Stanbic Bank Uganda has for years stood tall as the country’s largest and most profitable commercial bank. From balance sheet dominance to steady profit leadership, the bank has long held the crown in Uganda’s financial industry. Yet, beneath the surface of consistent profits lies a shifting competitive landscape. The once clear lead is steadily narrowing, and a new question arises: Can Stanbic maintain its dominance in the face of sharper, faster rivals? And more critically, can its new CEO, Mumba Kalifungwa, reignite the growth momentum that once made Stanbic not just a giant, but a trailblazer?

More Than a Decade of Profit Leadership Amidst a Fast-Changing Battlefield

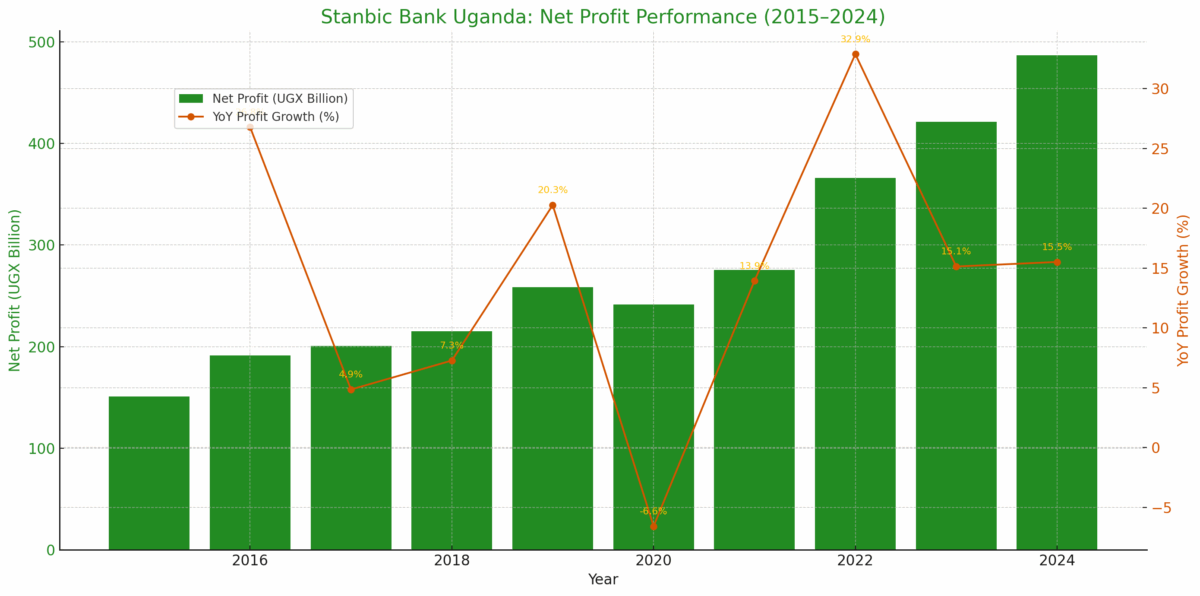

For more than a decade, Stanbic Bank Uganda has remained the country’s most profitable commercial bank, consistently commanding the largest share of total industry profits. From UGX 150.8 billion in 2015 to a record UGX 486.8 billion in 2024, Stanbic more than tripled its net profit over the ten-year span, reinforcing its leadership in size and earnings power.

Between 2015 and 2019, the bank grew its profits from UGX 150.8 billion to UGX 258.7 billion, achieving a compound annual growth rate (CAGR) of 14.4%. During this period, Stanbic captured 28.4% of total industry profits by 2019, outpacing its peers and cementing its position as the market leader. This strong performance was supported by double-digit growth in deposits and assets, robust lending activity, and healthy cost management. Stanbic operated from a position of dominance—leading in nearly every performance metric.

However, between 2020 and 2024, the dynamics shifted. While Stanbic’s profits continued to grow—reaching UGX 486.8 billion in 2024, up from UGX 241.7 billion in 2020—the CAGR of 19.1% during this period, though strong, was no longer the highest in the industry.

