Across Africa, the banking hall is no longer the epicentre of financial services. It is the agent kiosk in a trading centre in Arua. The POS terminal inside a hardware shop in Mbarara. The small counter in Kalangala Islands, where deposits, withdrawals, utility payments, and tax transactions now happen daily.

In Uganda, the numbers tell the story.

As of June 30, 2025, at least 24 financial institutions, including 23 commercial banks and one microfinance deposit-taking institution, had joined the shared Agent Banking Platform, creating one of the region’s most interoperable last-mile financial ecosystems.

Growth has been dramatic. In a single year, transaction value surged by 76.1%, rising from UGX 16.7 trillion to UGX 29.4 trillion, while transaction volumes increased by 50.5%, from 8.3 million to 12.5 million.

Average transaction size grew by 17%, from UGX 2 million to UGX 2.35 million.

This illustrates that agent banking is no longer about small withdrawals. It is moving serious money.

At the same time, the physical network has expanded aggressively. Registered agents grew by 49.1% in one year, rising from 15,288 to 22,793 nationwide.

Yet beneath this expansion lies a more complex reality.

The active agent ratio declined from 58% to 48%, largely because thousands of new agents were onboarded faster than they could be fully activated and supported.

Growth is accelerating, but utilisation and supervision are struggling to keep pace.

The hidden risk of scale

Thousands of dispersed agents create visibility gaps. Agents relocate without notice. Machine handlers change. Registers are inconsistently maintained. Dormancy creeps in quietly. Fraud risks multiply. Compliance scrutiny intensifies.

All of this happens far from head offices where strategy is set, and risk committees sit.

The economics offer no room for inefficiency. Establishing a traditional branch can cost between UGX 300 million and UGX 500 million once infrastructure, systems, and staffing are factored in.

By contrast, deploying an agent terminal costs roughly UGX 1 million. The difference is structural, not incremental.

“Agent banking today is no longer optional for any serious bank,” says Ivan Kituuka, head of distribution and alternate channels at Housing Finance Bank.

Agent banking enables faster market penetration, lower fixed costs, longer operating hours, and proximity to underserved customers.

It is how rural deposits are mobilised, utilities are paid, and government funds reach remote communities.

But scale without structure is dangerous.

In a market where nearly UGX 30 trillion flows annually through agent networks, the question is no longer whether banks will scale; it is whether they can manage that scale.

The invisible infrastructure

While customers see kiosks and logos, a parallel system operates behind the scenes, mapping agents, supervising compliance, resolving operational breakdowns, geo-tagging locations, reducing dormancy, tracking handler changes, and transmitting real-time field intelligence back to banks.

That invisible infrastructure is Pebuu Africa, founded by serial entrepreneur John Paul Semyalo.

What began as a payments experiment has evolved into one of Africa’s most structured agent banking supervision ecosystems.

As digital finance accelerates across the continent, Pebuu is ensuring that last-mile expansion does not collapse under its own weight.

From a payments startup to a supervision engine

Pebuu did not begin as a supervision company.

Around 2014, Uganda was only beginning to experiment with online payments. Mobile money was gaining traction, but banks had not yet envisioned large-scale agent banking networks.

Semyalo, then working in advertising and public relations, attended an international payments expo. One small detail stayed with him.

“Every time a transaction went through, it made this catchy, rhythmic sound, something like ‘pay-boo’.”

The name lingered. It felt modern and forward-looking. Pebuu was born from that moment of technological curiosity.

The company built its own agent network, eventually reaching 2,400 agents nationwide.

Using a single Pebuu wallet and POS system, agents resold utilities, taxes, school fees, and other digital services in what was an ambitious attempt to create a unified payments layer.

Then Covid-19 disrupted the model.

Lockdowns shuttered shops. Working capital evaporated. Telecom operators accelerated direct-to-mobile services. Customer behaviour shifted almost overnight.

Revenue slowed, but one critical asset remained intact: infrastructure.

Pebuu had already built nationwide reach, deployed supervisors across districts, and developed digital reporting and geo-mapping tools long before banks fully appreciated how essential those systems would become.

Instead of retreating, Semyalo pivoted. “Instead of running our own agent network, we asked: What if we used this infrastructure to help banks manage theirs?”

2025: Finance Trust Bank posts 32% growth in deposits; 74% surge in net profit in strongest performance yet

2025: Finance Trust Bank posts 32% growth in deposits; 74% surge in net profit in strongest performance yetThat question reshaped the company. Pebuu transitioned from payment operator to supervision and last-mile channel management partner.

Scale in motion

Today, Pebuu supports leading institutions, including Stanbic Bank, Centenary, Housing Finance Bank, Absa, and others.

Every morning begins with field briefings. Targets are reviewed, escalations flagged, and reports assessed. Then, supervisors disperse by motorcycle into trading centres, border towns, mountain districts, and island communities.

