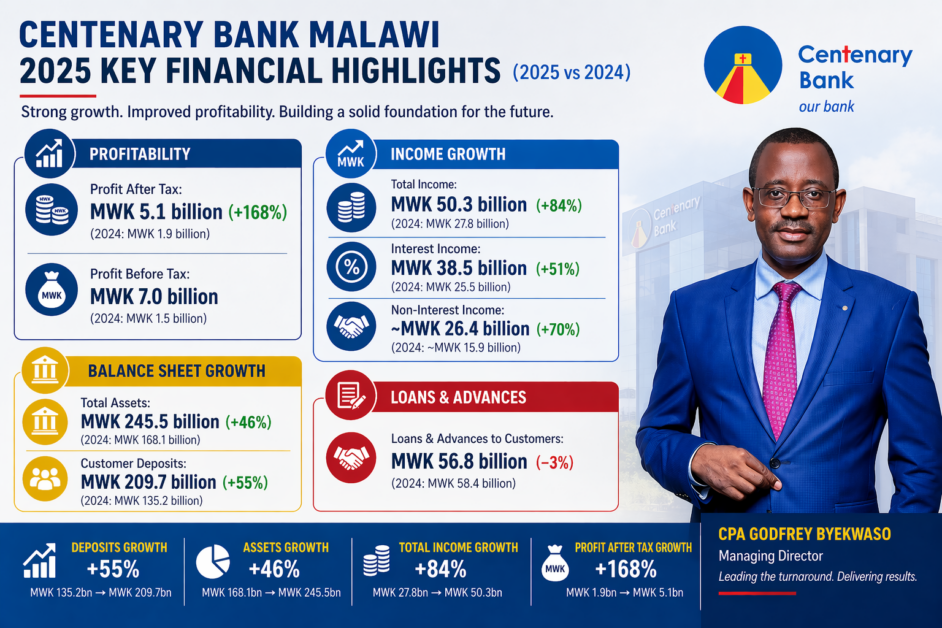

Centenary Bank Malawi closed the 2025 financial year with a profit after tax of MWK 5.1 billion (UGX 11.2 billion), representing a 168% increase from the MWK 1.9 billion (UGX 4.2 billion) recorded in 2024.

This sharp rise in profitability reflects not only revenue growth but also improved operational efficiency and a more disciplined balance sheet.

Total income expanded significantly during the year, rising by 84% from MWK 27.8 billion (UGX 61.2 billion) in 2024 to MWK 50.3 billion (UGX 110.7 billion) in 2025, supported by growth in both interest and non-interest revenue streams.

Interest income increased by 51%, from MWK 25.5 billion (UGX 56.1 billion) to MWK 38.5 billion (UGX 84.7 billion), driven largely by increased investment activity and improved asset utilisation.

Non-interest income also recorded strong growth, rising by 70% from approximately MWK 16 billion (UGX 35.2 billion) to MWK 26.1 billion (UGX 57.4 billion), reflecting higher transaction volumes and broader business activity.

Deposits surge as confidence returns

Perhaps the most telling indicator of the bank’s recovery is the performance of customer deposits.

In 2025, customer deposits grew by 55% to MWK 209.7 billion (UGX 461.3 billion), up from MWK 135.2 billion (UGX 297.4 billion) in 2024.

The surge points to a significant restoration of market confidence, an essential milestone for any institution emerging from a period of instability.

Deposit growth of this scale typically reflects not just improved liquidity, but also stronger customer trust, enhanced service delivery, and a clearer market positioning.

The deposit-led growth also provided the bank with a stronger and more stable funding base, allowing it to support operations while maintaining prudent risk levels.

Balance sheet expansion and strategic repositioning

Total assets grew by 46% to MWK 245.5 billion (UGX 540.1 billion) in 2025, up from MWK 168.1 billion (UGX 369.8 billion) in 2024, reflecting a significant expansion of the bank’s balance sheet during the year.

