The proposed tax changes for the 2026/27 financial year go well beyond routine amendments.

Taken together, they point to a deliberate policy shift toward easing the cost of doing business, improving compliance through digital systems, and attracting investment into priority sectors such as tourism, health, agriculture, energy, and manufacturing.

Most of the proposed changes are set to take effect on July 1, 2026.

For businesses, these proposals are not merely legal amendments. They could translate into lower compliance costs, stronger cash flow, reduced tax exposure on qualifying investments, and fresh room for expansion.

Below are the key proposals businesses should watch closely.

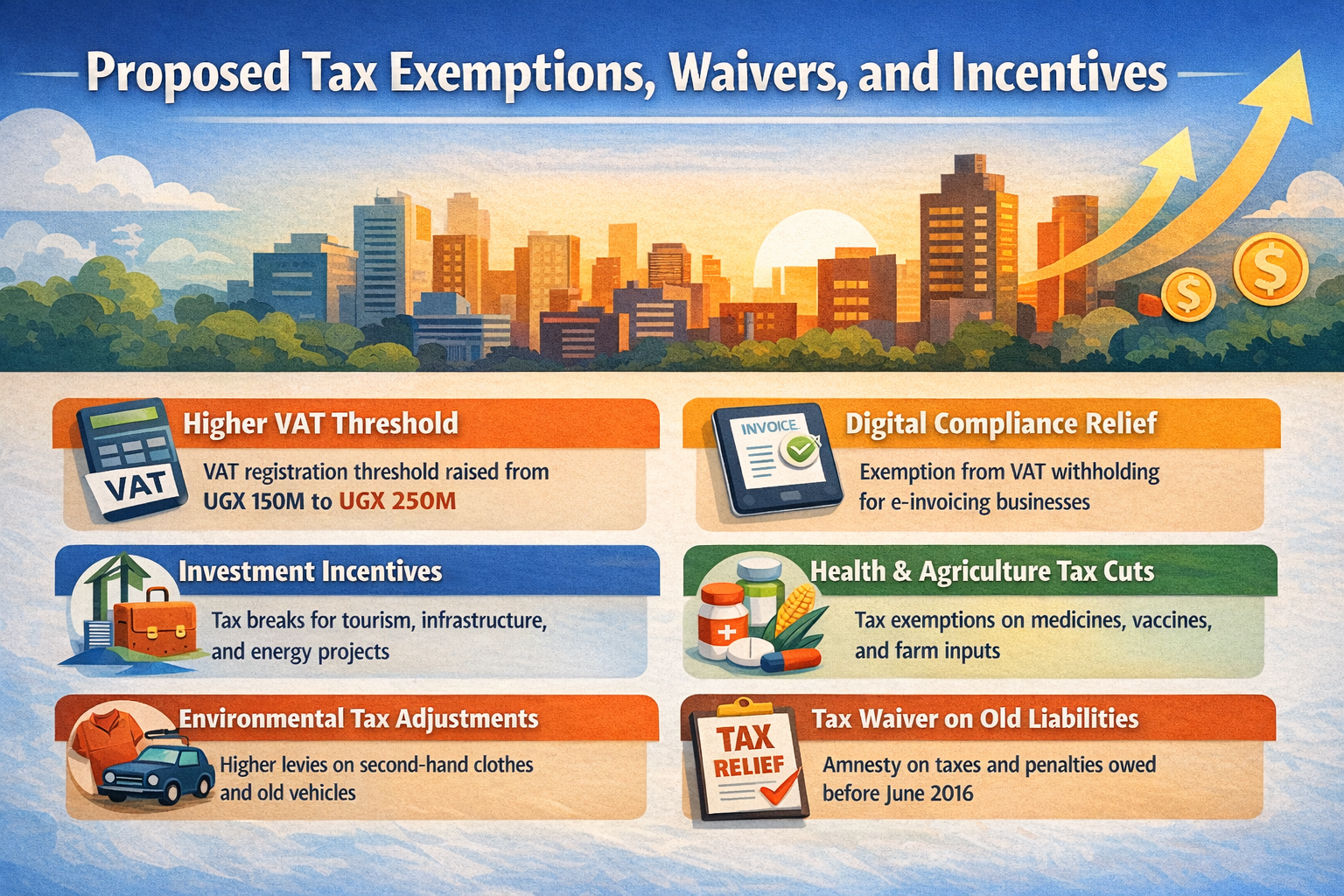

The VAT threshold for small businesses

One of the clearest relief measures is the proposed increase in the annual VAT registration threshold from UGX 150 million to UGX 250 million, representing an increase of UGX 100 million, or about 66.7%.

