By Sharon Kyatusimiire

After more than four decades in insurance, a journey that began in 1984, Peter Makhanu speaks with the composure of a man who has seen cycles, crises, regulatory shifts, and technological revolutions reshape the industry from paper-based underwriting to artificial intelligence–driven claims processing.

“My journey in insurance began in 1984, shortly after college, when I joined Kenya Reinsurance Corporation, a reinsurance company. I spent 10 years there before moving to UAP, now Old Mutual, where I served for another decade.”

That grounding in reinsurance, the technical backbone of the industry, shaped his discipline early. A decade at Kenya Reinsurance Corporation was followed by another at UAP, sharpening both underwriting and commercial instincts.

“After that, I was approached by the Catholic Church to establish a new insurance company from the ground up. That greenfield venture became PACIS Insurance, and I led it for about 13 years, until 2017.”

Institution-building became his defining strength. By the time Liberty Group approached him in 2017, after acquiring East African Underwriters in Uganda, he was not simply a career executive. He was a builder.

“Later that year, Liberty Group, having just acquired East African Underwriters in Uganda, was looking for a CEO to drive the next phase of growth and transformation. I was invited to take up the role, and I have been with Liberty Uganda since 2017.”

What followed has been one of the more measurable transformation stories in Uganda’s short-term insurance market.

The numbers: A seven-year structural shift

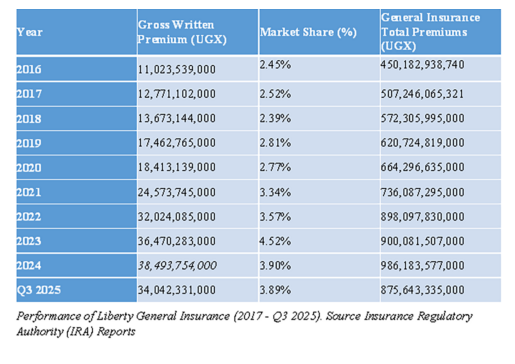

When Makhanu assumed leadership in May 2017, Liberty General Insurance was generating UGX 12.77 billion in Gross Written Premium (GWP), the lifeblood of every insurance company, and held a modest 2.52% share of the market.

Seven years later, by the close of 2024, that figure had climbed to UGX 38.49 billion, with market share expanding to 3.9%.

In absolute terms, Liberty added UGX 25.72 billion in premiums over the period.

The company effectively tripled its premium base, achieving a 3.01-times growth multiple and sustaining a compound annual growth rate (CAGR) of 17.1% between 2017 and 2024.

This performance becomes even more striking when placed against the broader industry backdrop.

Over the same period, Uganda’s general insurance market grew from UGX 507.25 billion to UGX 986.18 billion, an approximate CAGR of 10%.

Liberty, therefore, outpaced the market by roughly seven percentage points per year.

This was not growth by default or passive participation in an expanding sector. It was growth driven by deliberate competitive gain.

Decoding liberty’s performance under Makhanu

The first three years under Makhanu’s leadership were marked by steady, disciplined progression rather than explosive expansion.

When he assumed office in 2017, Liberty was writing UGX 12.77 billion in gross written premiums and held a 2.52% market share.

In 2018, premiums edged up to UGX 13.33 billion, followed by a stronger climb to UGX 15.61 billion in 2019. By 2020, the company had reached UGX 18.41 billion, with market share improving modestly to 2.77%.

Between 2017 and 2020, Liberty added approximately UGX 5.64 billion in premiums, a measured, incremental expansion that consolidated its footing in a highly competitive market.

The gains were deliberate rather than dramatic, suggesting a leadership approach focused on stabilisation, internal alignment, and strategic positioning before scale.

Then acceleration took hold.

In 2021, gross written premiums surged to UGX 24.57 billion, representing a 33.5% year-on-year increase.

The following year, growth remained robust, rising to UGX 32.02 billion, another 30.3% jump.

In just two years, Liberty added roughly UGX 13.6 billion in premiums, more than half of the total premium growth achieved between 2017 and 2024.

This period marked a clear turning point, the moment when small gains gave way to broader growth and the company’s competitive position was fundamentally redefined.

Market share moved in tandem with premium growth. From 2.52% in 2017, Liberty’s share climbed to 3.57% by 2022, eventually peaking at a reported 4.52% in 2023.

Although it normalised to 3.9% in 2024, the underlying repositioning had already occurred.

Liberty had moved from a modest player to a consistently near-4% competitor in a market of about 21 short-term insurers competing for scale and relevance.

The 2025 trajectory suggests that the momentum has not faded. By the end of the third quarter of 2025, Liberty had already written UGX 34.04 billion in premiums, equivalent to 3.89% market share.