Stanbic’s nearest rival, Centenary Bank, posted stronger profit growth over the same period. From UGX 161.2 billion in 2020, Centenary’s profit rose to UGX 342.3 billion in 2024, reflecting a CAGR of 20.7%—higher than Stanbic’s 19.1%. Over the full decade (2015–2024), Centenary’s profit grew more than threefold, from UGX 101.6 billion to UGX342.3 billion, narrowing the absolute gap with Stanbic while increasing its share of industry profits to 20.9%.

Even more dramatic was the turnaround at Absa Bank Uganda. Under the leadership of Mumba Kalifungwa until early 2025, Absa grew its net profit from UGX 40.7 billion in 2020 to UGX 177.9 billion in 2024, a staggering CAGR of 44.6%. Although still behind Stanbic and Centenary in size, the rapidity of Absa’s expansion is a signal of mounting competitive pressure.

dfcu Bank, despite past setbacks, staged a sharp rebound. From UGX 24.1 billion in 2020, dfcu’s profit surged to UGX 75.1 billion in 2024, a CAGR of 32.9%, reclaiming lost ground and boosting its market share to 4.6%.

Mid-tier banks also recorded explosive profit growth:

- Housing Finance Bank increased its profit from UGX 20.7 billion to UGX 71.1 billion, growing at 36.1% CAGR while PostBank Uganda grew from UGX 10.1 billion to UGX 35.4 billion, posting 36.8% CAGR.

- NCBA Uganda, which had a turbulent start to the decade, recovered from negative earnings in 2020 to register UGX 38.9 billion in 2024, delivering a CAGR of 44.1% over the five years.

Some smaller banks, such as I&M Bank, Finance Trust Bank, and Bank of India, also posted aggressive double- or triple-digit CAGR figures, albeit from low base levels.

| Year | Customer Deposits (UGX bn) | YoY Growth (%) | Loans & Advances (UGX bn) | YoY Growth (%) | Total Assets (UGX bn) | YoY Growth (%) | Net Profit (UGX bn) | YoY Growth (%) |

| 2015 | 2,438.4 | – | 1,917.2 | – | 3,729.1 | – | 150.8 | – |

| 2016 | 3,058.5 | 25.43% | 1,976.7 | 3.10% | 4,588.6 | 23.05% | 191.2 | 26.79% |

| 2017 | 3,620.9 | 18.39% | 2,134.0 | 7.96% | 5,404.2 | 17.77% | 200.5 | 4.86% |

| 2018 | 3,892.3 | 7.50% | 2,508.8 | 17.56% | 5,393.1 | -0.21% | 215.1 | 7.28% |

| 2019 | 4,722.2 | 21.32% | 2,852.6 | 13.70% | 6,650.8 | 23.32% | 258.7 | 20.27% |

| 2020 | 5,493.5 | 16.33% | 3,618.4 | 26.85% | 8,572.2 | 28.89% | 241.7 | -6.57% |

| 2021 | 5,741.0 | 4.51% | 3,722.1 | 2.87% | 8,713.7 | 1.65% | 275.4 | 13.94% |

| 2022 | 6,131.3 | 6.80% | 4,085.0 | 9.75% | 9,033.3 | 3.67% | 366.0 | 32.90% |

| 2023 | 6,332.9 | 3.29% | 4,225.1 | 3.43% | 9,258.8 | 2.50% | 421.4 | 15.14% |

| 2024 | 7,106.9 | 12.22% | 4,373.8 | 3.52% | 10,343.9 | 11.72% | 486.8 | 15.52% |

These numbers reflect a banking industry that is expanding rapidly, particularly outside of the traditional top-tier institutions. From 2020 to 2024, total net profits across all 23 banks rose from UGX 727 billion to UGX 1,635.3 billion, representing a CAGR of 22.5%—outpacing Stanbic’s own growth rate of 19.1%.

This industry-wide acceleration, largely driven by digital transformation, product innovation, and customer segmentation, means that Stanbic’s relative dominance is being diluted—even though its absolute profit continues to rise.

The trend also mirrors earlier findings on Stanbic’s slower growth in deposits (6.6% CAGR), lending (4.9% CAGR), and assets (4.8% CAGR) between 2020 and 2024. Without strong acceleration in these core banking drivers, Stanbic’s profitability growth, however robust, is no longer unique.

