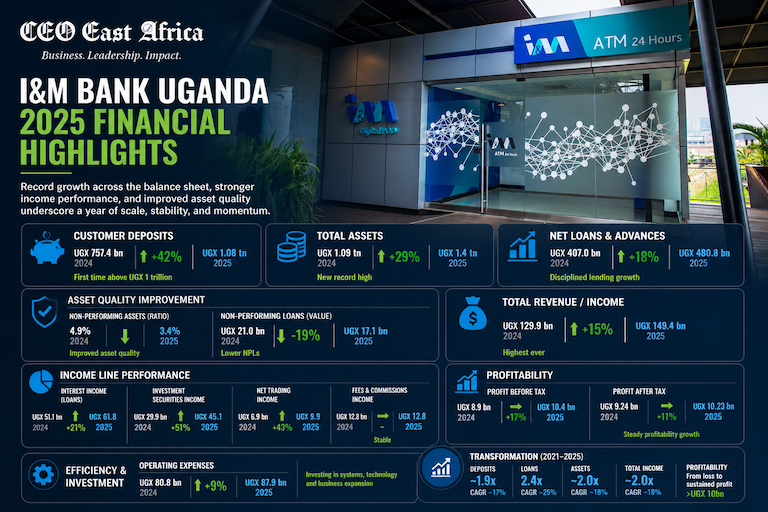

Since the rebrand to I&M Bank Uganda later that same year, the bank has more than doubled customer deposits from about UGX 574 billion to over UGX 1 trillion, expanded its digital and agency banking footprint, modernised its technology infrastructure, and repositioned itself as a far more ambitious regional banking player. Yet beyond the numbers lies a deeper story about leadership, culture, resilience, and the difficult realities of transforming a financial institution while still trying to grow it.

At the centre of much of that transformation has been Robin Bairstow, the Managing Director and CEO of I&M Bank Uganda, who previously led I&M Bank Rwanda before taking over the Ugandan operation during one of the most consequential periods in the bank’s history.

In this wide-ranging conversation with CEO East Africa Magazine’s Muhereza Abel Kyamutetera, Bairstow reflects on the bank’s transformation journey, the leadership lessons learned while rebuilding systems and culture simultaneously, the future of banking in an era of AI and fintech disruption, and why he believes East Africa’s next phase of growth will increasingly be defined by seamless movement of people, goods, and money across borders.

The conversation also explores I&M Brisk — the Group’s regional banking platform designed to simplify cross-border trade and transactions — as well as broader questions around trust, technology, regulation, talent, and the evolving role financial institutions must play in shaping the economies and societies they serve.

I&M Bank Uganda has undergone a remarkable transformation over the last four to five years following I&M Group’s acquisition of Orient Bank in 2021 and the subsequent rebrand to I&M Bank Uganda later that year.

Since then, the bank has more than doubled customer deposits from about UGX 574 billion in 2021 to over UGX 1 trillion in 2025, almost doubled its asset base, significantly expanded its digital and regional banking capabilities, and repositioned itself as a far more ambitious player within Uganda’s banking sector.

But I think away from the numbers, behind every strong set of figures, there is always a deeper story to tell. When you look at this journey personally — and the results the bank is delivering today — what excites you most about the transformation story behind those numbers?

Fundamentally, what excites me first is the growth in customer deposits and taking the bank beyond the UGX 1 trillion mark in both assets and liabilities. At the end of the day, banking is built on trust. Before you lend, you have to fund yourself, and the best way to fund yourself is through customer deposits.

One lesson I learned many years ago — and it has stayed with me ever since — is: fund before you lend, and earn before you spend. In many ways, that simple philosophy has guided a lot of what we have been trying to build over the last five years since I&M Group acquired the bank.

Over the last three years in particular, we have really started to see the direction moving the right way. Fundamentally, as a bank, we need to grow our customers and grow deposits, and we have seen encouraging progress on both fronts.

But beyond the balance sheet, we also measure ourselves constantly through customer feedback and data. We pay close attention to things like our Net Promoter Score and how customers genuinely feel about the bank. That has been an important part of this journey as well.

One of the most encouraging things for me is that many of the clients who have been with the institution since the Orient Bank days have stayed with us throughout the transition. Not only have they stayed, but many have told us they like the direction we are taking. Some have even brought new customers to us — their friends, businesses, and networks.

Those are the things the numbers do not always capture: the human side of transformation, the trust people place in you, and the confidence they have in the journey you are taking as an organisation.

