On Monday, April 25th, 2022, Equity Bank Uganda, a subsidiary of Equity Group Holdings Plc, published its financials for 2021.

Well, the publishing of financial performance is a regulatory requirement for all supervised financial institutions- and it must happen before the end of April, of every year, so towards the end of the month, there is often a rush to beat the deadline, so it is sometimes easy to miss some incredible stories.

One such beautiful story is the story of Equity Bank Uganda.

The bank reported that in 2021, customer deposits- perhaps the most important indicator of bank performance, had grown by 40.8% or UGX662.3 billion, from UGX1.623 trillion to UGX2.285 trillion! This made Equity Bank, Uganda’s 5th largest bank by deposits, out of 26 banks, with a market share of 8.1%. This is one position up from the 7th in 2020!

Although in the 5th position in terms of total deposits, Equity bank set a 2021 record. No other bank grew its deposits as Equity did. The closest banks to Equity Bank in terms of deposits growth in 2021 were Stanbic Bank which grew its deposits base by UGX247.5 billion; DTB Bank which grew its deposits by UGX217.5 billion and Citibank by UGX178.2 billion. But at UGX662 billion in fresh 2021 deposits, Equity Bank’s growth was larger than the deposits growth of Stanbic, DTB Uganda and Citibank combined!

Thanks to this strong growth in deposits, Equity was able to increase its lending, by 22.4%, from UGX1.261 trillion to UGX1.544 trillion, becoming Uganda’s 3rd largest lender with a 9% market share, two positions better than 2020 when it was the 5th largest lender.

Like night follows day, growth in lending, enabled Equity Bank to increase its total income by 31% from UGX292.1 billion to UGX382.7 billion to become Uganda’s 6th largest bank by income and a 7.3% market share.

Significant improvements in total income combined with efficient cost management – for example, operational costs only rose by 13% from UGX132.8 billion to UGX150.3 billion, supported the bank to report UGX118.2 billion in profit before tax and UGX86 billion in net profit. This is the highest since Equity Bank entered Uganda’s banking industry in 2008.

The bank’s balance sheet, as a result, grew 36.2% from UGX2.069 trillion in 2020 to UGX2.818 trillion in 2021, making the bank the 6th largest bank by assets, one place up from the 7th position in 2020.

Tracing Equity Bank’s Success Story

Equity Bank’s 2021 story is a great story by all means, but if you just look at the 2021 performance in isolation, you risk missing a sweet success story- which in Samuel Kirubi’s view, is a classic Ubuntu story.

Ubuntu is an African philosophy that emphasizes the power of being human i.e., one is because others are and vice versa. Popular among the Bantu- a collection of several hundred indigenous ethnic groups spread over a vast area of Central Africa to Southeast Africa, and to Southern Africa who speak Bantu languages, Ubuntu is built on the principle that ubuntu (humanity) begets abantu (people/customers), who in turn, translate into ebintu (things/prosperity).

Samuel Kirubi has been Equity Bank’s Managing Director in Uganda since 2015. He is also the man, who has presided over much of the bank’s fast and furious— although he insists more on purposeful, growth.

Equity Bank’s 14-year story in Uganda can best be told in two 7-year halves— the first running from 2008-to-2015, which is more of a foundation stage while the next 7 years (2015-2021) have been years of growth. Really good growth.

For starters, Equity Bank had always existed as a strong banking brand next door in Kenya. It didn’t come to Uganda, until 2008.

Unlike its other Kenyan rival, Kenya Commercial Bank (KCB) which chose to set up a greenfield operation in Uganda in 2007, Equity chose to enter Uganda via an acquisition of the then Uganda Microfinance Limited (UML), splashing some USD25.3 million (then UGX43.5 billion).

UML, founded in 1997, was at the time, Uganda’s largest Tier II financial institution with about USD 34m (UGX56.1 billion at the time) in assets and a gross loan portfolio of USD22.8m (UGX37.6 billion). It also had 83,000 customers spread across 28 branches.

But more importantly, with the acquisition, Equity Bank also secured a commercial banking license, joining the real big boys league, and hit the ground running.

By 2011, the bank’s balance sheet had grown fourfold to UGX262 billion underpinned by a UGX163.4billion loan book and 522,000 customers with UGX167 billion in deposits. 2011 was also significant because that’s when the bank made its first profit of UGX544 million.

By this time, industry-wise, Equity had carved out a 2% market share in deposits and a 13th position. In lending, the bank was the 13th of 25 banks with a 3% market share as well as the 14th position in assets base and a 2% market share.

