Uganda has spent years talking about digital transformation. It has built strategies around it, launched platforms around it, and anchored part of its long-term economic future on it.

But for millions of Ugandans, the first real step into that digital future still depends on something painfully basic: buying a smartphone. And that is where the contradiction begins.

While government is pushing a digital economy, the cost of entering that economy remains too high for many of the people.

The smartphone, now the gateway to digital payments, learning, e-commerce, government services, job search, and modern communication, is still priced like a consumer good rather than an essential economic infrastructure.

This is not just a household affordability problem. It is a national growth problem.

A market that is connected, but not fully digital

Uganda is not disconnected. Far from it. Uganda Communications Commission (UCC) 2025 fourth quarter report shows the country had 47.1 million active mobile subscriptions, 18.5 million mobile internet users

But only 20 million smartphones are in use, compared to 32.2 million feature phones and 6.1 million basic phones.

That single snapshot captures the structural imbalance, which shows that Uganda has built a communications market with massive reach, but it remains anchored in low-capability devices.

Millions can call, text, and send money. But millions still cannot fully participate in the richer, app-driven digital economy that policymakers and business leaders keep promoting.

The imbalance becomes even clearer when placed against network reach. Uganda has achieved roughly 96% 4G population coverage, yet only about 22% of the population are active mobile internet users, leaving a 75% usage gap.

This is not a supply problem. It is an access problem. And, as MTN submission puts it in the Pre-Budget Consultation Submission for the National Budget FY 2026/27, it shows that feature phones dominate because they cost less, not because people prefer them.

In quarter four of 2025, feature phones accounted for 61.7% of subscriptions, compared to 38.3% for smartphones, a gap that makes plain how far Uganda still is from becoming a truly smartphone economy.

That is why telecoms and industry players repeatedly call this a demand problem, not a supply problem. People want smartphones but cannot afford them.

Until fiscal policy addresses the affordability barrier, supply-side interventions will not close the gap.

The price of entry

The price of entry explains why. The Global System for Mobile Communications Association (GSMA) estimates that an entry-level smartphone in Uganda costs about $38.91 (UGX 146,757), equivalent to 39% of monthly GDP per capita, and a staggering 96% of monthly income for the poorest 40% of the population.

This burden becomes even clearer when placed against actual income realities.

Over half of Uganda’s working population earns a median monthly income of approximately UGX 200,000 (roughly $54), while the mean income across all working brackets is estimated at around UGX 327,988.

A significant 51% of the population earns less than UGX 150,000 monthly, according to data from the Uganda Bureau of Statistics.

In practical terms, this means that for a large share of Ugandans, buying even the cheapest smartphone requires committing between one or nearly an entire month’s income.

For those earning below UGX 150,000, the cost of a smartphone can exceed what they take home in a month, forcing households to either delay purchase, rely on cheaper feature phones, or divert income from essential needs such as food, rent, and school fees.

Even more striking, taxation accounts for roughly 35% of that cost, one of the highest burdens in Sub-Saharan Africa.

MTN, in its submission, quantifies the burden differently but reaches the same conclusion: Uganda applies a 10% import duty on smartphones and then adds 18% VAT, creating a 28% combined tax burden before the device even reaches the shop.

In other words, the state is not just observing the affordability problem. It is part of it. And that matters because the digital economy no longer lives inside offices or institutions. It lives inside the device in a person’s pocket.

The regional comparison makes the point even more starkly. It’s only Uganda that imposes a 10% smartphone import duty. Kenya, Tanzania, Rwanda, Nigeria, and South Africa charge zero.

Every comparable market supports digital services and smartphone adoption through lighter taxation, and markets like Kenya and Nigeria have seen explosive growth in digital participation and the tax revenues that follow.

That regional context matters because Uganda is trying to build the same kind of digital ecosystem.

That is why the affordability problem becomes even sharper when set against Uganda’s own policy ambitions.

The Tenfold Growth Strategy aims to expand the economy from $50 billion in 2023 to $500 billion by 2040, with a clear emphasis on building a knowledge economy driven by technology and innovation.

