Uganda’s Pride Bank has released its 2025 financial results — its first reporting year following the Tier II licence — delivering an accelerated performance marked by robust balance sheet expansion, strengthening income growth, and a sharp rise in profitability.

Pride Microfinance Limited officially transitioned into a Tier II Credit Institution, rebranding as Pride Bank Limited, on April 29, 2025. The Bank of Uganda issued the license for this upgrade on November 26, 2024, enabling Pride to broaden its services to include enhanced credit facilities and expanded savings options.

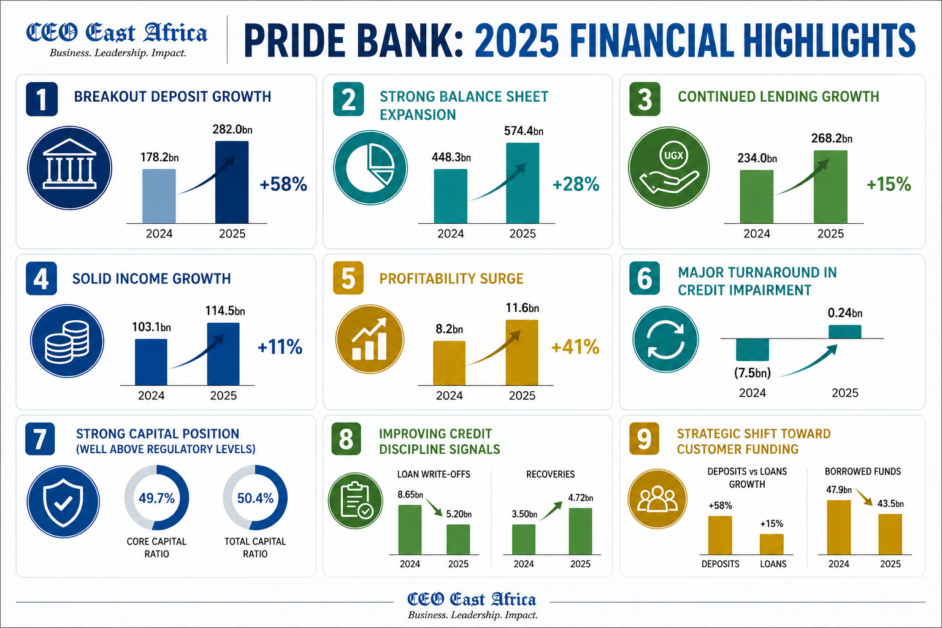

Customer deposits surged by 58% from UGX 178.2 billion in 2024 to UGX 282.0 billion in 2025, marking the most significant driver of growth during the year. This rapid expansion in funding provided the liquidity base to support increased lending activity and income generation.

Loans and advances rose by 15% from UGX 234.0 billion to UGX 268.2 billion, reflecting continued credit extension across the bank’s core segments. While loan growth was more measured relative to deposits, it signals a deliberate approach to balancing expansion with risk management.

This balance translated into steady income growth, with total income increasing by 11% from UGX 103.1 billion to UGX 114.5 billion, supported by higher interest earnings from the expanded loan book and stable fee-based income streams. Net interest income remained the dominant contributor, underlining Pride’s core lending model.

At the same time, the bank continued to invest in its operations, with total expenses rising by 6% from UGX 94.3 billion to UGX 100.3 billion, driven by increases in personnel costs and other operating expenses. However, this cost growth was offset by improved operating income and a notable turnaround in credit impairment performance.

A shift from a UGX 7.5 billion impairment charge in 2024 to a net credit position of UGX 0.2 billion in 2025 significantly boosted earnings, highlighting improved loan recoveries and better asset performance.

As a result, profit after tax increased by 41% from UGX 8.2 billion to UGX 11.6 billion, signalling stronger earnings resilience.

The bank’s balance sheet expanded accordingly, with total assets growing by 28% from UGX 448.3 billion to UGX 574.4 billion, reinforcing Pride Bank’s position as one of the largest Tier II institutions in Uganda.

This growth is underpinned by a strong capital base. While capital ratios moderated slightly due to balance sheet expansion, core capital adequacy stood at 49.7% (down from 54.6%) and total capital adequacy at 50.4% (down from 55.4%), remaining well above regulatory requirements and providing a solid buffer to support future growth.