The largest driver of asset expansion was investment in Government of Malawi treasury bills and notes, which surged by approximately 131%, from MWK 61.2 billion (UGX 134.6 billion) in 2024 to MWK 141.2 billion (UGX 310.6 billion) in 2025.

Cash and placements with other banks also recorded moderate growth, with cash balances rising from MWK 19.9 billion (UGX 43.8 billion) to MWK 20.6 billion (UGX 45.3 billion), and placements increasing from MWK 10.9 billion (UGX 24 billion) to MWK 12.2 billion (UGX 26.8 billion), further reinforcing the bank’s liquidity position.

In contrast, loans and advances to customers remained relatively stable, declining slightly from MWK 58.4 billion (UGX 128.5 billion) in 2024 to MWK 56.8 billion (UGX 125.0 billion) in 2025.

Managing risk in a difficult operating environment

The 2025 results must be viewed within the broader context of Malawi’s macroeconomic conditions, which remained challenging throughout the year.

As noted in the bank’s financial report, inflation averaged 28.4%, while the policy rate remained at 26%.

Within this environment, asset quality pressures became more pronounced.

Impairment charges increased by 351% to MWK 14.8 billion (UGX 32.6 billion) in 2025 compared to MWK 3.3 billion (UGX 7.3 billion) in 2024, mainly due to deterioration of the legacy loan portfolio and impairment allowances on government securities.

From an analytical standpoint, the scale of this increase suggests that a significant portion of the bank’s earnings is being directed toward absorbing legacy risks and strengthening the balance sheet.

While this weighs on short-term profitability, it also indicates a deliberate and disciplined approach to risk recognition.

In practical terms, elevated provisioning at this stage of the turnaround signals a shift toward balance sheet transparency and long-term stability.

By addressing asset quality issues early, the bank is positioning itself to support more sustainable credit growth once macroeconomic conditions stabilise.

From stabilisation to structured growth

The bank’s 2025 performance is best understood not as a standalone success, but as the outcome of a broader, multi-phase transformation journey that began well before the year under review.

Since joining Centenary Bank Malawi in April 2023 as deputy managing director, Godfrey Byekwaso has been closely involved in the institution’s stabilisation process, working to restore operational control, reinforce governance structures, rebuild customer confidence, and realign the bank’s strategic direction.

These early interventions laid the foundation for recovery, allowing the bank to transition from a period of uncertainty into one of greater institutional coherence and financial discipline.

By the time he assumed the full managing director role in October 2024, much of the stabilisation phase had been executed, creating the conditions necessary for more deliberate and sustained growth.

In 2025, these efforts began to translate into measurable outcomes. The bank entered a phase of structured growth, characterised by strong deposit mobilisation, a broad-based expansion in revenue streams, a cautious and disciplined approach to risk management, and a return to improved profitability.

Rather than pursuing rapid expansion, the focus appears to have been on building a stable, well-capitalised institution—positioned to grow sustainably over the medium to long term.

A measured turnaround and a platform for growth

Centenary Bank Malawi’s 2025 performance does not represent an overnight transformation, but rather the outcome of a structured and disciplined process that began in 2023 and has now entered a phase of measurable growth.

Under Byekwaso’s leadership, the bank has progressed from stabilisation to recovery and is increasingly positioning itself for sustained expansion.

In a high-inflation, liquidity-constrained operating environment, delivering 55% deposit growth, 46% asset expansion, and a 168% increase in profitability goes beyond headline performance.

It signals that the institution has regained stability, rebuilt confidence, and established a stronger financial and operational footing.

With its balance sheet stabilised, profitability restored, and deposits providing a solid funding base, the bank now appears to be transitioning into the next phase of its evolution.

This phase is likely to be defined by a gradual expansion of the loan book, continued investment in digital banking capabilities, and a deeper focus on SME and retail banking segments.

At the same time, management has indicated a continued emphasis on cost rationalisation, prudent risk management, and diversification of funding sources, measures aimed at sustaining growth while preserving balance sheet strength.

Taken together, these priorities suggest a deliberate shift from recovery to forward-looking expansion, anchored in discipline and supported by a more resilient institutional foundation.

Follow