By Taddewo Senyonyi

On June 28, 2011, the president of Uganda Yoweri Kaguta Museveni assented into law the Uganda Retirement Benefits Regulatory Authority (URBRA) Act 2011, with a major aim of regulating and controlling the pension sector.

The Authority started receiving applications from retirement benefit schemes and market players in December 2012 since it is a requirement that every pension scheme and service provider be licensed prior to undertaking any business.

However, there have been reports that the authority is failing to fulfill its mandate. The CEO’s Taddewo Senyonyi interviewed Andrew Kasirye, the Board Chairman, URBRA, about these claims and the progress so far made in fulfilling the law. Below are excerpts :

Briefly tell me about URBRA and its mandate?

The Uganda Retirement Benefits Regulatory Authority (URBRA) was established in 2011 as a regulatory framework under which all players in the pension industry can be effectively guided and given oversight. The players are pension schemes, fund managers, trustees, custodians and administrators. Before this law, there were existing pension schemes in the telecom sector and other private organizations, but they were being run without a clear approach, so the law came in place to harmonize the pension industry.

What are the different roles of a Trustee, an Administrator, a Custodian and a Fund manager?

In the first place, a pension scheme is a collection of a group of people saving money for their retirement. A Trustee is a person /company responsible for making decisions in a company managing a Retirement Benefits Scheme in accordance with the scheme rules the sponsor sets up. The trustee deed helps in making investment decisions with the help of a fund manager.

An Administrator on the other hand, is a person/company appointed by a trustee responsible for keeping records of the scheme including registering members, maintaining member records, reconciling contribution records and other services as maybe specified. An administrator can be in house or outsourced. For example Alexander Forbes is an administrator that can be outsourced. Unlike in house administrators, administrators are licensed by URBRA.

Fund Managers are appointed by trustees to manage their funds on agreed terms guided by the investment policy of the scheme. They carryout investment roles and are licensed by Capital Markets Authority and URBRA while a Custodian is a financial institution that offers custodial services, keep monies of the scheme. For custodians to be licensed by URBRA, they should have a letter of no objection or permission from Bank of Uganda.

The Uganda Retirement Benefits Regulatory Authority became effective in September 2011, what progress have you made in implementing this law?

Significant progress has been registered. The minister for finance appointed the board on 31st August 2012 and within this period we have put in place licensing rules; there’s a statutory instrument for licensing each of the players (schemes, trustees, administrators, fund managers and custodians). We worked on the laws and they had to be approved by the government and gazetted.

Before the law, there were existing players and the law told us to first deal with those and we are dealing with them. However, we don’t have a data base about these retirement benefits schemes, so we are going to embark on a nationwide survey to know which entities in the pension industry existed before the law. There are some that we know but they haven’t come forward maybe they are still waiting for the full liberalization of the sector and see what the law will provide.

It may also be due to our regulations which call for transparency and accountability which they haven’t been doing. I want to tell them that we are very flexible in applying the law. Those we have licensed, we have given them provisional licenses because they need to change the way they have been using their schemes in accordance with the law.

We want to help them build internal capacity through training in as far as investment, financial controls and reporting and governance are concerned. We have also managed to bring together key players in the financial sector; Bank of Uganda, Insurance Regulatory Authority, Uganda Securities Exchange, Capital Markets Authority and Uganda Revenue Authority in reforming the pension sector.

Modernising General Insurance: SanlamAllianz CEO Ruth Namuli on Building Uganda’s Insurance Powerhouse with Trust, Innovation, and Scale

Modernising General Insurance: SanlamAllianz CEO Ruth Namuli on Building Uganda’s Insurance Powerhouse with Trust, Innovation, and ScaleHow many Trustees, Administrators, Custodians and Fund managers have you approved/licensed since you were operationalized?