Stanbic Bank’s Customer Deposits Growth: Under Pressure From Below and Beside

From 2015 to 2024, Stanbic Bank Uganda maintained its crown as Uganda’s largest commercial bank by customer deposits. But while the numbers reflect growth, the momentum tells a more complex story—one of tightening margins, growing competition, and a shifting battlefield. Beneath the surface, the bank’s dominance is being tested by an increasingly aggressive field of competitors, both from traditional top-tier rivals and agile mid-tier challengers backed by regional muscle and digital capability.

Between 2015 and 2019, Stanbic’s deposits surged from UGX 2,438.4 billion to UGX 4,722.2 billion, a sharp rise of UGX 2,283.8 billion. This represented a compound annual growth rate (CAGR) of 18.0%—well above the industry average of 14.5% during the same period. At the close of 2019, Stanbic commanded a 20.6% share of all commercial bank deposits in Uganda, almost double its next closest rival, Centenary Bank, which held 11.0%.

However, in the subsequent five years (2020–2024), that dominance has started to come under increasing strain. Stanbic’s deposits grew from UGX 5,493.5 billion in 2020 to UGX 7,106.9 billion in 2024, an increase of UGX 1,613.4 billion. While still significant, this translated to a much lower CAGR of 6.6%—below the industry average of 7.3%. The bank’s market share edged down slightly to 20.2% in 2024, signalling that while Stanbic continues to grow, its growth is being eclipsed by faster-moving rivals.

What these figures reveal is a narrowing gap. Stanbic’s lead is no longer expanding, and the “moat” it once enjoyed in deposit leadership is slowly being breached by both traditional peers and a cohort of digitally savvy, regionally connected institutions.

As if this is not enough, there is rising pressure from top-tier competitors, such as Centenary Bank, which has quietly but steadily grown its deposit base. From UGX 3136.7 billion in 2020 to UGX 4214.5 billion in 2024, it added UGX 1,077.8 billion over five years—a CAGR of 7.7%, outpacing Stanbic’s 6.6%. Known for its deep rural outreach and connection to faith-based networks, Centenary remains a strong player in the mass market, and its deposit mobilisation strategy is clearly working.

Absa Bank Uganda is another rival, whose story is one of a tech-led resurgence. Its deposits rose from UGX 2,357.7 billion in 2020 to UGX 4,214.5 billion, gaining UGX 827.4 billion at a CAGR of 7.8%. While its market share remained relatively stable (8.5% to 9.0%), Absa’s ability to grow deposits steadily points to sustained relevance. The transition from Barclays to Absa was once a vulnerability, but today, Absa appears to have turned the corner.

Equity Bank was arguably the most formidable challenger during this period. Its deposits ballooned from UGX 1,623 billion in 2020 to UGX 3185.1 billion in 2024, a CAGR of 14.6%. Its five-year CAGR of 14.6% remains more than double that of Stanbic. The bank’s aggressive regional expansion, coupled with its digital-first strategy and integration of diaspora remittances, continues to attract significant liquidity.

The strongest signals of competitive disruption, however, are coming from the mid-tier. Banks like KCB, DTB, NCBA, Housing Finance Bank, and PostBank Uganda are pushing aggressively on deposits. These banks, many of them with regional or government support, are riding on the strength of their parentage, improved digital capability, and a hunger to capture market share.

KCB almost tripled its deposits from UGX 445.6 billion in 2020 to UGX 1,246.5 billion in 2024—an astounding CAGR of 29.3%. It added UGX 800.9 billion in deposits, pushing its market share from 2.4% to 3.5%. This performance is a testament to the strength of KCB’s cross-border operations, its SME banking proposition, and aggressive rollout of agency and mobile banking platforms.

DTB grew deposits from UGX 1,283.1 billion to UGX 2,094.0 billion between 2020 and 2024—a gain of UGX 810.9 billion, with a CAGR of 13.0%. DTB has leaned heavily on its business banking roots and regional linkages, maintaining a disciplined yet expansive growth strategy.

