Last week’s signing between the Government of Uganda and Standard Chartered Bank offered a reminder of the institution’s enduring strength.

The €641.1 million (UGX 2.75 trillion) financing package, covering power transmission, strategic water projects, and critical oil roads, underscored Standard Chartered’s continued ability to mobilise long-tenor, cross-border capital for projects few banks in Uganda can structure or underwrite.

This capability is anchored in the balance sheet and credibility of its global parent.

It is also a reminder that although the bank has chosen strategic shrinkage, by agreeing to sell its retail and wealth business to Absa Uganda, it remains a force to reckon with.

Writing in the CEO East Africa Magazine in October 2025, Sanjay said that the deal (still subject to regulatory approvals) “marked the beginning of an evolution, a deliberate and confident strategic refocus on what we do best: enabling trade, investment, and prosperity through our corporate and investment banking franchise.”

In otherwords, Standard Chartered is not trying to be smaller. It is trying to be sharper.

At the signing ceremony, both Dalu Ajene, Standard Chartered’s CEO and Head of Coverage for Africa, and Sanjay used the moment to underline why the bank continues to occupy a distinctive position in Uganda’s financing landscape.

Ajene pointed to the institution’s ability to leverage its on-the-ground presence and long-standing relationship with the Government of Uganda to structure complex, long-term financing, describing the transaction as an illustration of how international financial institutions can partner with governments to deliver projects with lasting economic and social impact in support of Uganda’s Tenfold (10X) Growth Strategy.

Rughani, in turn, framed the deal in practical development terms, noting that investments in water security, roads, and power transmission are foundational to resilience and inclusive growth, and reaffirming the bank’s commitment to financing infrastructure that is economically viable.

Taken together, the remarks reinforced a central theme of Standard Chartered’s current positioning: that even as it reshapes its domestic footprint, it retains the local insight, regional reach, and global balance-sheet strength required to finance transactions few banks in Uganda can credibly execute.

A balance sheet under pressure and the limits of parent strength

Standard Chartered Bank benefits from the balance sheet, credibility, and risk appetite of a powerful global parent.

That backing underpins its ability to arrange complex, long-term financing and to remain a preferred partner for sovereign and large corporate transactions.

But the local numbers show that execution on the ground has been operating under pressure for some time.

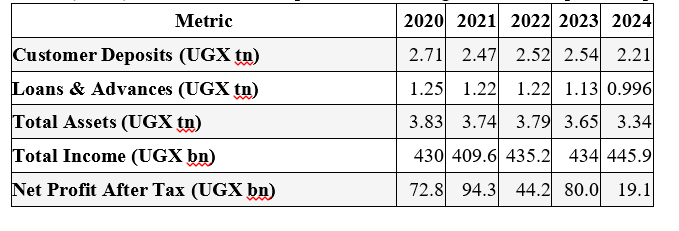

Over the last five years, Standard Chartered Bank’s headline indicators have steadily trended downward, even as Uganda’s banking system expanded.

Between 2020 and 2024, customer deposits declined from UGX 2.71 trillion to UGX 2.21 trillion (–19%), loans and advances from UGX 1.25 trillion to UGX 996 billion (–20%), and total assets from UGX 3.83 trillion to UGX 3.34 trillion (–13%).

These contractions point to a shrinking domestic footprint that predates the formal decision to exit mass-market retail.

Income generation, however, has proved more resilient. Total income edged up from UGX 430 billion in 2020 to UGX 445.9 billion in 2024, suggesting that the bank has been able to defend revenues even as scale reduced.

But profitability tells a more uneven story. Net profit after tax fell sharply to UGX 19.1 billion in 2024, down from UGX 80 billion the year before, underscoring the sensitivity of returns to costs, mix, and operating leverage in a smaller franchise.

Whether this compression reflects market dynamics, internal reprioritisation, or global capital allocation decisions is open to interpretation.

What is clear is that pressure on scale and returns was already evident well before the retail exit was announced, and that parent backing alone does not insulate the local business from the demands of disciplined execution.

Tax Appeals Tribunal Halts URA’s Objection to Non-Payment of 30% of Disputed UGX 169.9b by MTN Over Due Process Failures

Tax Appeals Tribunal Halts URA’s Objection to Non-Payment of 30% of Disputed UGX 169.9b by MTN Over Due Process Failures

Standard Chartered Bank: 5-year performance snapshot (2020–2024) (UGX trillion / billion)

Viewed in that context, the decision to sell Standard Chartered’s retail and wealth business to Absa, first signalled in late 2024 and formalised in 2025, represents less a retreat than a continuation of an existing recalibration.

The bank is deliberately choosing to be smaller, more focused, and more specialised. It will no longer compete aggressively for mass retail deposits, SME lending, or consumer wealth management.

Instead, Standard Chartered is concentrating on areas where it believes its global network and expertise offer a durable advantage: corporate and investment banking, structured and project finance, financial markets and treasury, trade finance, and sustainable finance, precisely the capabilities showcased in last week’s government financing deal.

But this strategic sharpening also raises the execution bar. With retail scale and diversification falling away, performance will increasingly depend on how effectively the local team originates, prices, structures, and manages complex corporate transactions in a crowded and competitive market.

For Rughan, the challenge is no longer to explain the strategy, but to demonstrate that a leaner Standard Chartered Uganda can convert focus into sustainable profits, acceptable returns on equity, and continued relevance, using local execution, not just global backing, as the differentiator.

Why 2026 matters for Rughani

This strategic clarity, however, is also what places Rughani firmly in the hot seat.

First, the Absa transaction must now be executed flawlessly. Tens of thousands of retail customers, billions of shillings in deposits and loan balances, staff, data systems, and regulatory approvals must transition without disruption.

For a bank with a 113-year history in Uganda, any misstep would carry reputational consequences far beyond the immediate transaction.

Second, once retail capital is freed, results will matter more than rhetoric. The promise of a leaner, corporate-focused Standard Chartered must translate into higher returns on a smaller balance sheet, improved profitability, and sustained relevance in Uganda’s largest investment cycles: energy, infrastructure, oil and gas, and regional trade.

Third, the competitive landscape is unforgiving. Corporate and investment banking in Uganda also has formidable players.

Stanbic and Absa, too, are key players in large-scale corporate lending and transaction banking; Citi holds a powerful niche with multinationals and sovereign clients, together with Stanbic and Absa, too; and well-capitalised regional and local banks, Centenary, dfcu, DTB, KCB, and Equity, are increasingly active in structured and project finance. Global pedigree alone does not guarantee dominance.

Strength remains but so does scrutiny

The paradox of Rughani’s moment is that Standard Chartered remains one of the few banks capable of pulling off deals like last week’s government financing, precisely because of the backing, risk appetite, and international reach of its parent group.

That strength buys credibility and time. But it also raises expectations.

In 2026, Uganda will begin to see what remains of Standard Chartered Bank Uganda once the retail and wealth businesses are fully carved out and whether the sharper, corporate-led model can deliver sustainable profits, acceptable returns on equity, and institutional relevance without the cushion of mass-market retail banking.

That outcome will define Rughani’s tenure far more than the strategy itself.

That is why, even as Standard Chartered continues to sign landmark transactions and position itself at the centre of Uganda’s development financing, all eyes are on Rughani.