In 2012 the bank launched merchant banking and also entered a partnership with Western Union to ease global transactions. The following year, the bank also added Visa Card, Master Card, JCB, Union Pay and American Express to its cards proposition. In 2014, it also entered a partnership with MoneyGram as well as launched its famous Eazzy 24/7 Mobile Banking App.

By the end of 2015, and after just 7 years in business, Equity had broken into the top 10 banks league, with a bang!

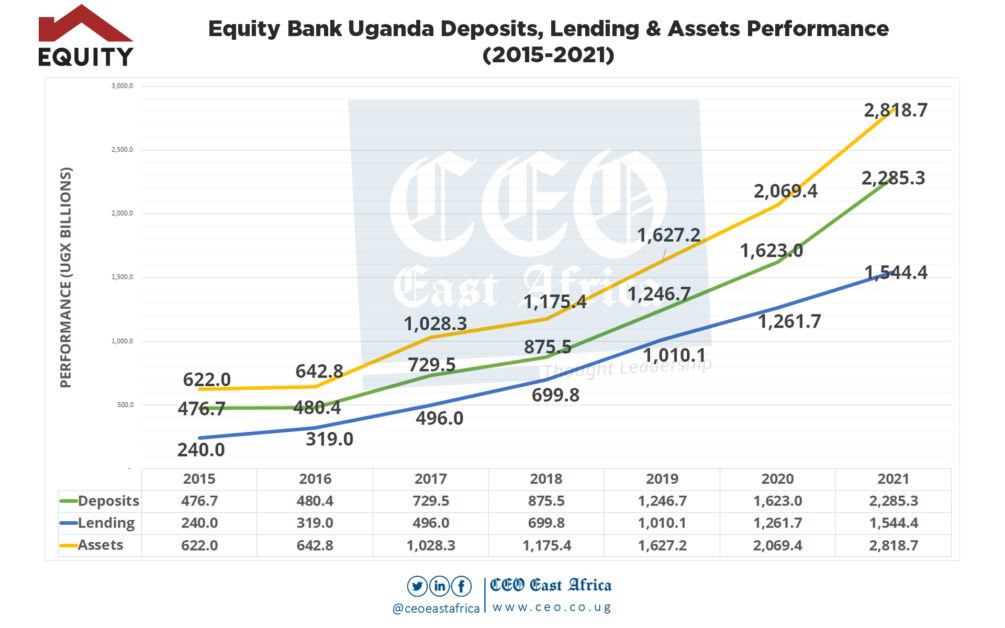

Customer deposits had reached UGX476.7 billion, the 9th largest at the time with a 4% market share. A growing deposits base allowed the bank to grow its loan book to UGX240 billion becoming the 10th largest lender with a 3% market share in a UGX9.5 trillion deposits industry. With a healthy deposits and lending base, the balance sheet bloomed to UGX622 billion, making Equity Bank, the 11th largest of 25 banks, with a 3% market share out of the industry’s UGX19.8 trillion assets at the time.

By this time, the bank’s growth in profitability had stabilized, reaching UGX6.8 billion, earning it the 10th most profitable bank position.

Much of this growth was presided over by Francis C.G Mills-Robertson who was Managing Director from August 2010 to May 2014 and Apollo Njoroge who was Acting Managing Director between May 2014 and mid-2015.

Both gentlemen were experts in the business with good knowledge of the banking landscape in Sub-Saharan Africa. Before Equity, Mills was the Head of Consumer Banking at Standard Chartered Bank in Uganda (April 2003-July 2007) and Executive Director, Consumer Banking, Ghana (July 2007- July 2010). Njoroge, who was the Executive Director and Chief Operations Officer during Mill’s time, was an equally experienced financial executive having served in various roles at Equity Bank in Kenya such as General Manager in charge of Business Relationships and Head of Business Growth & Development.

Great Things Happen When Purpose and Technology Mix with Great People

Mid-2015, Equity Bank, Uganda appointed Samuel Kirubi as Managing Director.

Kirubi was an Equity Bank insider 101.

He joined Equity Bank in Kenya while still at university, through the Equity Leaders Programme (ELP). Established in 1998, ELP is a rigorous leadership development program for top-performing students in the countries where the bank operates, aimed at creating a breed of the next generation of African transformative leaders. The scholars are exposed to Equity’s high-performing environment and are taught values of hard work, work ethics, customer service, communication skills, integrity and professionalism. Since its inception, 6,713 scholars have benefitted from the programme.

Kirubi, was among the pioneering cohort of the programme, in 1998 and got to be mentored by Dr James Mwangi, CBS; the indefatigable and visionary founder of the Equity Group and its current Group Managing Director and Group Chief Executive Officer.