NCBA’s deposits expanded from UGX 396.8 billion to UGX 654.2 billion over the same period, a gain of UGX 257.4 billion and a CAGR of 13.3%. The bank has ridden the wave of fintech collaboration and mobile-based products, echoing the success of M-Shwari in Kenya, and is using tech to leapfrog traditional bottlenecks.

Government-backed Housing Finance Bank grew deposits from UGX 654.2 billion to UGX 1,607.3 billion in five years—a CAGR of 25.2% and an absolute increase of UGX 953.1 billion. This nearly threefold growth highlights its rebounding brand and a shift toward digitisation and mortgage-linked banking.

PostBank added more than UGX 541 billion in deposits between 2020 and 2024, moving from UGX 449 billion to UGX 990.3 billion. With an estimated CAGR above 21.9%, PostBank’s mass-market model and digital agency banking rollouts have powered its ascension. It benefits from a reliable client base of public servants and the unbanked population, making it a strategic government asset. The bank has also seen increased support and business from the government.

The implication of these shifts is clear. Stanbic Bank is no longer pulling ahead—it is slowly being encircled. With a CAGR of 6.6% between 2020 and 2024 compared to 18.0% between 2015 and 2019, its momentum has markedly slowed. Meanwhile, nearly all its rivals—both in the top-tier and mid-tier brackets—have posted stronger deposit growth rates.

In banking, deposits are not just a metric—they are a lifeline. Rich deposits provide the liquidity that enables lending to government, businesses, and individuals. A healthy deposit book is directly linked to a bank’s ability to grow assets, generate income, and attract new customers. Moreover, as banks lend, they deepen customer relationships, which in turn attract more deposits—a virtuous cycle. Hence, deposit dominance is strategic. If Stanbic loses ground here, it risks losing ground everywhere.

Stanbic Bank’s Loan Portfolio: Growth Under Pressure from Fast-Charging Rivals

Over the last decade, Stanbic Bank Uganda has remained the country’s largest lender by value, but a deeper look at its performance in loans and advances between 2015 and 2024 reveals a story of two contrasting phases—one of strong growth and market dominance, followed by a period of slowing momentum amid mounting competitive pressure from both top-tier peers and fast-rising mid-tier banks.

Between 2015 and 2019, Stanbic grew its loan book from UGX 1,917.2 billion to UGX 2,852.6 billion, an increase of UGX 935.4 billion. This translated into a healthy compound annual growth rate (CAGR) of 10.4%, underscoring its position as the dominant lender in Uganda’s banking sector. The bank closed 2019 with a 20.3% market share—by far the highest in the industry—outperforming traditional competitors like Standard Chartered and dfcu Bank. This first phase of growth was defined by a strong balance sheet, a broad customer base across corporate and retail segments, and effective credit risk management.

However, between 2020 and 2024, the pace of growth decelerated significantly. During this second phase, Stanbic’s loan portfolio expanded from UGX 3,618.4 billion to UGX 4,373.8 billion—an increase of UGX 755.4 billion. Though still substantial, this represented a CAGR of just 4.9%, less than half the growth rate achieved in the earlier period. Importantly, this growth also fell short of the industry-wide average of approximately 7.5% for the same five-year period. While Stanbic managed to maintain a stable market share of 20.3% in 2024, this stagnation suggests that the bank is no longer outpacing the rest of the industry. Instead, it is growing at par—or even slightly below the pace of its rivals.

The comparative data is telling. Centenary Bank, Stanbic’s closest challenger, increased its loan book from UGX 1,958.9 billion in 2020 to UGX 3,716.6 billion in 2024—an absolute increase of nearly UGX 2 trillion and a CAGR of 17.4%. Its 2024 loan book is now just UGX 657 billion shy of Stanbic’s, compared to a gap of over UGX 1.1 trillion five years earlier. In other words, Centenary is not only growing faster—it is steadily closing the gap.

Absa Bank Uganda also posted consistent growth. From UGX 1306 billion in 2020, Absa’s loan book grew to UGX 1,993.8 billion in 2024, representing a CAGR of 11.1%. While still less than half of Stanbic’s in absolute terms, Absa has proven resilient and aggressive under its new post-Barclays brand.

