, and fuel, where consumption does not fall sharply as prices rise.

Mobile money is different. It is price-sensitive, especially among lower-income users. Higher costs mean fewer transactions, more cash usage, and more workarounds. In that sense, the tax does not simply collect from an existing base. It can also shrink the base it is trying to tax.

CSBAG pushes that same point from a public-finance angle. Its presentation argues that government’s need for revenue is understandable, especially in a period of wider deficits, but that the current tax design reflects a short-term focus on revenue extraction rather than a long-term strategy to expand the tax base.

It cites wider digital-economy modelling showing that modest tax reductions today can generate larger fiscal returns over time through higher adoption, job creation, and broader taxable activity.

Lukanga reaches a similar conclusion from the perspective of tax design. Rather than taxing the value of transactions, he argues, Uganda should tax the fees. Taxing usage less aggressively allows the system to grow.

Ssemugenyi’s view complicates the current reform proposal significantly. He is not arguing for higher taxes. He is arguing that spreading a 0.25% levy across the wider financial system may still suppress the multiplier effect of transactions that government should be trying to encourage.

In his words, taxing 0.25% on the value of cash withdrawals is like “eating your egg before it hatches.”

The warning is that government may be tempted by an immediate UGX 250 billion target, yet lose more over time through lower transaction volumes, lower profitability in financial institutions, and weaker income tax performance.

This is the basis of the argument for reform.

It is not guaranteed. It depends on how strongly users respond to lower costs. But the Ugandan evidence already shows the direction of response when costs rise: usage falls, balances decline, banks and cash absorb displaced value, and rural users are left with fewer workable substitutes.

That is not a neutral fiscal intervention. It is a structural reallocation of financial behaviour.

There is also a broader fiscal consideration. The cost of maintaining a cash-based system is not eliminated by taxing digital alternatives. If anything, it may be prolonged.

A slower transition to digital payments means continued reliance on cash, with all its associated costs. A faster transition could reduce those costs over time.

This is the trade-off: short-term revenue from taxes on digital transactions versus long-term efficiency gains and broader economic growth. Uganda’s policy choices will determine how that balance is struck.

MTN’s projections are designed to show what reform could look like under a lower-rate regime.

It projects that cash withdrawal transactions would rise from UGX 31.96 trillion in 2025/26 to UGX 63.39 trillion by 2029/30, nearly doubling in five years.

Over the same period, projected collections from a 0.25% excise duty would rise from UGX 80 billion to UGX 158 billion as transaction volumes expand.

It also projects that its mobile money customer base could grow to 24.2 million by 2030 and its agent network to 424,000. A larger customer base and denser agent network would not only raise direct transaction activity.

They would also make the platform more useful, more convenient, and more deeply embedded in the economy.

CSBAG’s own fiscal estimates move in the same direction. Its table projects transactions rising from UGX 31.96 trillion in 2026 to UGX 63.39 trillion in 2030 under a lower-rate regime, while expected government gains from expanded activity rise from UGX 119 billion to UGX 238 billion over the period.

It explicitly argues that the short-term loss can be offset in the medium term by volume growth and ecosystem expansion.

MTN’s trade-off table lays out the broader logic directly. In the short term, excise collections fall. But in the medium term, the company argues those losses are offset by volume growth, increased VAT on services, stronger corporate tax from ecosystem expansion, and broader digitally enabled business activity.

It presents its own tax record as evidence of that larger ecosystem effect: UGX 6.177 trillion in total taxes between 2015 and 2024, averaging UGX 618 billion annually, with corporate income tax rising from UGX 103.5 billion in 2015 to UGX 268.9 billion in 2024.

Lukanga makes that same case in even starker terms. The 0.5% that policymakers are so concerned about, he argues, can easily be made up by increased volumes. The more people use mobile money, the easier it becomes to collect revenue from larger players like MTN and Airtel.

That also lowers the cost of tax collection because the burden shifts toward large, organised service providers rather than individual users. There is, in that sense, a state-capacity argument for reform as well as an efficiency one.

Lukanga points to Kenya as the clearest case study in what happens when policy and platform growth reinforce each other.

He cites estimates from a London School of Economics study suggesting that Kenya processes close to 59% of its GDP through M-PESA. The implication is simple: scale becomes possible when people can use the platform easily and affordably.

Ssemugenyi, however, argues that long-term transition requires more than redesigning the levy. If government wants a genuine shift toward a cashless economy, taxation must be paired with deliberate incentives.

That includes smartphone financing schemes to expand access to digital devices, as well as targeted incentives such as tax holidays to encourage local smartphone assembly.

He points to Ethiopia as an example where state-backed device financing has helped accelerate digital adoption and support a cashless economy.

His broader point is that taxation cannot do the work of digital transformation on its own. It must be matched by policies that lower the real barriers to participation.

There is, however, a contrasting view from within the financial sector itself. A banker who spoke on condition of anonymity argues that a 0.25% tax would encourage digital payments, especially for the informal sector, which remains heavily cash-based.

That suggests some in the sector see the lower rate, even if broadened, as a workable compromise between revenue collection and behavioural nudging.

For Lukanga, the strategic choice is now unavoidable. Uganda must decide whether it wants to be seen as frustrating digital financial services or incentivising them.

He acknowledges government’s need to raise revenue, but insists that it should not come at the expense of long-term transformation.

Yes, there is a need to collect revenue, he says, but it should not compromise the strategy of digitising the economy and ensuring financial inclusion.