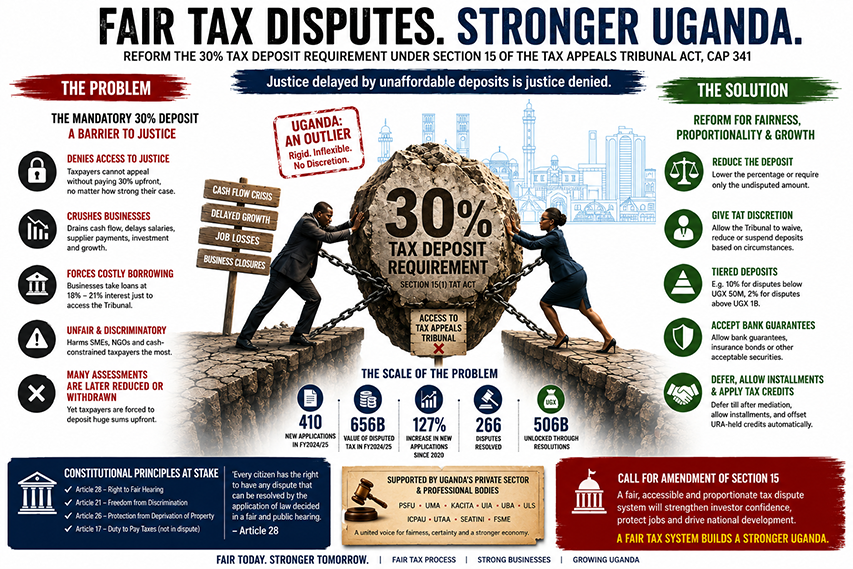

Uganda’s leading private-sector bodies, financial institutions, manufacturers, traders, lawyers, accountants, and civil society organisations have jointly petitioned the government to urgently reform what they describe as a “punitive” and economically harmful requirement that compels taxpayers to deposit 30% of disputed taxes before accessing the Tax Appeals Tribunal (TAT).

In a strongly worded petition submitted to the Ministry of Finance last month, the petitioners warn that the mandatory deposit requirement under Section 15(1) of the Tax Appeals Tribunal Act is choking business cash flows, undermining investor confidence, frustrating access to justice and worsening Uganda’s investment climate.

The petition, which the Ministry received on April 27, was backed by influential organisations including the Private Sector Foundation Uganda (PSFU), Uganda Manufacturers Association (UMA), Kampala City Traders Association (KACITA), Uganda Bankers Association (UBA), Uganda Insurers Association (UIA), Uganda Law Society (ULS), Institute of Certified Public Accountants of Uganda (ICPAU), SEATINI Uganda and the Uganda Tax Agents Association (UTAA).

The petitioners argue that while the law may have been justifiable when introduced over two decades ago, the economic realities of Uganda’s modern business environment, coupled with the sharp increase in tax disputes and aggressive tax assessments, have transformed the requirement into a major barrier to justice and business sustainability.

Mounting tax disputes fuel private sector frustration

Under the current law, any taxpayer challenging a Uganda Revenue Authority (URA) tax assessment before the Tax Appeals Tribunal must first deposit 30% of the disputed amount before the case can be heard.

The petitioners contend that the requirement disproportionately affects businesses and organisations with limited liquidity, regardless of whether the disputed assessment is later found to be flawed or excessive.

“We affirm the constitutional duty of every citizen to pay tax,” the petition states. “However, we contest the requirement to pre-pay a portion of a tax that is under legitimate challenge before any tribunal has determined the merits.”

The petition comes amid mounting tension between Uganda’s business community and URA over what many firms describe as increasingly aggressive audit practices, large retrospective assessments and rising compliance costs.

According to the petitioners, the scale and frequency of tax disputes have grown sharply in recent years. Citing the Tax Appeals Tribunal’s 2025 Performance Report, the petition notes that 410 new applications were filed in the financial year ending June 2025, representing disputed tax claims worth UGX 656 billion.

The petition further states that tax disputes filed before the Tribunal have grown by 127% since 2020, averaging 34 new filings every month. The petitioners argue that the current framework effectively forces businesses to finance large deposits even before the legality or accuracy of assessments is tested independently.