Equity Bank, which had been surging in earlier years with an eye-catching CAGR of 43.2% between 2015 and 2019, faltered slightly in the second phase. After peaking at UGX 1,609.5 billion in 2023, its loan book declined to UGX 1,308.8 billion in 2024. This resulted in a significantly lower CAGR of just 0.9% between 2020 and 2024. While this may temporarily take the pressure off Stanbic, Equity remains a formidable institution with a regionally integrated model and strong digital infrastructure that could support a swift rebound.

More striking, however, is the emergence of mid-tier banks that are outpacing Stanbic on a growth rate basis—some growing at up to 7 times Stanbic’s rate. Housing Finance Bank, for instance, posted a CAGR of 18.5% over the 2020–2024 period, growing its loan book to UGX 1,084.7 billion. KCB Bank grew its loan book from UGX 253.2 billion in 2020 to UGX 903.5 billion in 2024, recording a remarkable CAGR of 37.4%. DTB Uganda also posted double-digit growth with an 11.1% CAGR, while government-owned PostBank Uganda expanded its loan book from UGX 334.7 billion to UGX 718.7 billion, achieving a CAGR of 21.1%.

These banks, though smaller in absolute size, are carving out larger spaces in the credit market by leveraging digital platforms, targeting underserved niches such as youth and SMEs, and in many cases, drawing on strong regional or government backing. Their agility, relatively lean cost structures, and alignment with national inclusion strategies are turning them into credible threats to larger incumbents.

From a broader industry perspective, the total loan book across commercial banks grew from approximately UGX 17.7 trillion in 2020 to around UGX 21.6 trillion in 2024. While Stanbic still contributes the largest individual share, its relative contribution to overall market growth has shrunk. Holding a static market share in a growing market is a quiet signal of erosion—others are gaining ground, and the leadership gap is narrowing.

This performance has strategic implications. First, it shows that Stanbic is no longer the fastest-growing lender in Uganda. While scale provides some insulation, the dynamics of banking have shifted. Size alone is no longer sufficient—growth, relevance, and customer-centric innovation are now critical levers of competitiveness.

Ruparelia Group Wins Key Entebbe Land Case, Clearing Path for the New Mega Speke Resort and Convention Centre, Entebbe

Ruparelia Group Wins Key Entebbe Land Case, Clearing Path for the New Mega Speke Resort and Convention Centre, EntebbeSecond, Stanbic is facing increasing pressure from below. The mid-tier banks—particularly those with regional footprints or government ownership—are expanding aggressively, often through mobile-based lending models, agency networks, and partnerships that enable low-cost expansion. These institutions are building deep roots in high-growth segments, such as micro, small, and medium enterprises (MSMEs), youth, agriculture, and digital commerce.

Third, the slowdown in Stanbic’s lending growth could have ripple effects on other areas of the business. Loans and advances are not just an asset—they are a source of customer engagement and a driver of deposits. The relationship between borrowing and saving is well established in retail and SME banking. If Stanbic’s lending slows, it may struggle to attract low-cost, high-quality deposits, thereby affecting its ability to lend competitively and maintain margins in the future.

Stanbic Bank’s Asset Performance: Holding the Top Spot, But for How Long?