Interesting. And while there is the discipline of “earning before spending,” transformation on this scale also requires significant investment upfront.

Over the last two to three years, where have you deliberately invested — whether in technology, people, systems, culture, or customer experience — to help position I&M Bank into the institution we are seeing today?

Well, everything starts with getting the foundation right. When you are building or transforming an institution, the foundation matters.

One of the earliest commitments we made after the acquisition was around technology and infrastructure. A major part of the investment over the last few years has gone into modernising the bank’s technology ecosystem and creating a platform that could support long-term growth.

We started by rebuilding the bank’s core infrastructure. At the time, we were operating on a single database with no redundancy. We moved from that to two fully-fledged data centres, both located here in Uganda, which was important for us from both resilience and data protection perspectives.

Once the infrastructure was in place, we then focused on upgrading the software and systems layer. We implemented a new core banking system capable of supporting scale and future growth. Today, banking is heavily API-driven, so we needed a platform that could integrate seamlessly with digital services and future innovations.

We also strengthened controls, particularly on the treasury side of the business. Treasury can generate strong returns, but it is also an area where banks can lose money very quickly if controls are weak. So we invested significantly in automated controls, monitoring systems, and risk management processes that support both the back office and middle office from a market-risk perspective.

Then we moved to the customer-facing side of the business. We upgraded the operating environment for our tellers, redesigned our internet banking platform, improved the mobile banking experience, and modernised our ATM infrastructure. In fact, within about 45 days, we rolled out an entirely new ATM network, recarded our customer base, changed our switch provider, and migrated from Visa to Mastercard.

Some of these investments are not always glamorous from the outside. I was joking with my team recently that one of our servers — essentially just a small box with flashing lights — costs as much as two Bugatti Veyrons and a Porsche combined. Now, a Porsche or a Bugatti is exciting to look at; a server box is not. But that is the reality of the kind of investment required to build a modern banking institution.

And ultimately, none of this happens without people. You can have all the strategy and ambition in the world, but transformation of this scale requires committed teams. We have been fortunate to have an exceptional group of people driving this journey across the organisation.

And looking at the numbers, I’m sure shareholders must be happy with the growth and returns the bank is delivering. But sometimes, from a customer’s perspective, people look at strong banking results and ask: “The bank is doing well — but what does that actually mean for me as a customer?”

So when customers look at these numbers, what should give them confidence or make them feel encouraged that I&M Bank is genuinely becoming a better institution for them as well?

If I look at where banking starts, banks are fundamentally measured on a few key things — net interest margins, impairments, and return on equity for shareholders.

Now, you can charge very high fees and make strong short-term returns, but that does not necessarily create sustainable growth or long-term customer trust. On the other hand, you can also lend aggressively to everyone and grow quickly, but then you expose yourself to high impairments and bad loans.

Our responsibility as leaders, together with the board, has been to strike the right balance — making banking cost-effective for customers while still maintaining strong risk discipline. That balance is critical because if your impairments become too high, ultimately those costs are passed back to customers one way or another.

One of the encouraging things for us is that our impairments are now below 3% on a gross basis, and we expect them to fall below 1% on a net basis this year. That gives us room to responsibly expand our risk appetite and support more customers and sectors going into 2026 and beyond.

But beyond the numbers themselves, customers should look at the investments we have made in making banking simpler and more efficient. We constantly study what the best banks around the world are doing — whether in Uganda, across Africa, Europe, or the US — and one thing is consistent: the institutions that succeed are the ones that make it easier for customers to do business.

That has been a major focus for us. We have invested heavily in technology, customer experience, and operational efficiency to make banking faster, more seamless, and more accessible. At the same time, we have also improved the systems our staff use internally so they can serve customers more effectively — whether it is retrieving records, processing transactions, or responding faster to client needs.

Ultimately, the growth in revenue, assets, and deposits is really a reflection of customers responding positively to a better banking experience.

And one thing that stands out when you look at the numbers — especially the deposit growth — is that the bank has grown customer deposits from about UGX 574 billion in 2021, around the time of the acquisition and rebrand, to over UGX 1 trillion in 2025. Even between 2024 and 2025 alone, deposits grew quite sharply from roughly UGX 757 billion to over UGX 1.07 trillion.

Yet, despite that growth, the bank does not appear to have pursued a major physical branch expansion strategy over the same period. To the best of my knowledge, apart from the new headquarters branch here, we have not really seen a significant rollout of new branches.