But that future depends on broad participation. And that participation depends on access.

Parliament’s Budget Committee has already warned that key sectors such as innovation, human capital development, and technology remain under-resourced relative to national ambitions.

This raises questions about whether the country is adequately investing in the foundations of its own growth strategy.

The contradiction runs through the entire fiscal framework. Uganda National Development Plan III set explicit digital transformation targets: internet penetration from 25% to 50%, entry-level smartphone cost from UGX 100,000 to UGX 60,000, and 80% of government services online.

The target price path was meant to fall steadily, from UGX 100,000 in 2017/18 to UGX 95,000 in 2020/21, UGX 87,000 in 2021/22, UGX 75,000 in 2022/23, UGX 70,000 in 2023/24, and UGX 60,000 in 2024/25.

But affordability remained a challenge even by the end of NDP III. NDP IV raises the stakes further.

For 2029/30, it targets internet usage rising from 20% to 45%, e-government satisfaction from 22.2% to 30%, digital skills from 26% to 36%, and mobile money and banking usage to 71%, rising to 100% by 2040.

Uganda, in effect, is trying to build the upper floors of a digital economy while the front door remains too expensive for millions.

The view from the market

That broad market picture is also visible from the shop floor.

Musa Kirunda of Mush Gadgets, a Kampala electronics dealer, says the tax pressure is immediate and commercial.

“We have less capital but pay more taxes on phones, this means I have to price them higher to customers to get a return from my business. When you increase the price, the sales drop. But at the same time, you’re competing with some people who don’t pay taxes or engage in smuggling of these phones,” he says

Most Ugandan phone dealers source their phones from Dubai, Kenya, or China.

Dubai is viewed as a cheaper option for sourcing phones; however, shipping costs and taxes remain high, while Kenya also remains preferred for cheaper phones.

Kirunda questions why government provides tax incentives to investors who already have cheaper sources of capital from their home countries.

“We’re already struggling with expensive loans from banks. And we have operating costs such as rent, electricity, and additional income tax,” he says.

Despite government’s push for the Buy Uganda Build Uganda initiative to promote local production, Kirunda argues that local assembly plants have contributed little to supply, as they remain focused on manufacturing basic and feature phones.

The smuggling reality

The pressure on smartphone tax is not just theoretical. It is visible at the country’s main entry point.

On December 19, 2025, URA customs enforcement officers at Entebbe International Airport disrupted a series of sophisticated mobile phone smuggling attempts, seizing 422 undeclared high-value smartphones worth $50,640 (approximately UGX 235.5 million) over three weeks.

Speaking on the seizures, Moses Kyomuhendo, the Manager of Enforcement and Border Control in the central region, said the anti-smuggling campaign sought to deter the growing trend of smuggling high-value electronics into the country.

He revealed that most of the seized devices originate from UAE and China, with high-end brands such as Samsung and iPhones dominating the consignments.

Some of the suspects have since been prosecuted, while others paid penalties and outstanding taxes.

The industrial policy trap

Uganda’s smartphone tax is defensible as an industrial policy. The nominal logic is that import duties protect local assembly and manufacturing.

However, local producers such as SIMI Technologies and MiOne are yet to meet existing demand, let alone the greater demand that would emerge if prices fell.

International manufacturers have not set up local plants because Uganda’s market is still too small to justify the capital investment. Mobile devices made in one EAC country still face tax barriers when crossing borders.

Over 3,000 Receive Free Eye Care at Ruparelia Foundation’s Bukedea Eye Camp

Over 3,000 Receive Free Eye Care at Ruparelia Foundation’s Bukedea Eye CampA UCC market assessment for January shows that a locally assembled smartphone costs on average UGX 630,000, which is almost double the price of some imported smartphones.

At the same time, only 1,866 locally assembled smartphones were active on the 4G network as of January 30, measured over six months from June 2025.

So the result is a circular trap: taxes are defended in the name of local industry, but those same taxes suppress the demand growth that could one day make local production viable.

That contradiction is sharper when placed against Uganda’s own industrial policy history. In November 2019, President Museveni commissioned Uganda’s first mobile phone and computer assembly plant, SIMI Mobile Technology, in Namanve Industrial Park.

