KCB Bank Uganda has delivered a breakout financial performance in 2025, with net profit surging 65% to UGX 49.3 billion, up from UGX 29.9 billion the previous year, as the bank’s growth strategy began to translate into powerful earnings momentum.

The performance marks a defining moment for the lender, signalling a transition from steady expansion into a phase of accelerated, efficiency-driven growth phase, underpinned by strong deposit mobilisation, disciplined lending, and improving cost management.

At the heart of the 2025 results was robust balance sheet expansion. Total assets grew by 28.2% to UGX 2.2 trillion, up from UGX 1.7 trillion in 2024, reinforcing the bank’s growing scale and market relevance. This growth was largely funded by a sharp increase in customer deposits, which rose by 33.9% to UGX 1.67 trillion, reflecting both rising customer confidence and the bank’s success in deepening its funding base.

On the asset side, net loans and advances expanded by 28.7% to UGX 1.16 trillion, demonstrating continued credit growth across key sectors of the economy. Importantly, lending growth remained slightly below deposit growth, signalling a measured and disciplined approach to risk, even as the bank scaled its loan book.

The income statement tells an equally compelling story. Total income increased by 23.3% to UGX 297.4 billion, driven by higher lending volumes and improved revenue generation across core banking activities. At the same time, cost growth remained contained, with total expenses rising by just 14.8% to UGX 230.2 billion.

This gap between income and expense growth unlocked significant operating leverage, with profit before tax jumping 64.9% to UGX 67.1 billion, ultimately driving the sharp rise in net earnings.

Edgar Byamah’s Strategic Transformation of KCB Uganda

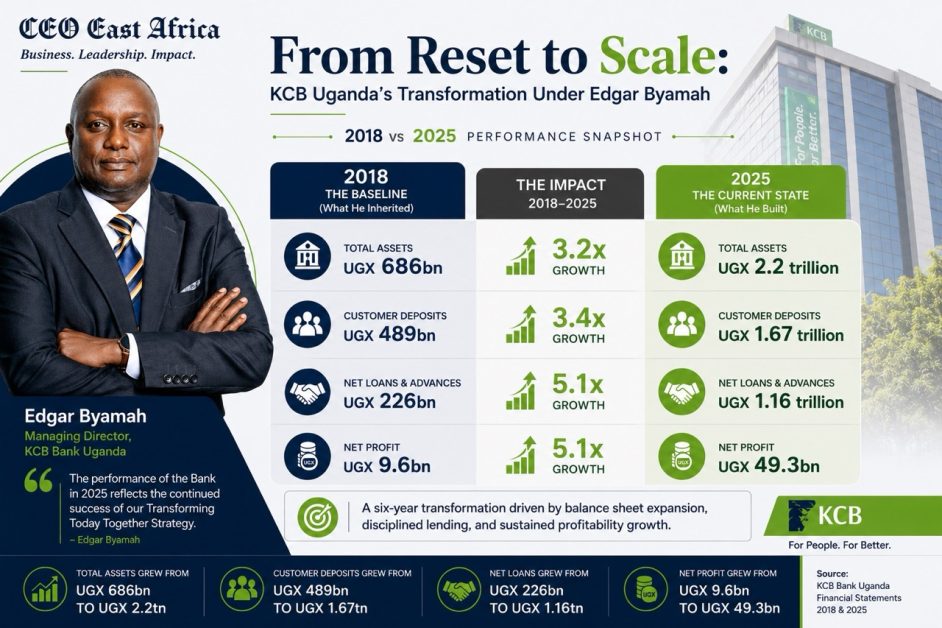

Behind KCB Uganda’s 2025 breakout performance lies a longer, deliberate transformation engineered by Managing Director Edgar Byamah, who took over leadership in early 2019. Using 2018 as the true baseline, the scale of that shift is striking.

At the time, KCB Uganda was a UGX 686 billion asset bank generating just UGX 9.6 billion in profit, operating largely as a modest mid-tier player with limited scale and influence. Six years later, the bank has evolved into a UGX 2.2 trillion institution delivering UGX 49.3 billion in earnings, effectively repositioning itself within Uganda’s competitive banking landscape.