With three quarters completed, the company had achieved nearly 88% of its full-year 2024 premium total of UGX 38.49 billion.

If cautiously annualised, the current run-rate points toward potential full-year premiums exceeding UGX 45 billion, implying a return to high-teens growth.

Taken together, the data suggests that the breakout years of 2021 and 2022 were not a temporary spike, but part of a broader structural shift in the company’s trajectory.

As Makhanu himself observes, “The insurance sector in Uganda is highly competitive.

We have about 21 short-term insurance companies, all competing for essentially the same market. That naturally creates intense pressure within the industry.”

In such an environment, he is clear that price wars alone cannot sustain growth.

“In such an environment, success cannot be driven purely by price. It must be anchored in the quality of service you provide and the level of innovation you bring to the market.”

Leadership defined by humanity and discipline

At the core of Makhanu’s leadership philosophy lies a distinctly human approach.

“At the core of my leadership are fairness, accountability and integrity. When you are leading people, you are dealing with human beings, not systems or machines, so fairness in how you treat them is essential.”

“Accountability is equally important; as a leader, you must take responsibility for your decisions and set the standard for others to do the same. Integrity is non-negotiable.”

Big Interview: How SBG Securities is Driving Uganda’s Investment Future

Big Interview: How SBG Securities is Driving Uganda’s Investment Future “Empathy also plays a critical role. People have emotions, personal challenges, and aspirations. Before making decisions that affect them, you must understand their circumstances and perspectives.”

Above all: “If you do not clearly articulate where the organisation is headed, people will lack direction.”

The performance record at Liberty reflects that long-term orientation. Growth has been compounded, not chased.

Beyond profit: Measuring institutional strength

For Makhanu, profitability is necessary, but insufficient.

“Beyond profits, I believe success begins with people. The most important asset any company has is its employees.”

“The second measure is customer retention. Are your customers staying with you over the long term, or are they constantly leaving?”

He extends that framework further: “Brand strength and innovation also matter … without innovation, you risk becoming invisible in a competitive market.”

And then impact: “Profit alone is not enough; a company must contribute positively to society.”

He cites Liberty’s Financial Fitness Academy, through which trained professionals deliver financial literacy training in workplaces, schools and communities.

“For me, true success is measured by engaged employees, loyal customers, strong brand relevance, continuous innovation and tangible societal impact.”

Industry headwinds: Talent, regulation and digitisation

“One of the most common challenges in this industry is talent. Insurance is a service business; it is driven by people, not machines.”

“Another ongoing challenge is navigating the regulatory environment … even a small compliance oversight can result in significant penalties or reputational damage.”

“And then there is digitisation. The industry is evolving rapidly … talent, regulation, and digital transformation are constant leadership priorities.”

Globally, he sees a decisive shift underway.

“Artificial intelligence is transforming operations, from underwriting to claims processing.”

He also highlights behavioural pricing.

“Telematics technology in motor insurance can track driving behaviour, how often someone drives, at what times, and in which locations.”

Yet digitisation brings responsibility.

“Data privacy is becoming increasingly critical … how insurers manage, protect and responsibly share client information will be a defining issue for the industry going forward.”

Penetration below 1%: The structural challenge

Uganda’s insurance penetration remains below 1%.

Makhanu identifies three core constraints.

“Insurance penetration remains low largely because of three interconnected factors: access, affordability and awareness.”

On access: “Much of the industry is concentrated in Kampala, yet significant economic activity is happening in regional centres such as Gulu, Mbarara and Jinja,” he says.

On affordability: “Flexible, well-priced products are essential to widening uptake.”

On awareness: “When people recognise that a relatively small premium can shield them from significant loss, their perception changes.”

Trust, he argues, is often lost at onboarding.

“We must thoroughly explain what the policy covers, what it does not cover, and concepts such as excess.”

“Ultimately, rebuilding trust comes down to transparency and education.”

Looking ahead: The next decade

Despite structural challenges, he remains optimistic.

“I see a thriving and expanding insurance sector over the next decade.”

Drivers include oil and gas, bancassurance growth, professional training and expanding regulation.

“When individuals take out bank loans to purchase property, they are often required to insure those assets. This process gradually builds a culture of insurance.”

By Q3 2025, Liberty had already written UGX 34.04 billion in premiums, with 3.89% market share.

If annualised cautiously, that implies a potential full-year trajectory above UGX 45 billion, representing possible high-teens growth over 2024.

“What gives me hope is the steady improvement in people’s livelihoods.”

“Anything of value requires protection.”

After more than 40 years in insurance, from reinsurance foundations in 1984 to leading Liberty through a 3x premium expansion, Makhanu embodies both institutional memory and forward-looking execution.

For him, insurance is not merely a product. It is an enabler of economic progress.