Backed by Minister of State for Investment Evelyn Anite, the project was presented as a flagship of the Buy Uganda Build Uganda agenda, meant to promote local manufacturing, reduce import costs, save foreign exchange, and generate employment.

Operated by Chinese-owned ENGO Holdings, the plant was projected at full capacity to produce 2,000 feature phones, 1,500 smartphones and 800 laptops a day, along with accessories.

The ambition was not small. It was to prove that Uganda could assemble its own devices, serve rural ICT needs with solar-powered handsets, and begin reducing dependence on imports.

But that history also underlines the problem running through the current tax debate.

Local assembly was supposed to support affordability and scale. Yet the market remains overwhelmingly dominated by feature phones, while smartphones are still expensive for the majority.

Anite argued at the time that local production would make electronics more affordable, even citing devices around UGX 20,000, and later led efforts to position Ugandan-made phones for export to markets such as Morocco.

In 2021, a separate initiative involving CTI Africa, its arm LifeMobile, and the National Enterprises Corporation was also announced to assemble smart devices in Uganda.

The policy intent, then, has been consistent: build local production, expand access, and create jobs. The problem is that the tax structure has not moved in the same direction.

Why regulators agree

Julianne R. Mweheire, the director of economic regulation, content, and consumer affairs, frames the issue in even broader terms.

She argues that smart devices have become a critical tool of access and that “we cannot talk about digital inclusion without talking about the cost of devices.”

Uganda, she says, is pushing for a generation of smart devices such as smartphones with 4G and 5G capabilities, anchored on a long-term goal of driving high usage of 4G and 5G networks.

However, the challenge remains that the cost of devices in Uganda is significantly driven up by taxes, which range between 35 and 50% across VAT, import duty, and infrastructure levies.

These taxes substantially inflate the final retail price.

Mweheire raises a critical point. If an entry-level smartphone costs about UGX 250,000 inclusive of taxes, then without those taxes, it could fall to roughly $40 to 50 (UGX 150,903 to UGX 188,629).

That price shift could dramatically improve scale, usage, and overall utilisation of existing network infrastructure.

She points to a deeper structural mismatch where geographic network coverage exceeds device penetration, noting that smartphones are largely concentrated in urban areas where incomes are higher, while rural populations remain reliant on basic and feature phones.

Compounding this gap is unreliable electricity, which further limits the productive use of devices.

Drawing comparisons with other countries, Mweheire notes that higher electric grid penetration consistently correlates with higher smartphone usage.

She reduces the argument to a straightforward economic case. More people connected through smartphones means higher revenue for URA across multiple channels, including data usage, digital transactions, and taxes generated through smartphone-enabled services.

Increased smartphone usage also translates into higher corporate income tax contributions from telecom operators, alongside broader multiplier effects across the economy.

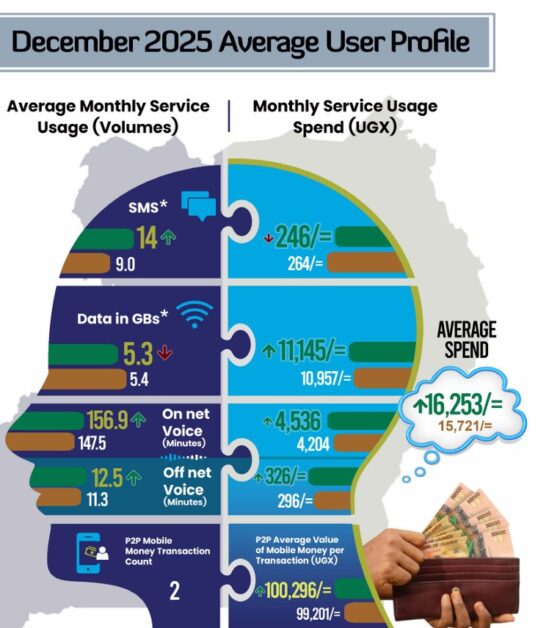

Meanwhile, UCC data shows average monthly data spend at UGX 11,000, with 47 million active customers, but only 18.5 million active data users.