On asset quality, non-performing loans increased by 15% from UGX 8.25 billion to UGX 9.51 billion, but improved recoveries — rising from UGX 3.50 billion to UGX 4.72 billion — alongside lower loan write-offs point to a stabilising credit environment and strengthening risk management practices.

Driving Impact: Lending to the Real Economy and Expanding Financial Inclusion

In line with its purpose of “Transforming Lives Responsibly,” Pride Bank’s growth extends well beyond balance sheet expansion, anchored in its role as a financial inclusion engine for underserved segments of Uganda’s economy.

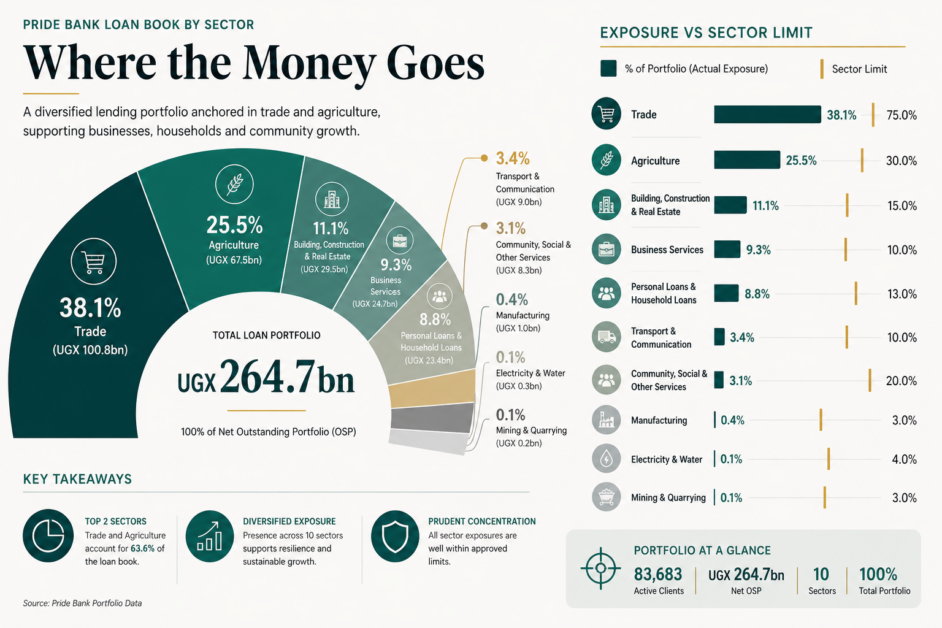

The bank’s loan book reflects this mandate. As of 2025, its UGX 264.7 billion portfolio is spread across 10 sectors, with a clear concentration in the real economy. Trade accounts for 38.1% (UGX 100.8 billion) of total lending, followed by Agriculture at 25.5% (UGX 67.5 billion)—together representing nearly two-thirds of the portfolio. Other key segments include Building, Construction and Real Estate (11.1%), Business Services (9.3%), and Personal and Household Loans (8.8%), underscoring a diversified yet purpose-driven lending strategy focused on MSMEs, agri-value chains, and informal-sector participants.

This sectoral distribution is matched by scale on the ground. Since 2017, Pride Bank has disbursed over 1,062,942 loans worth approximately UGX 2.97 trillion, reflecting sustained credit delivery to micro, small, and medium enterprises across the country.

By the end of December 2025, the bank served a total clientele of 83,683 customers, of whom 37,343 were women, reinforcing its continued focus on inclusive access to finance. Agriculture alone accounted for 15,462 clients, spanning both smallholder farmers and value chain traders, highlighting the bank’s deep penetration in one of Uganda’s most critical economic sectors.

On the funding side, the sharp 58% increase in deposits—from UGX 178.2 billion to UGX 282.0 billion—signals growing customer trust and engagement. The depositor base has expanded to 327,229 customers, supported by a nationwide footprint of 43 branches and 4 contact offices.

Customer growth has also accelerated, with 18,421 new borrowers onboarded in 2025, representing a 22% increase in customer accounts and reflecting deeper penetration across both rural and peri-urban markets.