So how have you been able to deliver that level of growth without dramatically increasing the branch footprint? And does that perhaps say something about how banking itself is evolving beyond the traditional branch model?

One of the biggest drivers has been the expansion of our agency banking network. A few years ago, our penetration there was almost negligible, but today we are close to 3,000 agents across the market.

More importantly, we have continued expanding the range of products and services customers can access through those agents, and that integration has been exceptional for the bank. It has allowed us to extend our reach and convenience without necessarily relying only on physical branches.

At the same time, we have also leaned heavily into technology. Customers increasingly want to bank on their own terms and at their own convenience. For example, many customers told us they wanted the ability to make deposits 24 hours a day, so we invested in cash deposit machines across several locations. We are now also looking at expanding more automated and digital banking services into off-site locations closer to where customers actually are.

And the results have been very encouraging. In one case, a branch moved from virtually zero to about UGX 8 billion in deposit collections within a single month after the introduction of new cash deposit machines.

Technology has evolved to a point where the experience is almost instant. The moment a customer deposits money into the machine, the funds are reflected immediately in their account — even if it is 11:55 pm on a Saturday night. Physically, the bank may only process that cash on Monday morning, but from the customer’s perspective, the money is already available in real time.

I think that speaks to where banking is going. Customers still value branches, but increasingly they value accessibility, convenience, speed, and the ability to bank whenever and wherever they want.

So, when you look at the bank’s journey since the acquisition in 2021, how would you describe the phase I&M Bank Uganda is currently in today?

Were the last four to five years primarily about rebuilding and laying the foundation? Are you still in a growth and transformation phase? Or do you now feel the institution is entering a different stage altogether — perhaps one focused on scale, regional ambition, and the next level of expansion?

I think we are very much still in a growth phase. Across the I&M Group, we operate within a shared strategy cycle, and this year is actually the third year of our current strategic cycle.

The priorities and drivers of growth today may be slightly different from where we started immediately after the acquisition, but the direction remains very clear — we are still building, scaling, and growing.

At the moment, if you look across the key areas of the business, we are growing at a compounded annual growth rate of just under 20%. At that pace, the bank would effectively double in size within about five years. Of course, our competitors are also growing, but we are confident about the trajectory we are on.

The journey has really happened in phases. First came the investment phase — rebuilding systems, infrastructure, technology, and capabilities. Then came consolidation, stabilising the institution and embedding the transformation. And now we are moving into the next phase, which is about accelerating growth and improving returns.

Naturally, shareholders expect to see stronger return-on-equity numbers over time, particularly into the early 20% range, which is where many leading banks in the market operate. But what has been encouraging for us is that, despite the transformation work and constraints we have had to navigate over the last few years, we have still managed to outpace the market in terms of growth across assets, liabilities, and revenues.

They say one of the keys to growth is understanding exactly where your strengths and weaknesses lie as an institution.

So if I put a metaphorical gun to your head and asked you to point to one or two things about I&M Bank that you would almost “die standing for” — things you genuinely believe the bank does exceptionally well and would defend without hesitation — what would those be?

If I had to point to one thing, it would be our people. We genuinely have an exceptional group of people across this organisation. And yes, there are talented people across the industry, but what I believe has stood out for us is the level of resilience our teams have shown throughout this transformation journey.

When you think about it, we were changing our core banking system while also relocating our head office at almost the exact same time. Those are major operational shifts on their own, yet our teams continued pushing forward through all of it.

And because we are very data-driven as an organisation, we measure these things closely. We constantly track staff engagement levels, and what has been remarkable is that despite the pressure, the pace of change, and the reality of always having finite resources, our staff engagement scores have continued improving year after year. In fact, we are now benchmarking at levels comparable to some of the top organisations globally from an employee engagement perspective.

For me, that matters because engaged employees create engaged customers. They serve better, collaborate better, innovate better, and ultimately perform better.

That is probably the one thing I would go to my grave defending about this organisation — the quality, resilience, and commitment of our people.

I’m sure when people look at transformation stories from the outside — especially after the results start coming through — everything can appear smooth, well planned, and even glamorous.

But behind every successful transformation are usually difficult conversations, uncomfortable decisions, pressure, uncertainty, and moments where things could easily have gone wrong.

As someone who has been leading teams through this journey, what has that experience taught you personally about leadership? And in your view, what really makes great teams succeed, especially during periods of intense transformation and change?

Honesty, integrity, and openness. At the core of every strong team, there has to be trust.