That gap is not just about usage. It is about lost revenue. At current levels, 18.5 million users spending UGX 11,000 per month translates to roughly UGX 203.5 billion in monthly data revenue, or about UGX 2.44 trillion annually.

If even half of the remaining 28.5 million non-data users were converted into active data users at the same average spend, that would generate an additional UGX 156.75 billion per month, equivalent to nearly UGX 1.88 trillion annually.

If all active customers were fully participating in data usage, total annual data revenue could rise to over UGX 6.2 trillion.

This gap reflects the limitation imposed by device access.

Government has used initiatives such as shifting public services, including passports, company registration, and tax payments onto digital platforms to drive adoption and push users onto 4G networks.

Yet usage patterns remain shallow, with UCC data showing that 60% of internet consumption is concentrated on social media, while higher-value use cases such as education, research, innovation, and marketing remain underutilised.

Mweheire says this is exactly why UCC and other stakeholders have engaged the Ministry of Finance to restructure taxes on entry-level devices.

She notes that GSMA benchmarks an entry-level smartphone at $150, and the proposal presented suggests that devices at or below that threshold should not be taxed, while those above it can be taxed.

The objective, she says, is to induce demand in a market where feature and basic phones still dominate, despite significant investment in network infrastructure designed to support smart devices.

Even so, she cautions that the continued dominance of basic and feature phones is itself a signal of poor affordability.

These devices lack the capabilities required for full participation in the digital economy.

While URA has raised concerns about potential abuse, such as importers misclassifying devices as entry-level, Mweheire argues that safeguards already exist.

UCC and URA have agreed on the Central Equipment Identity Register, known as SimuKlear, which tracks imported devices, ensures compliance and enables proper tax application.

The system is also linked to GSMA to verify global device pricing.

She proposes that any tax exemption on entry-level smartphones could initially run for two years and then be reviewed.

“We made a presentation to the Ministry of Finance that we cannot achieve the NDP targets with the current tax regime on smartphones. We need a model where the earning potential of Ugandans matches device costs,” she says.

She also argues that whereas device financing has made inroads, it is costly to consumers.

There is also a revenue story behind the argument, and it is central to MTN’s case.

The company says it contributed UGX 6.177 trillion in taxes between 2015 and 2024, averaging about UGX 618 billion a year across VAT, local excise duty, and corporate income tax.

However, the company’s point is that government ultimately earns more from a growing digital ecosystem than from protecting narrow tax lines that make the ecosystem smaller.

The key insight is that ecosystem size, not just direct tax collections, ultimately determines total government revenue.

A thriving digital sector generates substantial corporate tax, VAT on services, PAYE, and broader economic activity. When taxes suppress ecosystem growth, they reduce the full range of tax revenues that flow from a healthy digital economy.

The case for business and innovation economy

Michael Niyitegeka, Refactory Executive Director, takes the argument beyond telecoms and into the wider economy. From a business perspective, he argues that there is a need for strong incentives to expand access to devices and internet connectivity.

Despite heavy investment in digital platforms, banks and fintechs are still seeing limited utilisation, even among users who can afford them, partly due to high internet costs as telecoms try to recover their investments.

Niyitegeka points to regional examples, noting that countries such as Kenya, Tanzania, and Rwanda have made progress by scrapping heavy taxes on entry-level smartphones.

“The internet is no longer a technology; it is a marketplace,” he says, where traders can set up online shops, reach global markets, and even ship products to Europe.

“We need more entrepreneurs to drive the digital economy,” he adds, arguing that usage must move beyond social media platforms like TikTok to more productive applications.

Niyitegeka highlights sectors such as tourism, manufacturing, and agriculture as areas that could grow significantly through better use of digital tools.

At the core of the problem, he says, is access. “We have a youthful population that needs to work. We’re trying to skill young people to do remote work, but they can’t access devices.”

In fact, he goes further, suggesting that if policy is to prioritise productivity, scrapping taxes on entry-level laptops may have an even stronger economic impact than smartphones, given their direct link to work and skills development