Taken together, these data points point to more than just institutional growth. They highlight a lending model deliberately anchored in sectors that drive livelihoods—trade, agriculture, and small-scale enterprise—while maintaining diversification across services, construction, and household finance.

Ultimately, Pride Bank’s expansion is not merely balance sheet-driven. It is grounded in real economic participation—extending credit, mobilising savings, and widening financial access for individuals and businesses that remain structurally underserved by traditional banking institutions.

A 16-Year Transformation: From MDI to Tier II Banking Powerhouse

The 2025 performance cannot be fully understood without situating it within Pride Bank’s longer-term trajectory under Managing Director Veronicah Namagembe.

Since 2009, the institution has undergone a profound transformation — evolving from a modest microfinance deposit-taking institution into a dominant Tier II player.

Over this period, Pride Bank has delivered remarkable scale across its core financial metrics, with customer deposits growing from UGX 13.8 billion to UGX 282.0 billion — a more than twentyfold increase. Its loan book has expanded from UGX 47.8 billion to UGX 268.2 billion, representing nearly sixfold growth, while total assets have risen from UGX 66.1 billion to UGX 574.4 billion, an almost ninefold increase.

Over the same period, profitability has remained resilient despite cyclical fluctuations, growing from UGX 2.4 billion in 2009 to UGX 11.6 billion in 2025 — representing an approximate 10% compound annual growth rate — with the bank maintaining profitability every year, including through periods of economic disruption such as COVID-19.

This growth has been achieved consistently, even through economic disruptions such as COVID-19 and broader macroeconomic volatility.

The culmination of this journey came in November 2024, when Pride was granted a Tier II banking license by the Bank of Uganda — a milestone that formalised its evolution into a fully-fledged credit institution.

This transition is not merely regulatory; it represents a fundamental shift in the bank’s operating model, enabling expanded product offerings, increased lending capacity, deeper participation in Uganda’s financial system, and a significantly enhanced ability to mobilise deposits at scale.

The 2025 results, therefore, represent the first tangible output of this new phase, where years of institutional building are now translating into accelerated growth.

Under Namagembe’s leadership, Pride Bank has demonstrated a rare balance: scaling commercially while remaining anchored in financial inclusion.

Outlook: Scaling the Next Phase of Growth and Impact

As Pride Bank enters its second year as a Tier II institution, the focus now shifts from transition to execution at scale.

With a significantly expanded deposit base and strong capital buffers, the bank is well-positioned to deepen its impact across the economy. Priorities for this next phase include deepening lending across key sectors such as Agriculture, Public sector, Trade & Business, transport, Building & Real estate, Education, expanding digital and branch-based access channels to reach 544,558 customers by 2030 and introducing more sophisticated financial products tailored to customer needs.

“We are now focused on achieving the 2026 – 2030 strategy that will transform Pride into a digital-first bank,” says Managing Director Veronicah Namagembe, adding: “As a tier II financial institution, Pride is better positioned to serve its growing customer base with unique but customer-centric products such as trade finance, telegraphic transfers, mortgage loans, forex accounts, among others.”

The opportunity ahead lies in translating this financial strength into broader economic impact, particularly in SME financing, agricultural value chains, youth and women entrepreneurship, and affordable credit for underserved communities.

“At the core of our strategy is sustainable business growth, customer centricity, digital and data-driven efficiency and a high-performance culture,” Namagembe adds. “We also intend to have atleast 25% of the total loan book in the Agriculture sector by 2030.”

At the same time, sustaining asset quality, tightening cost discipline, and protecting profitability will be critical as the bank scales. Pride Bank is targeting a 12.2% return on equity, a 3.5% non-performing loan ratio, and a 76% cost-to-income ratio—benchmarks that signal a deliberate shift toward disciplined, sustainable growth.

Stakeholders — including customers, regulators, and development partners — will be watching how the bank balances its dual role as a commercially viable institution and a driver of financial inclusion.

To fully articulate this next phase, further clarity on strategic priorities, sector focus, customer growth targets, and innovation roadmap will be key. The bank is expected to roll out agency banking, mobile-based loans, an improved dynamic website and a mobile application as part of its Tier II expansion strategy.

What is already evident, however, is that Pride Bank enters this phase from a position of strength — built on a 16-year foundation of disciplined growth and now reinforced by its Tier II status.