There is a very good book called The Speed of Trust, and I have always treated it almost like a leadership manual. The central idea is simple: when people genuinely trust one another, organisations move faster. If I trust someone to do their job properly, they will usually deliver better and faster. But if everybody is constantly checking everybody else, the organisation slows down.

Trust also creates agility, and agility has become one of the key behaviours we have tried to build into the organisation. It allows teams to innovate, adapt quickly, and make decisions with confidence.

But one of the things I was very deliberate about when I arrived was that we could not pretend everything was perfect. There is a fine line between positivity and what I call “toxic positivity” — where people ignore obvious problems and simply keep saying everything is fine.

Early on, I spent time meeting staff across the organisation — more than 300 people in small group sessions and individual conversations. And one of the first things we told people was: things are not great right now, but we are going to make them better.

At the time, customer complaint levels were high. In fact, before I even arrived in Uganda, people were already writing to me from Rwanda saying, “You’re coming to Uganda — you need to know these are the problems customers are facing.”

We knew there were real issues within the organisation. But once we brought those problems into the open and started addressing them honestly — saying, “This is broken, this is how we are fixing it, and this is what comes next” — people started believing that transformation was actually possible. That created confidence and momentum internally.

Another difficult leadership lesson is the discipline of staying true to your strategy, especially under pressure. Sometimes opportunities come along that may look attractive commercially, but they do not fit your risk appetite, your values, or your long-term direction. And as leaders, you have to be willing to say no.

One principle my team and I have always believed in is that we never want our competitive advantage to come from weak compliance or taking risks we should not be taking. Lack of compliance cannot become a market differentiator.

We have to remain a disciplined and compliant institution, operate within regulations, and make decisions that are aligned with our values and behaviours — even when that is the harder path to take.

I was actually going to ask about that balance. Because I’m sure there is pressure to grow from every direction — from shareholders, from the market, and probably even from yourself personally. But at the same time, you still have to manage risk carefully, which you’ve partly touched on.

And going back to what you mentioned earlier — about people already writing to you before you even arrived — I’m sure there must have been a lot going through your mind at the time.

If the Robin of then met the Robin of today, what do you think the Robin of today would tell that Robin who was walking into the organisation back then?

Stay true to yourself.

At that stage, one thing I strongly believed was that we had good people in the organisation because I had already spent time meeting them. Secondly, we had a clear plan for what needed to be done — closing the gaps, fixing the problems, automating processes, simplifying customer experiences, strengthening sales, and building the institution we wanted to become.

People often use the metaphor of changing an aircraft engine while the plane is flying. But in our case, it felt like we were changing not just the engine, but also the landing gear, the wings, the tail, and the fuselage — all while still keeping the plane in the air and moving forward.

And when you look at that against the growth we have still managed to achieve over the last five years, it becomes even more significant because all of this happened alongside major organisational change. We had leadership transitions, changes at the middle-management level, people retiring, internal promotions, and teams adapting to a completely new direction. Yet despite all of that, we still managed to deliver on the objectives we had set ourselves.

For me, that reinforces an important leadership lesson: transformation is never about one individual. It only works when you have strong teams and people willing to believe in the journey.

I sometimes think about those old war images where the officers are standing at the front of the trenches, but right behind them are teams of people supporting them. It would be impossible for an executive team to lead from the front if nobody behind them believed in where the organisation was going.

We have been fortunate to build a very strong leadership team supported by committed people across the organisation, and that has made a huge difference in this journey.

If you were to someday write a book — much like you mentioned your chairman has done — and one chapter focused specifically on the transformation journey of I&M Bank Uganda, what do you think that chapter would say about leadership, people, and building institutions?

And I ask that because even recently, when I was in Kigali, Rwanda, I spoke to the I&M Bank Rwanda CEO there, who told me very clearly that part of what he is building today is based on the foundation you left behind.

So across your journey — not just here in Uganda, but within the wider I&M Group and your broader leadership experience — what are some of the key leadership lessons you have really “banked”, so to speak? What kind of lessons would you want upcoming leaders, executives, or even fellow CEOs to take away from your experience?

One of the things I’ve been fortunate about is that I’ve now spent over a decade within the I&M Group, working both here in Uganda and previously in Kigali. And before I even get to the personal lessons, I think it’s important to understand something about the organisation itself.

At its core, I&M still carries the values and heart of a family-owned business, even though it has all the structures and hallmarks of a successful corporate institution. Once trust is established, leadership is given the latitude to make decisions, build teams, and execute strategy, knowing there is support behind them. That makes a big difference.