This transformation has been driven by a clear, lending-led growth strategy. Over the period, customer deposits have more than tripled (3.4x) to UGX 1.67 trillion, while the loan book has expanded over fivefold (5.1x) to UGX 1.16 trillion, anchoring both revenue growth and market relevance. The balance sheet has similarly scaled more than threefold, while profitability has increased over five times from its 2018 base—despite an early reset phase that saw the bank post a loss in 2019.

The trajectory reflects a disciplined strategic arc: an initial balance sheet clean-up and reset, followed by stabilisation, and ultimately a phase of accelerated growth and scale. The 2025 performance is therefore not an isolated spike, but the culmination of a multi-year execution strategy focused on building a strong funding base, expanding credit, and improving operational efficiency.

Preliminary analysis by CEO East Africa Magazine reinforces this positioning. Over the last five years (2020–2025), KCB Uganda has delivered one of the fastest growth trajectories in the sector. Customer deposits grew from UGX 445.6 billion to UGX 1.67 trillion—up 275% (3.7x), translating into a CAGR of approximately 29%, while loans and advances expanded from UGX 253.2 billion to UGX 1.16 trillion—up 359% (4.6x), with a CAGR of about 35–36%.

Over the same period, total assets increased from UGX 657.3 billion to UGX 2.2 trillion—up 235% (3.4x), representing a CAGR of roughly 27%, while total income rose from UGX 78.7 billion to UGX 297.4 billion—up 278% (3.8x), with a CAGR of approximately 30%. Net profit, measured from the post-turnaround base of 2020, grew from UGX 13.2 billion to UGX 49.3 billion—up 273% (3.7x), translating into a CAGR of about 30%.

This pace of expansion places KCB among the most aggressive balance sheet and earnings growers in the industry, particularly within the mid-tier segment, where few banks have combined such rapid deposit mobilisation, sustained credit expansion, and compounding profitability.

Beyond the Numbers: The Strategy Behind the Growth

Beyond the strong headline figures, KCB Uganda’s 2025 performance is underpinned by deliberate strategic choices that have translated into tangible impact across the economy, businesses, and communities. At the centre of this execution is the bank’s “Transforming Today Together” strategy, which has shaped both its growth trajectory and market positioning.

As Managing Director Edgar Byamah notes, “Our performance in 2025 reflects the continued success of our Transforming Today Together Strategy.” This strategy has not only driven financial expansion but has also ensured that growth remains anchored in relevance—responding to evolving customer needs while strengthening the bank’s long-term resilience.

A key pillar of this approach has been scaling access to credit for businesses, with the bank deliberately increasing financing thresholds to enable clients to move beyond participation to meaningful growth. Bid bond limits, contract financing, and invoice discounting facilities have all been expanded, allowing businesses to bid for larger contracts, execute more effectively, and scale operations with confidence. This shift reflects a broader repositioning of the bank—from a transactional lender to a growth enabler within Uganda’s private sector.

KCB has also strategically positioned itself at the forefront of Uganda’s emerging oil and gas economy, supporting local participation across the value chain. Through tailored solutions such as tax bridge loans, commodity financing, and collateral management arrangements, the bank is enabling businesses to access working capital and compete in one of the country’s most transformative sectors.

At the same time, the bank has continued to invest in thought leadership and ecosystem engagement, exemplified by its Power Talk series, which convenes stakeholders to address national development priorities and unlock opportunities in key sectors such as oil and gas. These engagements reinforce KCB’s role not just as a financier, but as a catalyst for dialogue and sector growth.

Beyond commercial performance, the strategy also extends into inclusion and sustainability. Through initiatives such as the Twekozese programme, the bank has supported over 2,350 young people with market-relevant skills, while significantly increasing women’s participation in technical and entrepreneurial spaces. Environmental efforts, including the planting of over 15,000 trees, further reflect a commitment to long-term sustainability.

Internally, the bank has invested in building a modern, people-centred work environment, recognising that its workforce is central to sustained performance. The development of its new head office at Lohana Towers, with facilities designed to enhance wellbeing, collaboration, and productivity, signals a deliberate focus on organisational resilience and future readiness.

As Byamah emphasises, “It is anchored on ensuring that the Bank remains responsive to the evolving needs of our customers and operating environment, while strengthening operational resilience and long-term sustainability.”