Soon after University, he would join the bank, rising to the Regional Manager level by 2008- the same year Equity was spreading its wings outside Kenya. He was then appointed Deputy Managing Director and Chief Operations Officer at the new Equity Bank, South Sudan- a tough assignment that he took on willingly. This was young Kirubi’s first assignment out of his home country.

In just 4 years, Equity South Sudan had grown to 11 branches. After a job well done, the now battle-hardened Kirubi was sent to Rwanda to establish the Equity subsidiary there. He would leave Rwanda in mid-2015 after another fine job there and was appointed Managing Director of Equity Bank Uganda.

Related

Kenya Shilling Holds Firm as Remittances Rise and Markets Show Mixed Signals – Central Bank Report

Kenya Shilling Holds Firm as Remittances Rise and Markets Show Mixed Signals – Central Bank ReportOver and above his rich African banking experience, he holds a master’s degree in Business Administration (Finance) from Moi University and a Bachelor of Arts Degree in Economics and Statistics from Egerton University. He is also a graduate of the Advanced Management Programme (Strathmore- IESE Business School, Barcelona Spain).

Kirubi, was in June 2016, joined by another astute banker, Anthony Kituuka as Executive Director.

Before returning to Uganda, Mr Kituuka was the Executive Director in charge of regional subsidiaries at Equity Bank Group, so he had an idea of what was going on in Uganda. Besides, before joining the Equity Group, he had spent his time in the banking industry, in various roles- Kenya Commercial Bank (KCB) in Nairobi as the head of Global Corporates, KCB Bank Uganda Limited (Head of Corporate Banking) and Barclays Bank Uganda Limited (Head of Business Banking).

An FCCA fellow and an alumnus of the Strathmore, Lagos and IESE (Spain) Business Schools, Kituuka, also holds an MBA in Oil and Gas from Middlesex University, London and a Bachelor’s degree in Statistics and Applied Economics from Makerere University.

Working with this dynamic duo, at the Exco level has been a team of other experienced bankers who together blend a rich complement of financial services experiences in and outside Uganda. They include Jimmy Mwangangi, the Head of Credit; Joseph Kimuli, the Head of Internal Audit and Sarah K. Nakkazi, the Head of Compliance. Others are Kenneth Onyango, the Head of Operations, Kezia D. Asiimwe, the Manager, Finance and Juliet Muheirwe, Head of Human Resources.

This team, together with another 1,200 bank staff has been instrumental in building a foundation and executing what has been Equity Bank’s second phase of runaway growth.

This second phase growth story started with the October 2017 launch of the bank’s robust Digital Banking platform—Eazzy Suite. The Eazzy Banking suite of products included a banking app known as EazzyBanking App which allows one to transfer funds to other accounts and mobile wallets or pay utility bills. It also included a solution to assist welfare clubs, investment clubs and groups manage their joint finances and investments known as EazzyClub. It also included a real-time bulk payment solution that allows one to automate electronic fund transfers, RTGS and mobile transfers called EazzyRemittance and a retail internet portal where customers can manage their bank accounts known as EazzyNet.

In addition, the suite has an interoperable payment platform, EazzyPay which allows one to pay for bills as well as goods and services at registered merchant outlets; a mobile-based loan product known as EazzyLoan; a cash and liquidity management solution for SMEs known as EazzyBiz, and banking capabilities packaged as APIs exposed through EazzyAPIs platform.

This would be followed by the rollout of the bank’s agency banking platform, known as EquiDuuka. EquiDuuka enables access to Equity Bank through third parties spread across the country. The bank was one of the first few banks to launch a standalone agency model, before other banks came on board, via the Agent Bank Company an outfit owned by all the commercial banks currently operating in Uganda, through their umbrella body, the Ugandan Bankers Associations.

By the end of 2018 Equity had opened nearly 1000 EquiDuukas. This was supported by 33 branches, 37 ATMs and 945 POS merchant terminals. Customers grew to 500,000+, deposits to UGX875 billion and lending to UGX699.8 billion. Assets crossed the UGX1 trillion mark, to reach UGX1.175 trillion, making Equity the 8th largest bank in the country, out of 25 banks.

Performance With a Purpose—The Unstoppable Equity Bank

The 2021 performance is therefore not surprising as it continues a 7-year trend in which the Bank continues to impress, year after year.

In the 7 years to 2021, deposits have grown 4 times or 379.4% from UGX476.7 billion in 2015 to UGX2.285 trillion in 2021; a compounded annual growth rate (CAGR) of 25.1%. The bank has also moved from the 9th position in terms of deposits to the 5th!