On a personal level, I was given some very good advice early in my career. And while continuous education is extremely important — because we all need to keep learning and improving our skills — career growth is not only about qualifications or working late into the night on exams, assignments, or a thesis.

The real differentiator, in my experience, is involvement.

First, obviously, you have to deliver on your objectives. But beyond that, get involved in your organisation. Participate in projects, contribute ideas, volunteer for initiatives, engage in CSR activities, and put yourself forward for things outside your immediate job description.

That is how people begin to notice you. They remember the person who contributed meaningfully to a project, who brought a good idea to the table, or who stepped up when needed.

Today, because of platforms like WhatsApp and email, people reach out directly all the time. I get unsolicited messages from individuals looking for opportunities, and while I may pass those along to HR, I still notice something important: the initiative it took for someone to make that effort.

I think that has probably been one of my biggest lessons around leadership and career development. It is not enough to simply do your job well because, realistically, most people come to work intending to achieve their objectives. The difference often comes from doing a little bit extra and becoming genuinely involved in the organisation.

Once that happens, work stops feeling like “just a job” and starts becoming something bigger and more meaningful.

Yeah, interesting. Let’s talk about I&M Brisk because the Group has positioned itself as the best regional banking partner for people doing business across Eastern Africa.

And personally, I’ve had my own experience with the product — whether in Nairobi, Kigali, and hopefully Dar es Salaam next. The experience has actually been quite seamless.

But for people who may not fully understand it yet, first explain to us: what exactly is I&M Brisk? And when you were conceptualising and building it, what problem were you trying to solve for customers across the region?

Let me give you a practical example. I still have an account in Rwanda, including a credit card there, and recently, while visiting Kigali, my payment was due. Now, the last thing I wanted was to become the former CEO who ends up on the non-performing loans list.

Previously, making that payment would have involved a fairly long process. I would probably have had to initiate a SWIFT transfer, go onto the app, convert currencies, move funds between accounts, and wait for the transaction to clear across different systems.

But this time, I simply walked downstairs into the banking hall here in Uganda, wrote down my Rwandan account details, deposited the funds, and the money reflected instantly in Rwanda.

And that is really the essence of I&M Brisk. The counters in Uganda effectively become counters for Rwanda, Kenya, and Tanzania. Equally, the counters in Kenya become counters for Uganda, Rwanda, and Tanzania.

What we were trying to solve was a real business and customer pain point around cross-border banking and the movement of money within East Africa.

Think about a customer whose truck is sitting at a loading point waiting for cement or goods to be released, but the payment is delayed somewhere in the banking system because funds are being routed through multiple correspondent banks, maybe through New York, while people try to trace transactions. That creates delays, frustration, and inefficiency for businesses.

With Brisk, a customer can walk into an I&M branch in Kenya, deposit money, and have it instantly credited into an account in Uganda, Rwanda, or Tanzania the same day.

In many ways, it changes the meaning of what a branch network is. Instead of having just the branches physically located in Uganda, our customers effectively gain access to a regional network of close to 300 branches across East Africa.

And ultimately, that is the bigger vision behind Brisk. East Africa is already moving toward greater regional integration. We are increasingly able to move goods and people across borders more seamlessly. What Brisk is doing is helping make the movement of money just as seamless across the region.

And I’m sure I&M Brisk is probably just one part of a much bigger ecosystem of solutions designed to make trade, transport, payments, and regional business easier across East Africa.

Beyond Brisk itself, what are some of the other products or capabilities within the I&M Group that are helping businesses and individuals move, trade, and operate more seamlessly across the region?

Absolutely. Brisk works best as part of a broader ecosystem of banking and trade solutions across the Group.

A lot of it is built around connectivity, accessibility, and the ability for customers to access information and transact seamlessly wherever they are. Online banking itself is not a new concept — I was already selling internet banking solutions at Citibank when some of my current staff members were still in junior school. But the technology has evolved tremendously over the years.

Today, customers expect real-time visibility, instant access to information, and the ability to transact across borders without friction. That is why products like our internet banking platforms and the On-The-Go application are so important, both for individual customers and corporates.

Beyond that, we also support regional trade through more traditional banking products such as guarantees, standby letters of credit, trade finance solutions, and cross-border payment capabilities. These remain critical for businesses moving goods, making payments, and managing transactions across multiple markets.