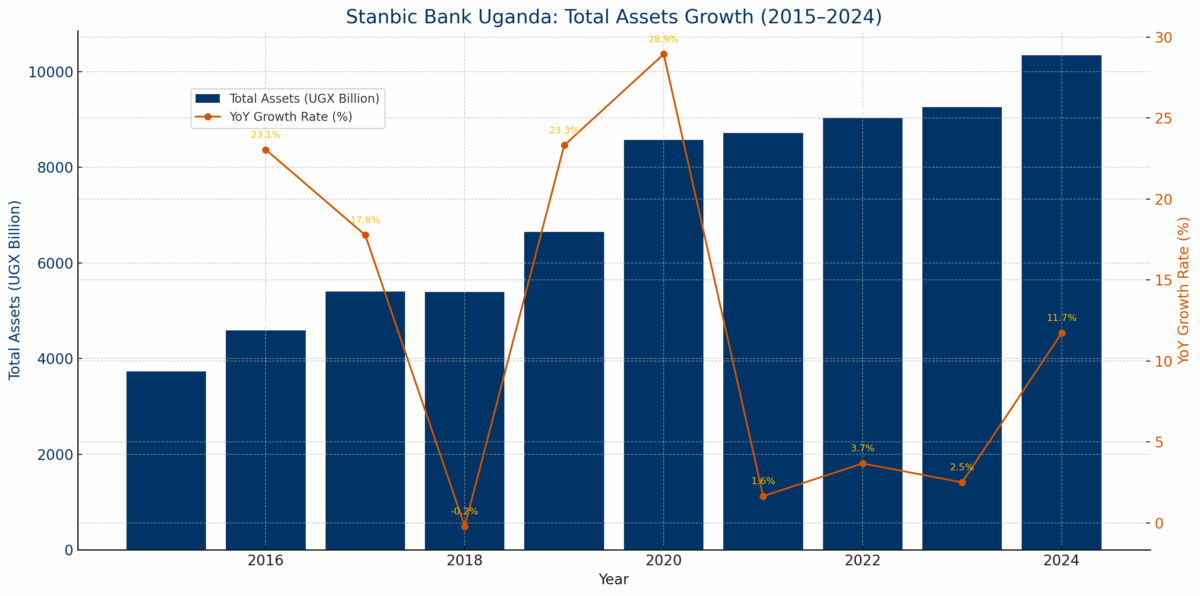

Over the last decade, Stanbic Bank Uganda has consistently held the largest asset base among all commercial banks in the country. However, while the bank has grown in absolute terms, a closer look at asset growth between 2015–2019 and 2020–2024 reveals a more complex dynamic—one that raises critical questions about whether Stanbic is pulling ahead or being caught up with by a more agile and fast-expanding field of competitors.

Between 2015 and 2019, Stanbic Bank grew its total assets from UGX 3,729.1 billion to UGX 6,650.8 billion, marking an impressive absolute growth of UGX 2,921.7 billion over five years. This translated into a compound annual growth rate (CAGR) of 15.6%, one of the highest among tier-one banks during this period.

The bank’s performance during this phase solidified its leadership, ending 2019 with a 20.5% share of the entire commercial banking industry’s assets. This dominance was underpinned by strong deposit mobilisation, a robust lending book, consistent profitability, and sound capital adequacy. Stanbic’s asset strength gave it significant liquidity headroom and a deep capacity to support corporate, SME, and retail lending, as well as substantial holdings in government securities.

This period reflected Stanbic’s position not just as a large bank—but the bank. It had outpaced most of its traditional peers, such as Standard Chartered (4.1% CAGR), dfcu Bank (16.2%), and Absa Uganda (20.5%). Only a handful of banks, notably Equity Bank (27.2%) and NCBA (27.4%), posted higher growth rates, though from much smaller asset bases.

From 2020 to 2024, Stanbic’s asset base continued to grow, rising from UGX 8,572.2 billion in 2020 to UGX 10,343.9 billion in 2024. While this still represents significant expansion in absolute terms (UGX 1,771.7 billion), the CAGR declined to 4.8%—less than a third of the growth rate recorded during the previous five years.

This slowdown in Stanbic’s asset growth is especially notable when compared with the industry-wide trend, where several banks have posted double-digit annual growth. As of 2024, Stanbic’s share of industry assets stands at 19.4%, slightly down from 20.5% in 2019. This shift, though numerically modest, is symbolic—it marks a plateau in dominance and signals that Stanbic’s growth is no longer ahead of the market.

The competitive landscape has evolved considerably. While Stanbic remains the largest bank by assets, its rivals are growing faster, and some are quickly closing the gap.

Centenary Bank’s assets, for example, expanded from UGX 4499.9 billion in 2020 to UGX 7,114.8 billion in 2024, nearly doubling in just five years. This translates to a CAGR of 12.1%, more than 2.5 times Stanbic’s growth rate over the same period. Its market share rose from 11.8% in 2020= to 13.4% in 2024. Centenary’s strategy of rural penetration, financial inclusion, and conservative risk management is clearly paying off, and its asset book is now over UGX 7 trillion, narrowing the gap with Stanbic.

