Kenneth Mumba Kalifungwa’s first year as Chief Executive of Stanbic Bank Uganda delivered a strong profit performance.

However, beneath the headline numbers lies a more nuanced story of growth, rising costs, and emerging pressure points that will shape the bank’s future trajectory.

For the year ended December 2025, Stanbic posted profit after tax of UGX 586.2 billion at the bank level and approximately UGX 591 billion at the group level, up from UGX 486.8 billion the previous year.

The result reflects a bank that successfully expanded its income base while maintaining operational discipline in a complex economic environment.

Kalifungwa described the year as one of resilience and execution, noting that the bank responded to a dynamic operating environment with discipline and agility, delivering strong performance anchored on a diversified strategy.

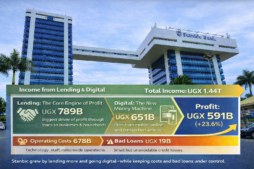

Stanbic’s total income rose to UGX 1.54 trillion from UGX 1.37 trillion in 2024, supported by growth in lending and non-funded income streams.

Interest income on loans and advances climbed to UGX 688.5 billion, while income from government securities and other investments also contributed significantly.

Net interest income reached UGX 788.3 billion, reinforcing the bank’s core strength in credit intermediation.

Non-interest income also played a key role. Fees and commissions generated UGX 236.0 billion, while total non-interest revenue reached UGX 651.2 billion, highlighting Stanbic’s shift toward diversified revenue streams beyond traditional lending.

Stanbic Holdings CEO Francis Karuhanga noted that revenue growth was underpinned by strong fundamentals, with double-digit expansion driven by business growth and client engagement across segments.

However, growth came with rising costs. Total expenditure increased to UGX 807.2 billion from UGX 719.1 billion, while operating expenses rose to UGX 612.0 billion due to inflationary pressures and continued investment in systems, people, and expansion.

Despite this, the cost-to-income ratio remained contained at 47.1%, reflecting disciplined cost management.

Still, the increase in costs outpaced some areas of revenue growth, indicating that efficiency will remain a key challenge.

Credit risk also edged upward. Provisions for bad and doubtful debts rose to UGX 18.6 billion, while non-performing loans increased to UGX 89.4 billion from UGX 70.1 billion the previous year.

Although still manageable, this trend signals growing stress in parts of the loan book.

Despite these pressures, Stanbic delivered profit before tax of UGX 736.0 billion, up from UGX 653.3 billion, demonstrating its ability to absorb higher costs and credit provisions.

Karuhanga added that profitability remained resilient, with return on equity improving to 26.8%, reflecting consistent value creation for shareholders.

Where Stanbic Made and Lost Money in 2025

Where Stanbic Made and Lost Money in 2025On the balance sheet, total assets grew to UGX 11.52 trillion from UGX 10.39 trillion. Customer deposits rose significantly to UGX 8.03 trillion, while loans and advances increased to UGX 5.09 trillion, indicating continued credit extension into the economy.

Deposit growth—up by nearly UGX 920 billion—was one of the bank’s standout achievements. Kalifungwa attributed this to strong client trust, while Karuhanga noted deposits grew by 12.9%, reinforcing confidence in the institution.

Liquidity remained strong, supported by cash balances of UGX 1.47 trillion and financial investments of UGX 1.54 trillion.

Capital levels were also robust, with total qualifying capital at UGX 1.97 trillion and capital adequacy comfortably above regulatory requirements.

However, some risks remain. Large loan exposures stood at UGX 1.64 trillion, pointing to concentration risks in the event of sector-specific shocks.

The rise in non-performing loans also suggests asset quality pressures could increase alongside rapid credit growth.

Cash flow reflected both operational strength and significant shareholder payouts. Stanbic generated UGX 287.6 billion from operating activities but paid UGX 300 billion in dividends, resulting in a slight net decrease in cash.

Total dividends declared reached UGX 360 billion, up from UGX 300 billion in 2024. This included a final dividend of UGX 4.30 per share and an interim dividend of UGX 2.73 per share.

Karuhanga said the payout balances shareholder returns with maintaining capital strength to support future growth.

Shareholders’ equity grew to UGX 2.36 trillion from UGX 2.05 trillion, supported by retained earnings exceeding UGX 2.07 trillion, providing a solid base for continued expansion.

Beyond the financials, Kalifungwa emphasized Stanbic’s role in Uganda’s development, stating that the bank’s “Positive Impact Agenda” focuses on women, youth, and farmers by deploying capital and supporting enterprise.

Karuhanga reinforced this, noting the Group’s resilience and commitment to creating long-term value for shareholders, clients, and the broader economy.

The Chairman, Damoni Kitabire, affirmed confidence in the bank’s governance, noting that the financial statements received an unmodified audit opinion from Ernst & Young.

Kalifungwa’s first year can be described as a strong but not flawless debut. Stanbic Bank Uganda has expanded earnings, strengthened its balance sheet, and rewarded shareholders. However, rising costs, increasing credit risk, and loan concentration will require careful management.

The foundation has been laid, but sustaining this momentum will depend on how effectively the bank navigates these emerging pressures.