So Brisk is really complemented by a wider suite of digital, transactional, and trade-finance solutions that together make it easier for businesses and individuals to operate across East Africa.

And what has the market response been like so far to I&M Brisk, especially from businesses and customers that operate across multiple East African markets?

The response has been phenomenal. A large number of our customers who already do business across the region and bank with us in multiple markets have embraced it very quickly.

One of the things customers appreciate is the flexibility. Whether it is Tanzanian shillings, Ugandan shillings, Rwandan francs, Kenyan shillings, or US dollars, the system is designed to support multiple currencies seamlessly across the network.

For example, a customer can walk into a branch here in Uganda and deposit Kenyan shillings directly into their account in Nairobi or elsewhere in Kenya. That simplicity has resonated strongly with customers operating regionally.

We also support many businesses that trade directly across borders or have partnerships, suppliers, and associates operating in different East African markets. For those customers, the ability to move money quickly and seamlessly within the region has been extremely valuable.

And when you look at cross-border business, there are obviously different layers to it — individual customers, SMEs, large corporates, traders, logistics players, and regional businesses.

Does I&M Brisk work across all those segments? And how have you seen different categories of customers using the platform across the region?

It really does not matter who you are. If you have an account within the I&M network, you can use the platform. Whether you are an individual customer, an SME, or a large corporate, you are able to deposit funds and credit your account from any of the participating markets across the region.

In the same way, third parties can also make deposits into customer accounts from any I&M branch across the network. That flexibility is what makes the solution powerful, especially for customers operating across borders or dealing with regional suppliers, partners, and clients.

And I remember during an interview with Zahid Mustafa, the I&M Bank Tanzania CEO, he spoke about one of the advantages I&M has built as a regional group — especially for businesses operating across multiple East African markets — being the ability to structure and support facilities across borders.

So if I’m a corporation with operations in Uganda, Kenya, Tanzania, or Rwanda, how does being present across those markets make it easier for I&M to support my business regionally?

It really becomes a unique advantage for us as a regional bank.

For example, a business may not yet have a long operating history with us in Uganda, but we may already know them very well in Kenya or Tanzania. Because we operate as a connected regional group, we are able to leverage that existing relationship, credit history, and performance track record when supporting them in another market.

In some cases, a customer may have a very established business in one country but only a smaller operation in another. Through the Group structure, we are also able to look at things like securities and collateral held in one market and use that broader relationship to support the customer regionally.

So it is not just about moving money across borders. It is also about leveraging regional knowledge, relationships, credit understanding, and even securities across the different markets where we operate.

The other important part is that our teams across the region actively work together. We have formal structures and forums through which the different entities coordinate business referrals and regional customer relationships. We also have a dedicated regional business head based in Kenya whose role is to ensure that customers operating across markets receive a consistent level of service across all the entities.

That makes cross-border banking and regional business much smoother for customers because they are dealing with a connected ecosystem rather than isolated country operations.

And from what you’re saying, once you start operating across multiple jurisdictions, there are obviously different regulatory environments, banking rules, and legal frameworks involved.

From your perspective, are there still areas where policy, regulation, or regional integration frameworks could evolve further to make cross-border banking, trade, and movement of money even smoother? Or do you feel the ecosystem is already working fairly well as it stands today?

No, actually, I think the region has made significant progress over the years. From a trade perspective, having a single customs platform across the East African markets has already made cross-border business much easier than it used to be. The movement of people is also far less restricted today, which is important because talent and expertise move across borders as well.

Within the Group, for example, we regularly share expertise across markets. Depending on the need, we may bring in people from Rwanda, Tanzania, or Kenya, and we have also had senior staff permanently relocate across borders within the region. That exchange of skills and experience has been very valuable.

On the regulatory side, while each central bank operates independently within its own country, the regulators engage with one another quite closely. In fact, we have participated in what are called regulator colleges, where regulators from Kenya, Rwanda, Mauritius, Tanzania, Uganda, and other markets come together to review the Group, discuss regional operations, and look at issues like capital adequacy, systemic importance, and regulatory alignment across the different jurisdictions.

So generally, there is already a high level of cooperation and coordination happening across the region.

If there is one area where I think some markets could evolve further, it is around the treatment of technology and software investments. Banking today is increasingly digital, and software infrastructure is expensive regardless of the size of the organisation.

In Kenya, for example, the regulatory approach has been a bit more forward-thinking because investments in software are treated in a way that better supports digital transformation. In some other jurisdictions, when you invest heavily in software, it becomes classified as an intangible asset that effectively reduces your capital position, almost penalising you for investing in technology.