Absa, another very close rival of Stanbic, grew its assets from UGX 3,543.6 billion in 2020 to UGX 5,431.7 billion in 2024, posting a CAGR of 11.3%. The bank added over UGX 2 trillion in assets, with its market share increasing from 9.3% to 10.2%, maintaining a steady position among Uganda’s top five banks. Absa’s digital growth strategy, corporate banking strength, and effective governance during its transition from Barclays continue to reinforce its long-term competitiveness.

Equity grew explosively from a low base in 2015 but experienced a pullback in 2024. Between 2020 and 2024, its asset CAGR was 13.1%, even after a UGX 358.9 billion contraction in 2024. It remains a fast-charging regional player with strong SME and mobile-driven strategies. Its asset base of UGX 3,389.2 billion in 2024 still trails Stanbic’s by a wide margin, but its annual growth momentum (prior to 2024) was one of the highest among the top banks.

Some of the most dramatic shifts have occurred among mid-sized banks, many of which are backed by regional financial groups or the government of Uganda.

The government of Uganda part-owned Housing Finance Bank grew its assets from UGX 1,108 billion in 2020 to UGX 2,339.5 billion in 2024, posting a 20.5% CAGR, one of the highest in the industry. Its absolute growth of more than UGX 1.2 trillion positions it firmly as a rising force. With increased government support, improved mortgage offerings, and digital platforms, HFB has become a critical player in asset growth.

Fully government-owned, PostBank’s asset growth has been phenomenal, from UGX 674.6 billion in 2020 to UGX 1,427.6 billion in 2024, an expansion rate of over 20.6% CAGR. This rapid growth is driven by government-aligned initiatives, digital transformation, and payroll-backed lending. I

KCB expanded its asset base from UGX 657.3 billion in 2020 to UGX 1,718.5 billion in 2024, achieving an exceptional 27.2% compound annual growth rate (CAGR). Its fast-growing footprint, SME-focused lending, and group-level capital support have transformed it into one of Uganda’s fastest-growing banks.

While Stanbic Bank remains the undisputed asset heavyweight in Uganda, it is no longer growing at a faster rate than its competitors. Between 2015 and 2019, it comfortably outpaced the market average. Between 2020 and 2024, it underperformed the industry average—and most of its major competitors.

The competitive landscape has changed. A new breed of lean, fast-growing banks—many regionally backed or state-supported—are climbing up the ranks. Centenary is now over UGX 7 trillion in assets. Absa continues to grow above the market. HFB and PostBank are expanding at double-digit rates. Stanbic is still ahead—but it is no longer pulling away. In fact, the gap is closing steadily.

For Stanbic, the strategic question in 2025 and beyond is no longer just about size—it’s about velocity. Can the bank reclaim its growth advantage and reassert leadership through innovation, digital engagement, and strategic asset allocation? Or will it become a legacy giant overtaken by a more adaptive, fast-charging field?

Only time—and decisive action—will tell.

Stanbic Bank’s Income Growth Reflects a Broader Slowdown Across Core Fundamentals

Between 2020 and 2024, Stanbic Bank Uganda remained the largest income earner in Uganda’s banking sector, growing its total income from UGX 876.6 billion to UGX 1,372.3 billion, reflecting a compound annual growth rate (CAGR) of 11.9%. While commendable and above the industry growth rate (+11.6%), this rate trails that of several peer and mid-tier banks, signalling a loss of growth momentum in an increasingly competitive banking environment.

Stanbic’s market share in total industry income slipped marginally from 18.8% in 2023 to 18.5% in 2024, a reflection not of weakness in performance but of faster gains by rivals who are leveraging niche market penetration, digital transformation, and customer-centric innovations.

Crucially, this income deceleration mirrors Stanbic’s broader slowdown in deposits (6.6% compound annual growth rate, or CAGR), loans (4.9% CAGR), and assets (4.8% CAGR) over the same period. Since these fundamentals largely drive interest income, Stanbic’s muted growth in these areas has naturally capped its revenue expansion.

