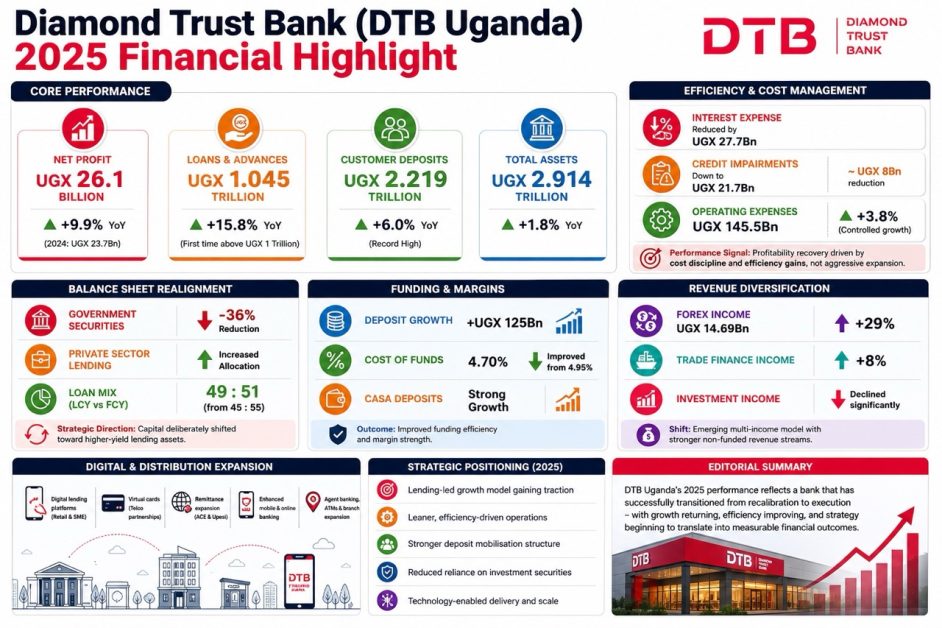

Diamond Trust Bank Uganda’s 2025 results mark a strong and encouraging return to growth, with net profit rising by 9.9% to UGX 26.1 billion, up from UGX 23.7 billion in 2024. While modest on the surface, this recovery is significant—it signals a bank regaining momentum after a year of deliberate recalibration.

Efficiency gains were driven primarily by a reduction in interest expense on borrowings by UGX 27.7 billion, credit impairments—down by about UGX 8 billion to UGX 21.7 billion—and tighter control of operating expenses, which rose marginally by 3.8%, i.e. approximately UGX 5.3 billion to UGX 145.5 billion, alongside improved funding efficiency that allowed the bank to grow deposits without a corresponding rise in interest costs.

The bank has strengthened its bottom line not through aggressive expansion, but through greater efficiency—deploying capital more strategically, tightening cost discipline, and shifting toward higher-yielding assets. The result is a business that is becoming leaner, more focused, and more intentional in how it generates returns.

The 2025 performance marks a clear recovery from a period of deliberate recalibration, when the bank saw significant adjustments in its key financial metrics as Godfrey Sebaana—appointed Managing Director and CEO in April 2024—began implementing a series of strategic shifts in execution, asset allocation, and revenue drivers.

In that transition year 2024, DTB undertook a measured repositioning of its balance sheet. Deposits declined by 5.1%, falling from UGX 2.207 trillion in 2023 to UGX 2.094 trillion in 2024, while total assets contracted by 4.8% to UGX 2.863 trillion. Lending growth slowed markedly, rising just 3.2% from UGX 874.2 billion in 2023 to UGX 902.2 billion in 2024, as the bank recalibrated its asset mix and stepped back from lower-yielding positions. The true cost of the transition, however, was felt at the bottom line, where net profit declined sharply from UGX 41.0 billion to UGX 23.7 billion.

Seen in this light, the 2025 performance is the first clear outcome of a strategy taking root. It reflects a bank in transition—one that has actively reshaped its asset mix, rethought its funding model, and absorbed the short-term cost of change in pursuit of long-term efficiency and growth.