Yet those investments are exactly what drive digitalisation, automation, efficiency, and better customer experiences in modern banking. So I think that is one area where continued evolution in the regulatory framework could further accelerate innovation across the region.

You know, people often say banking is one of the best barometers of what is happening in an economy. Through deposits, lending patterns, transactions, and customer behaviour, banks almost get a real-time feel of where confidence is rising, where business activity is slowing, where people are investing, and even where uncertainty exists.

In fact, someone at MTN was recently telling me that just by analysing transaction data, they can tell where harvesting seasons are happening, where it is raining, and even which business corridors are becoming more active.

So when you look at the data flowing through the banking system — because I imagine you are looking at these trends constantly — what are you seeing in the economy right now? Where do you see the biggest opportunities emerging? And as the country gradually moves beyond some of the uncertainty that often surrounds pre-election and post-election periods, what excites you most about Uganda’s economic direction at this point in time?

When you look at the data over the last few years — particularly coming out of the post-COVID period — there was a stage where the economy was showing strong GDP growth, but that growth was not necessarily filtering down broadly across the population.

Sometimes headline economic growth can be misleading. You can have sectors performing strongly, but the benefits are not immediately reaching ordinary people in a meaningful way.

What I am beginning to see now, however, is more evidence of that growth gradually trickling through into the wider economy, particularly in areas where we are seeing sustained investment and stronger revenue inflows.

Coffee, for example, has performed exceptionally well over the last couple of years. Oil and gas continue progressing steadily, and I actually liked the way the Minister explained the timelines around first oil. She said it is a bit like expecting a baby — you generally know the period, but nobody can give you the exact date with complete certainty. It may come slightly earlier or slightly later, but the direction is clear.

I also think the government’s broader growth agenda — including the 10X strategy and investments across sectors such as science and technology, mining, agriculture, tourism, and infrastructure — is beginning to create a stronger platform for long-term economic expansion. Some of those sectors are already contributing meaningfully, while others still require further development.

Tourism, in particular, has enormous potential, especially alongside investments like the airport expansion and broader efforts to improve the country’s attractiveness to international visitors. I remember when I first arrived in Uganda, one of the major tourism headlines involved security incidents in one of the national parks, which was a very unfortunate period. But over the last few years, we have seen much greater stability and stronger law-enforcement visibility, which has helped rebuild confidence in the sector.

Agriculture also remains critically important to Uganda’s economy. Historically, we have relied heavily on rainfall, but increasingly the conversation is shifting toward longer-term solutions such as irrigation, storage infrastructure, and reducing dependence on unpredictable weather patterns.

And beyond that, the opportunities emerging around oil and gas are significant. The country is gradually moving from the construction phase toward extraction and eventually into maintenance, services, and the wider ecosystem that develops around the sector.

We see many of these shifts directly through the customers we bank with. We work with oilfield service companies, coffee exporters and producers, hotels, tourism operators, and businesses across several sectors, so we get a fairly real-time sense of where momentum is building within the economy.

You mentioned earlier that you were already selling online banking solutions at Citi when some of the people now working at I&M Bank were still in junior school, which says a lot about how much transformation you have witnessed firsthand.

But where we are today feels very different. Banking is moving incredibly fast — digitisation, mobile technology, AI, fintechs — and increasingly the bank itself is sitting inside the customer’s phone.

I remember asking a former MTN CEO a few years ago whether he would be surprised if, somewhere down the road, you eventually saw telecom companies and banks deeply integrating parts of their businesses, or even merging certain functions, because the lines between industries are becoming increasingly blurred.

So, in your own assessment, five to ten years from now, where do you honestly see banking going?

There are a couple of things happening at once.

First, when telecom companies initially started moving into financial services, many banks — and I have to include myself and my generation in this — reacted defensively. Banks ran to regulators, saying, “Please stop this.” But if you look back now, mobile money has done an incredible job in driving financial inclusion across Africa.

I think what has changed over time is that the industry has become less focused on competition and much more focused on collaboration. Banks and telecoms now understand that there are areas where we complement one another. At the end of the day, someone still needs to provide liquidity, lending products, capital, and the infrastructure that supports financial ecosystems.

So rather than fighting fintechs and telecoms, the conversation today is increasingly about partnerships and integration.

