As the clock ticks toward June, when the current term of Insurance Regulatory Authority (IRA) Chief Executive Officer Ibrahim Kaddunabbi Lubega is expected to expire, a quiet but palpable tension has begun to build across Uganda’s insurance industry.

There has been no public advertisement of the position, no formal communication outlining a succession plan, and no clear signal from either the Ministry of Finance or IRA itself.

In the absence of official guidance, attention has shifted to informal channels, where, according to multiple industry sources, discussions are intensifying and lobbying efforts are quietly underway.

What is unfolding is not merely a routine leadership transition. It is shaping into a moment of institutional significance, one that raises broader questions about governance, regulatory continuity, and the future direction of a sector that has grown steadily under Lubega’s watch.

A long tenure meets a legal question

Lubega has led IRA since 2010, making him one of the longest-serving heads of a regulatory authority in Uganda.

Over that period, he has become closely associated with the evolution of the insurance sector itself.

However, his extended tenure now intersects directly with the provisions of the Insurance Act, 2017, which stipulates a five-year term for the chief executive officer, renewable once.

In effect, the law provides for a maximum of 10 years in office. By the time his current term expires in June, Lubega will have served for over 15 years.

This places his tenure well beyond the statutory framework and raises a central question that is increasingly being asked within industry circles: whether IRA is preparing for a transition in leadership, or whether another extension, potentially amounting to a fourth term, could be considered.

The issue is not simply one of duration. It touches on the interpretation and application of the law, and whether institutional practice has kept pace with the legal framework introduced in 2017.

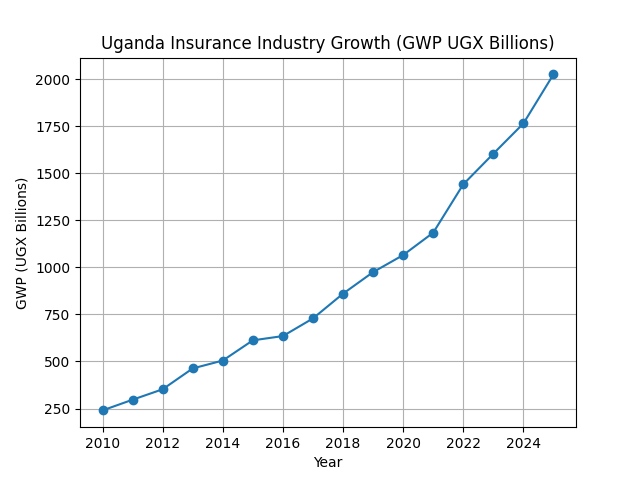

From UGX 240 billion to UGX 2 trillion: A defining era of growth

There is broad consensus within the industry that Lubega’s tenure has coincided with a period of significant growth and transformation.

In 2010, when he assumed office, Uganda’s insurance industry was valued at approximately UGX 240 billion.

By 2025, based on preliminary figures, the sector is projected to exceed UGX 2.02 trillion. This represents more than an eightfold expansion over 15 years, underpinned by consistent double-digit growth.

This growth has not been merely quantitative. Structurally, the industry has evolved in important ways. Distribution channels have expanded beyond traditional brokers to include agents, bancassurance, and increasingly digital platforms.

Life insurance, once a relatively small segment, has grown rapidly and now approaches parity with non-life business.

New areas such as microinsurance, agriculture insurance, and corporate health coverage have also emerged, reflecting a broader and more diversified market.

At the regulatory level, IRA itself has undergone significant development. The introduction of the Insurance Act, 2017 marked a shift toward a more robust legal and supervisory framework, supported by new regulations covering licensing, governance, reinsurance, mobile insurance, and capital adequacy.

Over time, IRA has moved toward more risk-based approaches to supervision, aligning with evolving global standards.

For many stakeholders, this continuity of leadership has contributed to stability in a sector that requires both technical expertise and regulatory consistency.

Stability vs governance: A growing tension

At the same time, the very longevity that some view as a strength is also the source of increasing scrutiny.

