Uganda’s banking industry in 2023 continued growing across all fundamentals such as deposits, lending, income as well as assets. It however grew slower than it did in 2022.

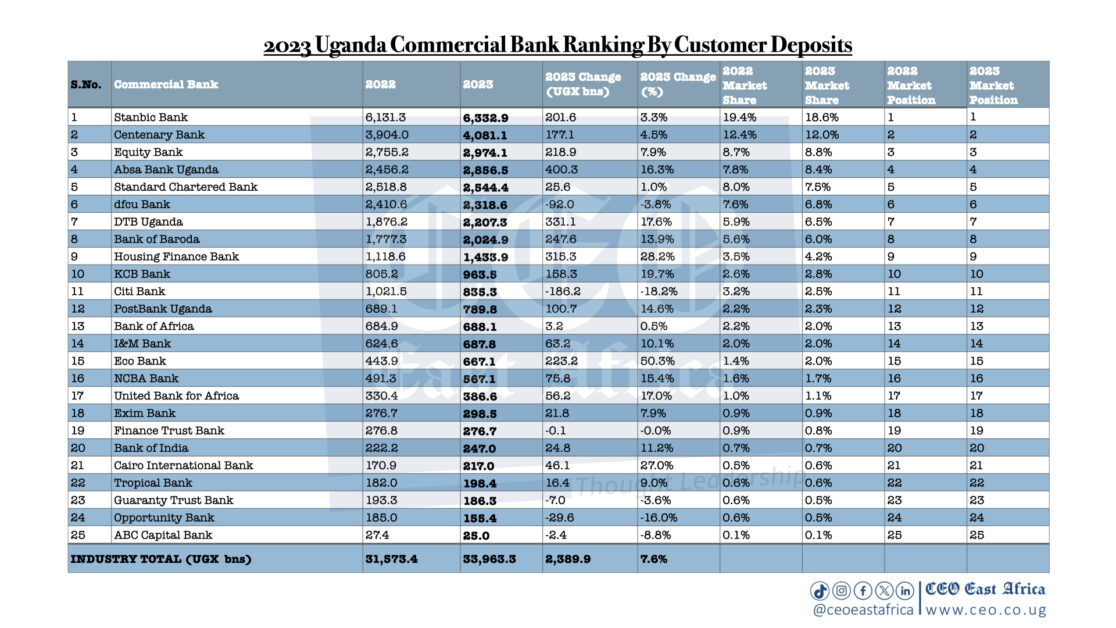

Total industry deposits grew by UGX2.4 trillion, from UGX31.6 trillion to UGX34 trillion⏤a growth of 7.6%. This was however a slower growth, compared to a 12% rise in 2022, when the industry grew from UGX27 trillion to UGX28.2 trillion.

Total lending grew by 7.5% from UGX19.1 trillion in 2022 to UGX20.5 trillion in 2023, a growth of UGX1.4 trillion. Although nominally, industry lending in 2023 grew more than it did in the preceding year, the 2023 growth rate was slower than the 11.3% growth rate registered in 2022.

Total industry assets also grew by 8.9%⏤ from UGX45.5 trillion to UGX49.5 trillion⏤ a growth of UGX4 trillion. This is much closer to the 9.9% registered in 2022. This is particularly because as banks slowed down lending to the public, they significantly increased lending to the Government by buying more treasury bills and bonds, as a measure against credit risk that remains high as marked by higher than usual Non-Performing Loans (NPLs).

Although industry NPLs eased down to 4.6% in 2023 according to BoU, they remain relatively higher compared to the 3.41% 6-year lows registered in 2018.

This strategy paid off for the industry especially as government borrowing appetite grew. The increased lending to the government, compensated for the reduced lending to the private sector and as a result, total income grew by 17.5%, from UGX5.8 trillion to UGX6.8 trillion⏤ a growth of UGX1 trillion. This growth rate is much faster than the 12.4% registered in 2022.

Although industry profits grew by 11.2% from UGX1.3 trillion to UGX1.4 trillion, the growth rate was again slower than the 19.3% growth rate in 2022. In 2022, commercial banking industry profits rose from UGX1.1 trillion to UGX1.3 trillion.

Industry ranking by bank

Govt Abandons Plan to Tax all Cash Withdrawals

Govt Abandons Plan to Tax all Cash WithdrawalsPaying specific emphasis on performance by individual banks, there were no significant changes in industry ranking from last year especially amongst the top 5 banks.

Stanbic Bank and Centenary Bank retained their positions as the first and second largest banks by deposits, lending, income, assets and profits respectively, albeit with mixed growth rates.

Absa Bank retained its 3rd position as the third largest bank by assets, thanks to its improvement from 4th to 3rd position as the largest lender. Absa also remained the 3rd largest bank by income and profitability while retaining its position as the 4th largest by deposits.

Equity Bank moved from the 5th to the 4th largest bank by assets, even though it ceded its 3rd position as the largest lender, settling for the 4th position. It however retained its 3rd and 4th positions as the largest bank by deposits and total income respectively. It however registered the largest industry loss of UGX18.8 billion, due to a provisioning of UGX191.2 billion for bad and doubtful debts.

Standard Chartered Bank eased from the 4th to the 5th largest bank position by assets. It also jumped three places to become the 5th in profitability while maintaining its 5th position as the largest by deposits and the 6th largest lender. It however slipped to 6th position, from 5th in total income.

Below are 5 graphics showing the full performance of all the banks by deposits, lending, assets, income and profitability.