Uganda’s banking sector has never been stronger on paper. And the Bank of Uganda’s latest Financial Soundness Indicators show why.

Banks, the indicators show, are heavily capitalized, flush with liquidity, profitable, and increasingly resilient.

Regulatory capital sits above 25% of risk-weighted assets, double the global standards.

Non-performing loans have fallen from 5.2% to 4.1% in a year, while liquidity coverage ratios have surged to an extraordinary 580%. Returns on equity remain a solid 16 to 17%.

In short, Uganda’s banks are safe, liquid, and among the most profitable in the region.

Yet behind this impressive stability lies a nagging paradox: credit expansion is weak, and the little lending that takes place is concentrated in consumption and real estate.

Very little goes to the core sectors of the economy, such as agriculture and manufacturing, the backbone of sound economic growth.

Credit without transformation

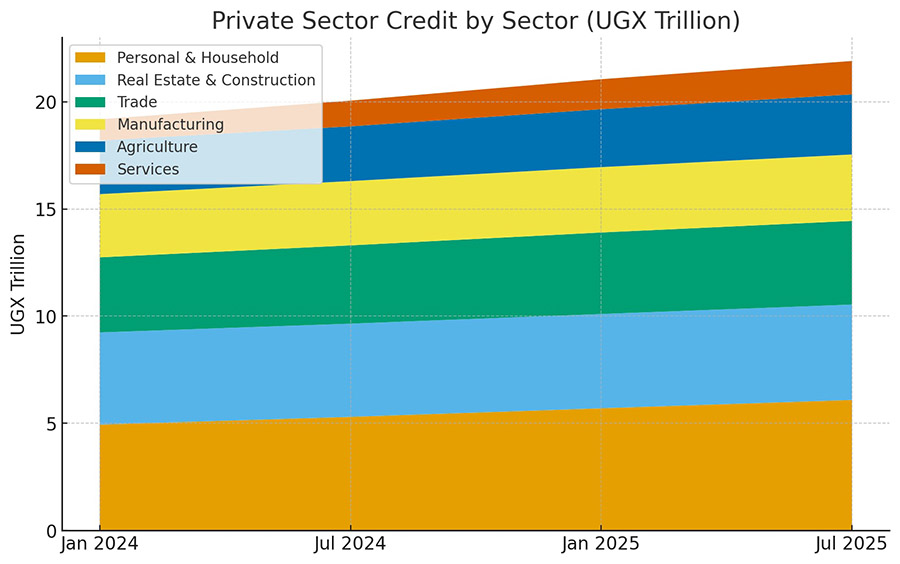

The Private Sector Credit Report covering January 2024 to July 2025 reveals the mismatch.

Personal and household loans grew from UGX4.9 trillion to UGX6.1 trillion, rising to over a quarter of total lending.

Much of this went into consumption, from non-durable goods to services.

Real estate followed closely, taking 19 to 20% of the credit pie, with commercial mortgages steadily growing.

Trade absorbed 15 to 17%, although retail lending shrank sharply in early 2025.

Agriculture, despite accounting for roughly a quarter of Uganda’s gross domestic product, stagnated with only 11 to 12% of credit.

Manufacturing fared little better, stuck at 12 to 13%, with food processing loans even falling.

The one bright spot was business services, which nearly doubled its share over the period, reflecting Uganda’s growing service economy.

The pattern is clear. Banks are happy to fund households and real estate, but remain reluctant to channel credit into sectors that could power structural transformation.

Why banks play it safe

This skew in lending has several explanations. Agriculture and SMEs are perceived as high-risk due to weather shocks, volatile prices, and weak collateral.

Consumer loans and mortgages, by contrast, provide high yields with lower monitoring costs.

Weak credit infrastructure, limited insurance penetration, and slow contract enforcement further discourage long-term lending.

Banks, already highly profitable, face little incentive to change. With safe returns from consumption lending and property, they prefer to play it safe rather than take on the uncertainties of farming or industrial ventures.

The outcome is a banking sector that looks strong individually but contributes only modestly to national economic transformation.

Related

Katikkiro Mayiga hails JCRC, Pearl Bank, Rotary over USD 4 million bone marrow facility drive

Katikkiro Mayiga hails JCRC, Pearl Bank, Rotary over USD 4 million bone marrow facility driveThe costs of the credit imbalance

The consequences are far-reaching. Uganda’s economic transformation risks being delayed if agriculture and manufacturing remain underfunded.

Household credit boosts consumption in the short term but adds little to productive capacity.

Credit concentration is another concern, with more than 60% of lending clustered in four categories: personal loans, real estate, trade, and manufacturing.

Most importantly, this lending pattern is at odds with Uganda’s Vision 2040 and the National Development Plans, which place agro-industrialization and export-led growth at the center of development.

This is not just a technical imbalance; it is a national economic challenge. A banking sector that prioritizes consumption over production cannot deliver the financial backbone Uganda needs to achieve middle-income status.

Glimmers of opportunity

Even so, there are promising shifts, with business services lending surging, which signals dynamism in Uganda’s service economy.

Within manufacturing, chemicals and pharmaceuticals are showing resilience, suggesting the possibility of diversification beyond food processing.

Growth in commercial mortgages points to more investment in business infrastructure rather than just speculative real estate.

These emerging areas, though small, highlight where Uganda’s financial system could pivot if incentives and risk-mitigation structures improve.

What needs to be done

Unlocking credit for transformation requires deliberate policy and innovation.

Strengthening risk-sharing mechanisms like the Agricultural Credit Facility could de-risk lending to farming and agro-processing.

Tax incentives may encourage banks to finance manufacturing and export-oriented projects.

Technology can also play a transformative role. Digital credit scoring, mobile banking platforms, and the use of alternative data could make it cheaper and less risky to assess small borrowers.

Expanding agri-insurance would provide further confidence for banks. Beyond banking, deepening Uganda’s capital markets is crucial.

More active bond and equity markets would share the burden of long-term financing.

Ultimately, banks themselves must balance short-term profitability with long-term national priorities.

By diversifying beyond household and real estate lending, they can reduce systemic risks while contributing meaningfully to Uganda’s development.

Strength without depth

Uganda’s banks today are stable, liquid, and profitable, but their lending patterns risk leaving the country’s growth ambitions underfunded.

The paradox is stark: a banking system with the capacity to fuel transformation is instead financing consumption.

If Uganda is to realize its ambitions of agro-industrialization and export-led growth, its banking sector must shift from safe bets to bold investments.

The true measure of banking success is not just how secure and profitable banks are, but how well they power the economy they serve.