No bank has enjoyed this much compounded annual growth in deposits in this period, not even Stanbic Bank, Uganda’s largest bank- which during this period, grew its deposits by a CAGR of 13%.

In the same period, lending has grown 6.4 times or 543.5% from UGX240 billion to UGX1.544 trillion at the end of 2021; a CAGR of 30.5%. Again, this is the industry’s fastest and most stable growth, enabling the bank to climb from the 10th largest lender to now the 3rd largest.

Since interest income forms a big chunk of income, this has enabled the bank to also become one of the most profitable banks— the 6th most profitable following, a healthy 12.6 times growth or 751.5% growth in net profit over the period, from UGX6.8 billion in 2015 to UGX86 billion- a CAGR of 43.7%!

All this is on the back of customer numbers that have tripled, from 500,000+ to almost 1,500,000.

But more importantly, Equity Bank has during this period built an inexorable growth machine, made up of almost 6,000 agents running approximately 3.5 million transactions, worth UGX7 trillion per quarter. That translates into 1.2 million transactions a month, worth some UGX2.3 trillion! This means the bank’s agency network is pulling in an average of 40,000 transactions, a day worth UGX76.6 billion!

The agency network is supported by another equally significant payments network of close to 20,000 merchants.

As a result, today, only 3% of Equity Bank’s transactions are happening in the bank, while 97% are happening outside the bank.

To back this up, the bank, early this year launched another game-changing digital product service that enables a customer to open an account in minutes, from anywhere across the country, at any time and using just about any mobile phone.

All a customer needs to do is dial *247#. This triggers off a chain of ‘digital events” that sees the Equity Bank systems ‘speaking’ to the National ID database at the National Registration and Identification Authority (NIRA) to match the SIM card user details and subsequently an account number is automatically assigned.

No queues, no documents. Just *247# on any mobile phone!

Equity Bank is banking on this one-of-a-kind system to catalyse its financial inclusion and recruitment agenda, and this is how. While on one end, these digital systems make it easy for Equity Bank to enroll customers as well as serve them more efficiently, and yes profitably too, this is just one spoke in Equity Bank’s overall philosophy.

At the heart of the bank’s corporate philosophy is the transformation of the lives and livelihoods of Africans, socially and economically by availing them modern, inclusive financial services. This is informed by the bank’s purpose— “transforming lives, giving dignity and expanding opportunities for wealth creation in line with the bank’s vision of being the champion of the socio-economic prosperity of the people of Africa.”

To pursue its purpose, the bank pursues inclusive, customer-focused financial services that socially and economically empower clients and other stakeholders across 6 key pillars. These are education and leadership development; energy and the environment; enterprise development and financial inclusion; food and agriculture as well as health and social protection.

This is because, Equity believes that to drive Africa’s growth, African populations must be adequately, efficiently, and affordably banked, which is why investment in financial technologies is such a big deal. Apart from enabling Equity to rapidly expand its services to the underserved, technology makes financial inclusion affordable and therefore attractive. Affordable access allows the bank to pass on the benefits to the market, in form of affordable credit and other services.

Rapid financial inclusion has another critical role in the bank’s strategy. It allows Equity Bank to efficiently generate customer deposits/savings- the blood of every banking system, that it can in turn lend to those who need it most, especially those in the above 6 key pillars of growth. Investing in digital channels also enables money to move fast, to those who need it thus accelerating impact and value. And this is not just for Uganda- but across the entire Equity Group.

This is Equity Bank’s holy grail, on which it is banking its next phase of growth, which growth, according to Kirubi, will be driven by unlocking Uganda’s and Africa’s latent potential and in so doing grow the cake for mutual prosperity.

“We love to benchmark our next growth with the market potential and not our existing market share,” Kirubi told this reporter in an interview.

“For example, there are about 10 million bank accounts for the entire banking industry, but Uganda is a country of over 40 million people with a bankable population of between 15 million to 20 million,” he says, adding: “Therefore, in terms of that potential, in five years, we want to be in the north of 7 million active customers and 10% – 15% market share.”

He however reiterates that market share, is not the end goal, but rather the bigger purpose is creating shared prosperity. “It is pointless to have a big market share when the economy is not growing, which is why it is a bigger purpose for us to grow the cake. That is why we are constantly asking ourselves; how do we partner with the government and other entities to widen financial inclusion? How do we participate in catalyzing growth in the various sectors of the economy? How do we leverage our huge African presence to leverage other growth opportunities in the East African Community and the African continent as a whole?” he concludes.