Several banks posted significantly higher income growth than Stanbic during the same five-year period:

- Centenary Bank increased its income from UGX 720.5 billion in 2020 to UGX 1,217.0 billion in 2024, achieving a compound annual growth rate (CAGR) of 14.0%. Its grassroots reach, especially among rural and faith-based communities, continues to drive both deposits and interest income.

- Absa Bank Uganda, under the leadership of Mumba Kalifungwa until early 2025, expanded its income from UGX 400.1 billion to UGX 690.0 billion, achieving a compound annual growth rate (CAGR) of 14.6%. The bank’s aggressive push into SME lending, digital onboarding, and relationship management for corporates has supported this acceleration.

- Equity Bank posted the highest income CAGR among top-tier peers at 18.0%, growing from UGX 292.1 billion to UGX 565.8 billion—despite a slight dip in 2024. Its pan-African digital strategy and diversified income streams helped drive consistent performance.

- Among mid-tier players, KCB Bank Uganda stood out with an exceptional compound annual growth rate (CAGR) of 32.3%, increasing its income from UGX 78.7 billion to UGX 241.2 billion. It has tapped aggressively into the SME, digital, and payroll-backed loan markets.

- Housing Finance Bank delivered a compound annual growth rate (CAGR) of 27.7%, more than doubling its income to UGX 402.8 billion. Its government-aligned mortgage and affordable housing programs are proving commercially successful.

- PostBank Uganda’s growth increased from UGX 119.5 billion to UGX 248.1 billion, posting a strong 20.0% compound annual growth rate (CAGR), supported by its financial inclusion strategy and the digitisation of government-related payments.

Each of these banks benefited from focused strategic execution—whether in rural financial inclusion, SME financing, government partnerships, or digital transformation. In contrast, Stanbic’s broader product and market reach may now require sharper segmentation and operational agility to reclaim growth leadership.

Scale Without Speed Is No Longer Enough. Although Stanbic Bank remains Uganda’s largest income earner, in terms of growth, it is increasingly outpaced. Slower growth in deposits, lending, and assets has translated into tempered income expansion, allowing rivals to gain ground.

The Kalifungwa Mandate: A Proven Turnaround Leader Faces His Toughest Test Yet

As of March 2025, Mumba Kalifungwa took over the reins at Stanbic Bank Uganda, becoming the latest steward of a high-performing but maturing institution. His appointment is significant. At Absa Uganda, Kalifungwa demonstrated transformational leadership during one of the most volatile periods in recent banking history.

When he assumed office as Managing Director in April 2020, Absa was facing a pandemic-stricken economy. Over the next five years, he oversaw impressive growth across all key performance indicators. Deposits increased by 35% to UGX 3.19 trillion from the UGX 2,181 trillion he inherited, while loans and advances jumped by 52.5% to UGX 1.99 trillion (from UGX 1.33 trillion). Total assets grew by nearly 53% to UGX 5.43 trillion. Income rose by 72.5% to UGX 690 billion, and net profit, which had dipped to UGX 40.7 billion in 2020, rebounded to UGX 177.9 billion by 2024 – a CAGR of 17.9% from the 2019 baseline. Nearly every indicator saw double-digit gains, underscoring Kalifungwa’s strategic agility, operational discipline, and market-driven execution.

Stanbic Bank enters 2025 as a profitable but pressured market leader. Its net profits are the highest in the country, and its balance sheet remains the most formidable. But the market around it is evolving faster than ever. Peers are outpacing Stanbic in growth, younger banks are innovating rapidly, and mid-tier challengers are climbing up the ladder with government support and lean digital models.

Mumba Kalifungwa’s record at Absa demonstrates his ability to steer a bank through uncertainty and position it for accelerated growth. But Stanbic presents a different kind of challenge: not a bank in recovery, but a giant at risk of being outgrown. The urgency now is not about survival, but reclaiming speed, agility, and innovation.

He must revive growth in core fundamentals, restore competitive edge in customer acquisition and product innovation, and lead Stanbic into a new chapter of aggressive but sustainable transformation. The bar is high, but so is the expectation. The market is no longer forgiving of complacent incumbents. And as competitors close in, Kalifungwa must ensure that Stanbic is not just the biggest—but once again the fastest and the best.