The entrance of Raxio into the Ugandan market to offer Data Centre services for enterprises is timely. The Ugandan market is a take off stage where most enterprises; big and small, have embraced automation and are moving their services and operation processes to digital platforms with high computing resources.

The digital transformation journey involves touching critical business domains including business model, approach to innovation, technology model, customer engagement and so on. The triad of confidentiality, integrity and availability of Data as a biggest resource for any enterprise must always be among priorities of efficiency and effectiveness for businesses. Achieving this involves substantial technology capital investment in terms of computing resources like reliable networks, servers for processing power, storage solutions for data, applications, disaster recovery procedures and hiring technical human resource.

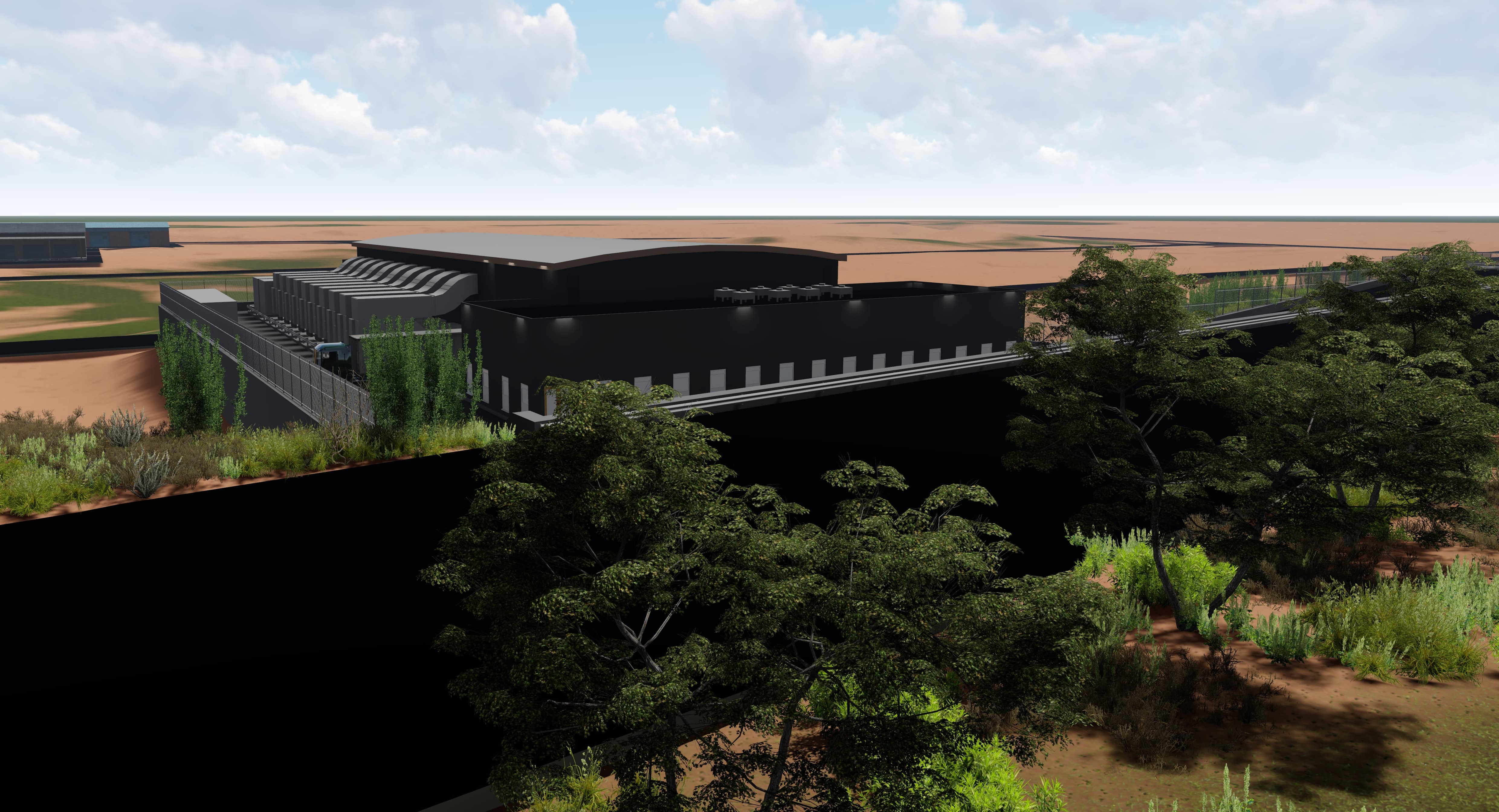

I find Raxio to have come in to take care of all the above cost burden so that enterprises can concentrate on their core businesses and transfer all the technology risks to Raxio. I also find Raxio a solution to the current regulatory restrictions on regulated financial institutions concerning having their mission critical systems hosted in-country. Some years back, the central bank ordered all financial institutions to host their business systems in in-country data centres as a mitigation against risks that may befall systems hosting locations outside the country where Uganda may not have control.

However, although Raxio is the first privately run carrier-neutral facility, it is worth noting that Raxio is not the first data centre in Uganda. The market probably needs an interrogation on why such services have not been embraced fully by the enterprises that need them. I know NITA-U have been conducting assessments on readiness of taking on cloud as a service.

Am sure the findings can give Raxio some mileage.

Raymond Ayebazibwe Karamagi is an ICT Specialist – ICT Infrastructure, Networks & Security

+256 773760821

Email : ayebraymond@gmail.com