In dense urban areas, multiple agents may be covered before midday. In regions such as Kalangala or Buvuma, a single visit can consume an entire day.

“We manage the banks’ agent networks through daily supervision,” says Elizabeth Atuhairwe, head of business support. “We assess compliance, check operational readiness, and offer on-the-spot support.”

That support is practical. Paper rolls are replenished. Applications are updated. Reversals are followed up on. Registers are delivered. Passwords reset. Complaints escalated.

“In essence, Pebuu acts as the eyes and ears of the bank on the ground,” she says.

Across Uganda, more than 300 field supervisors form one of the country’s most structured last-mile oversight networks. Each supervisor covers an average of 10 agents per day, depending on geography.

The impact is measurable. Pebuu has geo-mapped approximately 98% of supported agent locations. Compliance levels exceed 80% across supported networks.

Dormancy typically declines by between 10% and 20% within three months of structured supervision. Agent banking collections have grown by over 10% among major partner institutions.

To Kituuka, “supervision became an enabler of scale rather than a cost centre”.

Strengthening the human layer

Most agents operate banking as a complementary business alongside retail shops, hardware stores, or mobile money kiosks. Many earn between UGX 500,000 and UGX 1 million per month in commissions, while high performers generate between UGX 5 million and UGX 10 million.

Structured support often determines performance.

“Pebuu has helped us,” says agent banker Nantaba Harriet. “I no longer have to go to the bank for registers or resolve challenges alone. They fix issues quickly.”

Each month, Pebuu prints and distributes 30,000 training booklets, strengthening fraud awareness and compliance literacy.

“You’d be surprised how many agents could not identify a fake ID,” Semyalo admits.

Localisation underpins the model. Supervisors are recruited from the communities they serve.

“Local talent exists everywhere,” Semyalo says. “What they need is relevant training. Once you provide that, they deliver exceptional service.”

Strategic validation

For Housing Finance Bank, the partnership began with internal reflection. The bank had nearly 1,300 agents but recognised gaps in monitoring and compliance discipline.

“Agent supervision is not just operational; it is regulatory,” Kituuka explains.

Beyond compliance, structured supervision strengthens trust. Branding consistency, professional conduct, and visibility directly influence customer confidence.

Well-governed partnerships, he argues, are not outsourcing; they are capability extension. In modern banking, scale depends on collaboration as much as capital.

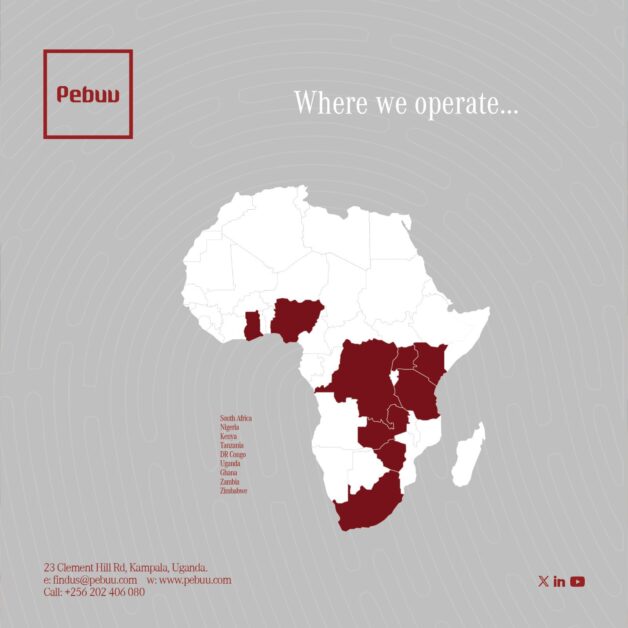

From Uganda to the continent

Pebuu has expanded into nine additional African markets: Nigeria, Ghana, DR Congo, Zimbabwe, Zambia, Tanzania, Kenya, Ethiopia, and South Africa.

In Nigeria, it works with Zenith Bank. In DRC, pilots are underway with Royal Bank. Regional institutions such as Stanbic and Absa extend the supervision model across borders.

“The dynamics are similar everywhere,” Semyalo says. “Head offices operate one way. Agents operate another. There’s always a gap. Pebuu becomes the bridge.”

The responsibility behind the model

“We employ more than 300 people,” Semyalo says. “If I drop the ball, the impact would be enormous.”

Behind every supervisor is a household. Behind every supported agent is a micro-enterprise funding families and school fees.

In some remote communities, a single rural agent can move over UGX 100 million a day, in places without branches, stable electricity, or reliable transport.

This is not merely about agent banking. It is about accountability at the last mile.

As trillions flow through distributed networks across Africa, Pebuu has positioned itself where visibility is weakest and risk is highest on the ground.

Motorcycle by motorcycle. Agent by agent. Market by market. Building not just networks, but trust.