Advocates of Lubega’s continued stay in office argue that the insurance sector remains in a phase of development where institutional memory and regulatory continuity are valuable.

They point to the steady growth of the industry, the expansion of products and distribution channels, and the strengthening of oversight mechanisms as evidence of effective leadership.

However, others take a more governance-focused view. They argue that term limits exist to ensure renewal, prevent the concentration of authority, and reinforce the independence of public institutions.

In this perspective, the issue is not one of performance but of principle. The question is whether institutions should evolve beyond the individuals who lead them, particularly once they reach a certain level of maturity.

This tension between continuity and renewal now sits at the heart of the unfolding situation.

Legal ambiguity and institutional silence

Related

Uganda Airlines Restores Airbus A330-800neo to Service, Boosts Dubai Flights After Fleet Disruptions

Uganda Airlines Restores Airbus A330-800neo to Service, Boosts Dubai Flights After Fleet DisruptionsA key factor complicating the debate is the lack of public clarity regarding how Lubega’s tenure has been structured over time.

While the Insurance Act, 2017 sets out clear limits, it is not publicly evident how those provisions have been applied in practice, particularly in relation to a tenure that began prior to the Act’s enactment.

Within the industry, various explanations are discussed. These include the possibility that earlier contracts were renewed under previous legal frameworks, that transitional provisions following the 2017 Act may have affected term calculations, or that administrative extensions have been granted.

However, in the absence of official communication, these remain speculative. This lack of transparency has contributed to growing uncertainty.

IRA has been contacted for comment, but as of now, there has been no public clarification on the succession process or the legal basis for the current tenure.

A quiet but intense succession conversation

Behind the scenes, however, the conversation appears to be active. Industry sources indicate that there is increasing engagement around potential succession scenarios, with different stakeholders expressing varying preferences.

Some are said to favour continuity, citing the benefits of stability and experience. Others are advocating for a transition, emphasizing the importance of adherence to legal frameworks and the introduction of new leadership perspectives.

There are also indications that potential candidates, both from within IRA and from the broader financial sector, are being informally considered.

Yet without a formal process, such as a publicly advertised position or a clearly defined selection mechanism, the process remains largely opaque.

This combination of silence at the institutional level and activity behind the scenes has created an atmosphere of anticipation, with industry players closely watching for any signals that might indicate the direction being taken.

A broader test of institutional maturity

The situation at IRA reflects a broader question facing public institutions in Uganda: how to manage leadership transitions in a way that balances continuity with renewal.

Term limits are not simply procedural requirements; they are intended to support institutional resilience by ensuring that leadership changes occur in a predictable and transparent manner.

In regulatory bodies, where decisions can have significant implications for financial stability and market confidence, these considerations carry particular weight.

The way in which IRA navigates this moment may, therefore, be seen as a test of institutional maturity, not only for the Authority itself, but for the broader governance framework within which it operates.

Countdown to June

With June approaching, attention is now focused on what happens next. Three broad possibilities are being discussed within the industry.

One is that a new chief executive officer will be appointed, marking a clear transition in leadership.

Another is that Lubega’s tenure could be extended once again, raising further questions about the application of term limits.

A third possibility is an interim arrangement, in which the current leadership remains in place while a formal process is undertaken.

At this stage, none of these scenarios has been officially confirmed. The absence of clarity has only heightened the sense of anticipation, with stakeholders awaiting a definitive signal from the relevant authorities.

Legacy and the final chapter

After more than 15 years at the helm, Lubega’s contribution to the development of Uganda’s insurance industry is widely acknowledged.

He has overseen a period of sustained growth, guided the implementation of significant regulatory reforms, and played a central role in shaping the sector’s evolution.

Yet as his current term approaches its expected end, attention is turning to how this chapter will conclude.

For many observers, the manner in which the transition is handled, whether through renewal, extension, or change, will play a significant role in shaping perceptions of his legacy.

Ultimately, the question facing IRA is not only about who will lead the Authority next, but about how the institution balances performance, legal frameworks, and governance principles at a critical moment in its development.