Rather than preserving stability for its own sake, DTB has repositioned itself for a more dynamic, return-focused future.

If 2024 was the year of recalibration, then 2025 is where that strategy begins to take hold.

Credit Takes Centre Stage Under Sebaana

The most visible outcome of this reset is the bank’s renewed emphasis on credit.

Loans and advances grew by 15.8%, from UGX 902.2 billion in 2024 to UGX 1.045 trillion in 2025, marking the first time DTB’s loan book has crossed the trillion-shilling threshold. Notably, this represents the strongest lending growth in five years, matching the last peak recorded in 2021–2022, and a sharp rebound from the subdued 3.2% growth in 2024.

This milestone reflects a deliberate shift away from low-yield investments, particularly government securities, toward more productive, higher-return lending. Indeed, the bank reduced its exposure to government securities by approximately 36%, reallocating capital into private sector credit.

For Sebaana, this shift is both strategic and timely. Uganda’s economy expanded by approximately 6.5% in 2025, with private sector credit growth recovering to around 11% after a contraction in the previous year. This improving environment has created opportunities for banks willing to lend—and DTB is positioning itself firmly within that space.

As the CEO notes, the bank has continued to “execute and refine our business strategy to adapt to the evolving operating environment,” leveraging both its sales force and technology investments to expand across retail, SME, and corporate segments.

Despite strong growth in lending and deposits, DTB’s overall balance sheet expansion has remained measured. Total assets grew by just 1.8%, from UGX 2.863 trillion in 2024 to UGX 2.914 trillion in 2025.

Deposits Rebound—and a New Funding Strategy Emerges

On the funding side, DTB’s recovery is equally telling. Customer deposits grew by 6.0%, rising from UGX 2.094 trillion in 2024 to UGX 2.219 trillion in 2025, an increase of over UGX 125 billion that not only reverses the previous year’s decline but pushes the bank to a new record.

But beyond the headline growth lies a deeper transformation in how deposits are mobilised.

Various initiatives have been implemented to drive Current Account Savings Account (CASA) growth, and they are beginning to pay off. Low-cost deposits have increased significantly, helping reduce the bank’s cost of funds from 4.95% in 2024 to 4.70% in 2025.

Sebaana has been particularly emphatic about the bank’s deliberate shift toward efficiency over expansion, with a strong focus on operational efficiency driven by automation and technology. Several processes have already been identified where digital solutions can reduce manual intervention, enabling the bank to “achieve more with less.”

Beyond Interest: Building a Diversified Revenue Engine

Alongside lending, DTB is also reshaping how it earns.

The bank is expanding its non-funded income streams, reducing reliance on traditional interest income. In 2025, foreign exchange income rose sharply by 29%, from UGX 11.35 billion to UGX 14.69 billion, reflecting a deliberate push to grow treasury-driven revenues and expand its FX customer base. Trade finance income also grew by 8%, contributing to a broader effort to diversify earnings.

This shift comes against a backdrop of declining income from investment securities, which fell significantly from UGX 161.95 billion in 2024 to UGX 101.21 billion in 2025, following a deliberate reduction in government securities holdings.

Together, these movements highlight a fundamental change—not just in how much the bank earns, but how it earns it. DTB is evolving into a more multi-income bank, where fees, commissions, and trading income play a larger role alongside lending.

By deepening collaboration between business units and treasury, the bank is strengthening cross-selling opportunities and building a more resilient, diversified revenue base.

Digital, Distribution, and the Culture of Agility

At the centre of this transformation is a strong push toward digital capability and distribution expansion. DTB has rolled out digital lending products for retail and SMEs, virtual card services in partnership with telecoms, expanded remittance services through ACE and Upesi, and enhanced mobile and online banking platforms.