The other major shift, of course, is artificial intelligence. AI is one of those terms everybody is throwing around right now. I saw a meme recently where a group of CEOs are chanting: “What do we want? AI. When do we want it? Now. Why do we want it? We don’t know.” And honestly, there’s probably some truth in that.

But beneath the hype, AI is going to fundamentally improve how financial institutions use data and make decisions. Banking generates enormous amounts of information, but there is always noise within the data. AI gives us the ability to analyse patterns more intelligently, improve decision-making, strengthen risk management, and understand customers much better.

It will also automate many repetitive tasks. I genuinely believe banks that effectively adopt AI will outperform those that do not.

At the same time, the lines between banks and fintechs are going to continue blurring. Fintech growth has not slowed down, and disruption in the industry is still accelerating.

I was recently looking at Capitec Bank in South Africa. They started with about 25,000 customers in 2002 and now have more than 25 million customers, making them the largest bank by customer numbers in the country. You are also seeing the rise of digital-first neo-banks expanding across multiple markets globally.

So yes, disruption will continue. There will always be a role for traditional banks, but the sector itself is evolving very quickly. Increasingly, you are seeing movement of talent between banks and fintechs — bankers joining fintechs, fintech professionals moving into banks — and that crossover is only going to grow.

I don’t think the future of financial services is shrinking; I think it is evolving. Some traditional banking roles may reduce over time, but entirely new opportunities will emerge around technology, AI, data science, digital products, cybersecurity, and financial infrastructure.

So for young people studying finance, accounting, engineering, or technology today, I actually think the future remains very exciting. If we need fewer traditional accountants in some areas, we will need more data scientists and digital specialists in others.

Five to ten years from now, I still believe financial services will remain one of the most dynamic and innovative industries to work in.

And for somebody watching this conversation — perhaps someone just starting out in banking or financial services and wondering whether they should pursue an MBA, study AI, move into data science, or specialise in another area — have you seen the industry’s demand for skills changing over time?

I’m sure there was a time when banks were looking for one type of talent, and today the market is probably looking for something quite different.

So when you look ahead, what are some of the skills or capabilities you think are becoming most valuable in banking today — and perhaps even harder to find in abundance?

Okay, I might influence a few young people negatively here, but some of the areas where we genuinely struggle to find enough talent today are compliance, anti-money laundering, cybersecurity, data science, and ESG.

Cybersecurity is huge. Data science is huge. And increasingly, it is no longer just about traditional IT skills. Today, we are looking for people who combine technology expertise with strong data and analytical capabilities.

Compliance and anti-money laundering expertise are also becoming critically important as the regulatory environment grows more complex. And another area where the sector still lacks enough depth is environmental and social governance — ESG — which is becoming increasingly important in modern banking.

Of course, there is still a strong demand for accountants; that shortage has probably always existed. But one thing people should understand is that banking is no longer just for accountants.

Today, banks employ engineers, people from natural sciences, technology backgrounds, humanities, and many other disciplines. The industry has become far more diverse than many people assume.

So if I can speak directly to young people watching this conversation, I would say the opportunities are definitely there — particularly in areas like cybersecurity, data science, compliance, ESG, and technology-enabled financial services.

I think that is all I have from my side. But before we close, is there anything you feel we may have left out — something important that perhaps does not get talked about enough, or even something you are personally passionate about that you would want people watching this conversation to take away from it?

From our perspective, one of the things that really defines I&M Bank is the importance we place on partnerships and ecosystems. A lot of what we do is built around working closely with our customers, businesses, and communities rather than simply operating as a standalone institution.

We are also very conscious of the role we play in society. Financial institutions have a significant responsibility — not just in terms of profitability, but in terms of expanding access to finance, supporting businesses, enabling growth, and contributing positively to the broader economy.

That is something we take seriously, and we try to approach what we do with a sense of responsibility and conscience.

And I think this is no longer just an I&M conversation. Across the industry globally, regionally, and locally — whether driven by regulators, central banks, governments, or the institutions themselves — there is a growing recognition that the financial services sector must operate responsibly and understand the impact it has on society.

Increasingly, the industry is moving toward a model where success is not only measured by financial performance, but also by how responsibly and sustainably institutions contribute to the communities and economies they serve.

Okay, alright. Robin, thank you very much for your time. It is always a pleasure coming here and having these conversations.

Hopefully, we will be back again very soon to continue unpacking some of these lessons around leadership, transformation, regional banking, and where the future of financial services is heading.

Thank you once again for your time and for sharing your insights with us today.