They cite examples where companies have been subjected to enormous tax demands only for the disputed figures to later be substantially reduced through mediation or settlement. One case referenced in the petition involved a taxpayer initially assessed UGX 1.5 trillion, but which later settled at only UGX 30 billion after review.

Petitioners warn of liquidity crunch and investment slowdown

According to the petitioner, such cases expose weaknesses in assessment quality and demonstrate why mandatory upfront deposits can become economically destructive.

The petition warns that the requirement is increasingly forcing businesses into difficult financial decisions, including expensive commercial borrowing, delayed supplier payments, payroll pressures and deferred investments.

“The 30% deposit creates immediate, large cash outflows that have far-reaching consequences,” the petition notes, warning that businesses are often compelled to secure loans at commercial interest rates ranging between 18% and 21% annually simply to finance disputed tax deposits.

The petition further argues that the requirement distorts taxpayer behaviour by encouraging businesses to settle questionable assessments instead of pursuing legitimate appeals.

“Taxpayers may accept incorrect assessments and ‘pay and move on’ because the deposit burden is too costly,” the petition states.

Business leaders also warn that the rule is undermining Uganda’s attractiveness as an investment destination at a time when the country is actively seeking industrial growth, foreign direct investment, and private-sector-led economic expansion.

The petition says the deposit requirement functions less as a neutral dispute resolution mechanism and more as a revenue collection tool that compromises confidence in Uganda’s tax administration system.

Constitutional questions and calls for legal reform

The coalition additionally framed the issue as a constitutional matter, arguing that the rigid application of the law undermines the right to a fair hearing by denying taxpayers access to the Tribunal simply because they lack the financial ability to raise the deposit.

The petition references several landmark court decisions, including the Supreme Court ruling in Uganda Projects Implementation and Management Centre versus URA and more recent Tax Appeals Tribunal decisions involving MTN Uganda, to argue that judicial interpretation has already started limiting blanket application of the provision in certain procedural disputes.

In the MTN Uganda matter cited by the petitioners, the Tribunal reportedly held that where disputes concern procedural validity rather than the merits of the tax assessment itself, the mandatory 30% deposit may not arise automatically.

The petition also benchmarks Uganda’s framework against regional and international jurisdictions, including Kenya, Tanzania, Sri Lanka, Nigeria, Ghana and Germany. According to the petitioners, Uganda stands out for imposing a rigid flat-rate deposit requirement with limited flexibility or discretion for waivers, reductions, or alternative securities such as bank guarantees.

Private sector pushes for flexible alternatives

Among the reforms proposed by the petitioners are reducing the deposit percentage, introducing tiered deposits based on dispute size, granting the Tribunal discretion to waive or reduce the requirement in deserving cases, recognising bank guarantees as acceptable security and allowing installment arrangements for disputed taxes.

One proposal recommends a tiered system ranging from 10% for smaller disputes to as low as 2% for disputes above UGX 1 billion.

The coalition also wants Parliament to amend the law to expressly empower the Tax Appeals Tribunal to waive or suspend the deposit requirement where disputes involve genuine legal or interpretive questions.

Pending legislative reform, the petition urges the Ministry of Finance and URA to apply existing flexibility mechanisms more consistently, including installment arrangements and offsetting tax credits against the 30% deposit obligation.

A defining debate for Uganda’s business environment

The petition now places Parliament, the Ministry of Finance and URA under growing pressure to balance government revenue collection needs against the private sector’s concerns over fairness, liquidity and access to justice.

Analysts say the outcome of the debate could have far-reaching implications for Uganda’s tax administration regime, investor confidence and ease-of-doing-business environment.

For Government, however, any reforms will likely have to carefully navigate concerns around potential abuse of the appeals process, delayed revenue collection and the risk of frivolous tax disputes.

Still, the broad-based coalition behind the petition signals that Uganda’s private sector is increasingly prepared to push back against tax policies it believes threaten competitiveness, operational sustainability and long-term economic growth.

Whether the petition results in full legislative reform or more modest administrative adjustments, it has already triggered one of the most significant business-policy debates around Uganda’s tax dispute resolution framework in recent years.