At the same time, the bank is expanding its physical and digital reach through offsite ATMs, agent banking, and new branches in high-growth areas. But perhaps more important than the infrastructure is the cultural shift. Sebaana describes DTB as a “human-led, technology-enabled” organisation, highlighting the speed at which the bank has moved from concept to product—an agility he says the bank must continue to nurture as it builds competitiveness in an increasingly digital marketplace.

Growth with Discipline

Even as DTB accelerates lending, it remains acutely aware of the risks.

“Maintaining our credit discipline remains a core priority,” Sebaana affirms, pointing to ongoing investments in credit governance and risk management.

The bank is also actively de-risking its balance sheet. The ratio of local currency to foreign currency loans has improved to 49:51 in 2025, up from 45:55 in 2024, reducing exposure to exchange rate volatility.

This balanced approach—growth with discipline—is central to DTB’s strategy under Sebaana.

Positioned for Uganda’s Growth Agenda

DTB’s transformation is closely aligned with Uganda’s broader economic ambitions.

The bank is targeting key sectors under the government’s ATMS strategy—Agro-industrialisation, Tourism, Minerals (including oil and gas), and Science and Technology—positioning itself as a key financial intermediary in the country’s long-term development.

As CEO Godfrey Sebaana explains, “At a country level, the bank’s business growth strategy is aligned to Uganda’s ATMS strategy. The bank is well positioned to support the government to drive industrialisation, increase exports and shift labour from subsistence to higher productivity sectors through its financial intermediation role.”

With Uganda aiming to grow its economy from approximately $50 billion to $500 billion by 2040, the opportunities are significant. DTB is positioning itself to play a meaningful role in financing that growth.

A Measured Outlook: From Reset to Results—and the Road Ahead

DTB Uganda’s 2025 performance is best understood not in isolation, but as the first clear outcome of a strategy that began disrupting the business a year earlier.

The sharp adjustments in 2024—declining deposits, reduced assets, slower lending, and a steep drop in profitability—were not signs of weakness, but the cost of recalibration. They created the space for a more deliberate, efficiency-driven model to emerge.

In 2025, that model is beginning to deliver.

Deposits have recovered and surpassed previous levels. Lending has accelerated decisively, crossing the trillion-shilling mark. Asset growth has resumed, albeit selectively. And profitability has returned, even in the face of declining income—pointing to a bank that is becoming leaner, sharper, and more intentional.

Management remains confident in this trajectory. As CEO Godfrey Sebaana notes, “our unwavering focus to drive sustained business growth delivered improved results in 2025,” adding that the bank will continue to expand its distribution capabilities, scale lending, and leverage technology to “drive operational efficiency through increased automation.” He maintains that DTB is “well positioned to deliver sustainable growth and create lasting value to our stakeholders.”

Yet, even as execution gains traction, the Board offers a more measured perspective.

Chairman Azim Kassam highlights Uganda’s strong macroeconomic fundamentals, noting that the country remains “one of the most compelling growth frontiers in East Africa,” supported by a young population, a diversified economy, and improving institutional strength. However, he cautions that this outlook remains exposed to external shocks. “The crystallisation of geopolitical risks… could test this resilience,” he warns, particularly if global developments disrupt supply chains, increase fuel prices, or trigger inflation and exchange rate volatility.

For DTB, such pressures could translate into “slower balance sheet growth, pressure on asset quality and higher funding costs in a tighter monetary environment.”

Even so, Kassam underscores confidence in the bank’s strategic direction, pointing to a model anchored on “customer reach, digital transformation and sustainability excellence” as key pillars for navigating an increasingly complex operating environment.

Looking ahead, the path is clear—but not without risk.

If 2024 was the year DTB chose to recalibrate, then 2025 is the year it began to prove that the reset was working. The next phase will test something deeper: whether this more efficient, lending-led, and digitally enabled model can sustain momentum while preserving asset quality and managing external shocks.

As Sebaana puts it, the bank is focused on growing “in a sustainable, convenient [way], without compromising on our risk and compliance standards”—a balance that will define its next chapter.

For now, one thing is certain—DTB Uganda is no longer optimising for comfort. It is building for performance.