This change could remove many small and growing businesses from mandatory VAT registration, reducing the cost of filing returns, maintaining VAT records, and managing related audits.

It also gives informal businesses more breathing room as they transition into the formal economy.

VAT withholding exemption for digital-compliant businesses

The VAT Bill also proposes that a designated withholding agent will not apply VAT withholding where payment for taxable supplies is supported by an e-invoice or e-receipt issued in line with the Tax Procedures Code Act.

In practical terms, compliant businesses using e-invoicing could avoid VAT being withheld at source, improving liquidity and rewarding digital compliance.

This effectively turns digital tax adoption into a financial advantage, not just a compliance requirement.

Investment incentives in tourism and infrastructure

Tourism is one of the clearest winners in the proposals. Under the VAT framework, a taxable person who develops a hotel or tourism facility may claim a VAT credit if they invest at least $10 million as a foreign investor or $5 million as a Ugandan citizen.

The credit applies to costs incurred up to two years before commissioning, including civil works, feasibility studies, construction services, and qualifying locally produced materials.

In addition, the Income Tax proposals provide for an income tax exemption for developers meeting the same investment thresholds, provided they use at least 70% locally sourced raw materials and employ at least 70% Ugandan staff, whose wages account for at least 70% of the total wage bill.

Together, these measures significantly improve the investment case for large-scale tourism and infrastructure projects.

Tax exemptions on health and agricultural inputs

The External Trade Bill proposes exempting imports of vaccines, medicines, medical supplies, pesticides, rodenticides, acaricides, and insecticides from both the infrastructure levy and the import declaration fee.

This is expected to lower landed costs for businesses in health supply chains and agricultural input distribution, while improving access to essential products and supporting productivity in the agriculture sector.

Burnt Investment, Broken Claim: A Tourism Lodge Owner’s Legal Battle with CIC Life Insurance

Burnt Investment, Broken Claim: A Tourism Lodge Owner’s Legal Battle with CIC Life InsuranceEnvironmental tax adjustments

The proposals also introduce strong environmental signals. A levy of 30% of the CIF (Cost, Insurance, and Freight) value is proposed on second-hand clothing, which is expected to discourage low-quality imports and potentially support local textile industries.

For motor vehicles, the maximum allowable import age is reduced from 15 years to 13 years, while environmental levies increase progressively from 20% to 50% of CIF value depending on the vehicle’s age between nine and 12 years.

These measures are likely to shift demand toward newer, cleaner alternatives and create opportunities in more sustainable product segments.

Tax waiver on historical liabilities

A major relief measure is the proposed waiver of all taxes, penalties, and interest outstanding as of June 30, 2016.

This provides a clean slate for businesses with legacy tax issues, allowing them to resolve historical exposures and return to full compliance without the burden of accumulated liabilities.

Broader tax base and compliance measures

While offering relief, the proposals also expand the tax base. New withholding tax provisions include 5% on certain foreign interest payments, 6% on non-business asset purchases, 15% on betting winnings, 10% on telecom and mobile money commissions, and 6% on payments to public entertainers.

Additionally, businesses carrying forward losses for more than seven years will be subject to a minimum tax of 0.5% of gross income, while stricter transfer pricing rules reinforce compliance with the arm’s length principle.

This reflects a broader push toward fairness, transparency, and improved revenue collection.

Excise duty adjustments across sectors

Changes in excise duty will also influence business costs. Fuel rates are proposed at UGX 1,750 per litre for petrol and UGX 1,430 per litre for diesel, while construction inputs such as cement are set at UGX 1,000 per 50 kilogramme.

Other adjustments include UGX 300 per kilogramme on sugar, UGX 400 per litre on cooking oil, and UGX 500,000 on motorcycle registration.

There is also a notable differentiation between local and imported products, particularly in plastics and paints, where higher rates on imports could encourage local manufacturing and substitution.

The bigger picture for businesses

Taken together, these proposals combine relief with discipline. Businesses stand to benefit from reduced compliance costs, targeted exemptions, investment incentives, and the clearance of historical tax liabilities.

At the same time, they must prepare for expanded withholding obligations, minimum tax exposure, and stronger compliance enforcement.

The 2026/27 tax proposals are, therefore, not just policy updates. They represent a strategic mix of incentives and reforms that businesses can actively leverage to improve efficiency, manage costs, and position for growth in an evolving economic landscape.