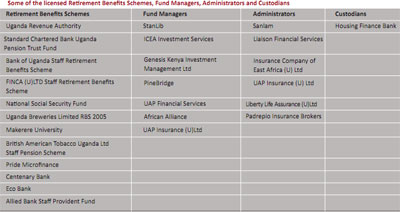

We have received many applications from trustees and to date 190 of them have been processed; we are working on processing their licenses. You see we have to observe due diligence. We have so far licensed 12 Retirement Benefits Schemes, seven (7) Fund Managers, three (3) Custodians and seven (7) Administrators, but I would like to clarify that many others have been processed just waiting for the licenses to be issued. Notably, NSSF has started complying with URBRA and we have issued them a provisional license and will continue working with them so that they remain relevant.

There are reports that you’re failing to uphold your mandate, with a backlog of licenses yet to be cleared. What are the challenges failing you?

That’s not true. As I have already said the minister for finance appointed the board on 31st August 2012 and within this little period we have achieved a lot as I have already indicated. It’s true we lacked financial resources because we were instituted in the middle of the year, but this has been catered for in this budget.We are in the process of recruiting a CEO and we are looking at an international recruitment. This is because we have many Ugandans with international exposure working in western countries.

The move to liberalize the sector and the proposed liberalization bill is said to have been based on two erroneous foundations, namely: bad corporate governance at NSSF and that NSSF had a monopoly on the pensions sector. Yet currently the management of the pensions sector has greatly improved and the NSSF Act allows the Minister responsible for NSSF to permit other players to enter the pension sector. This being the case, do you really think the liberalization of the sector has been made in good faith?

The NSSF Act is not in tandem with what our society demands today. It was Government’s first response towards the need to provide a social safety net for its working population .That Law was specifically designed for the formal sector where persons have ascertainable monthly income . Today, NSSF has slightly less than 500,000 members yet Uganda’s working population is approximately 12 million.

This Reform process among other issues addresses the need to extend pension coverage to the informal sector .Through public awareness and advocacy initiatives URBRA shall reach out to our very young working population in the informal sector and get them to subscribe to voluntary retirement benefit schemes. We shall partner with Trade Unions and Vocation based workers associations to reach out to market vendors, taxi drivers, lorry drivers, turn boys and brokers, artisans in all trades, hawkers and all manner of informal business people .

These, plus farmers represent the broader spectrum of Uganda’s population which also needs to be protected against old age poverty! We have already requested NSSF to extend its coverage by creating products for the informal sector. The timing of the government in liberalizing the pension sector is not accidental.

It comes at a time when 70% of the population is 30 years and below they are joining the labour force. There should be financial cultural change so that when they retire in 25-30 years to come, they don’t suffer. They should start saving now. I would like to urge the National Organization of Trade Unions moving into the informal sector around the country, organizing workers into vocational groups which will participate in formal pension system.

Every nation needs a pool of long term local savings. Why disperse the funds in NSSF, Uganda’s only local pool of long term savings into many smaller funds? How will NSSF invest in the long term infrastructure bond that H.E the president has proposed, if in five years all the funds will be transferred out of NSSF by the members?

The contemplated Reform which introduces liberalization with new aspects allowing the transferability and portability of savings has been misrepresented as an avenue for capital flight from NSSF .NSSF has made long term investments based on its investment policy and actuarial projections which URBRA as a Regulator will protect and safeguard through the forthcoming Investment Regulations .In addition , the transferability and portability of savings shall be governed by another regulatory regime which shall ensure that the solvency margins required by NSSF to honor promises made to its members are not eroded.

In your view what are the risks of opening up the pension sector especially in a financially illiterate society like Uganda?

URBRA has not yet opened up the Pension Industry to new players because the Retirement Sector Liberalization Bill has not yet become law .We are presently licensing largely ,Retirement Benefit Schemes, Trustees ,Fund managers ,Custodians, Administrators who were in existence before the law establishing the Regulator was enacted in September 2011 .

The few new players who we have licensed are Financial Institutions that were already rigorously vetted and approved by Bank of Uganda and the Capital Markets Authority to participate in the Financial services sector. In addition ,the licensing regulations that have been promulgated so far have a high watermark which will not be easily attained by ” fly by night operators