For every organisation/company, there are 2 sources of revenue/income. There is the mainstream revenue/income that comes from that particular company’s main business such as gross turnover for Fast Moving Consumer Goods Companies (FMCG).

The second type of revenue/income is classified as other income. Other income is that income that does not come from a company’s main operations such as gain or loss on revaluation of assets.

Accountants present these sources of income separately.

There has been a lot of mixed reactions and anxiety regarding NSSF’s recently released results, especially around the UGX402.8 billion in unrealised losses, which is why I have been prompted to break this down for many of NSSF’s nearly 2 million members.

First of all, NSSF’s core business is collecting member contributions and investing them safely and prudently and then pay out to members a real return – at least 2 percentage points above the 10 year rate of inflation.

This is a tradition they have kept since 2012/13.

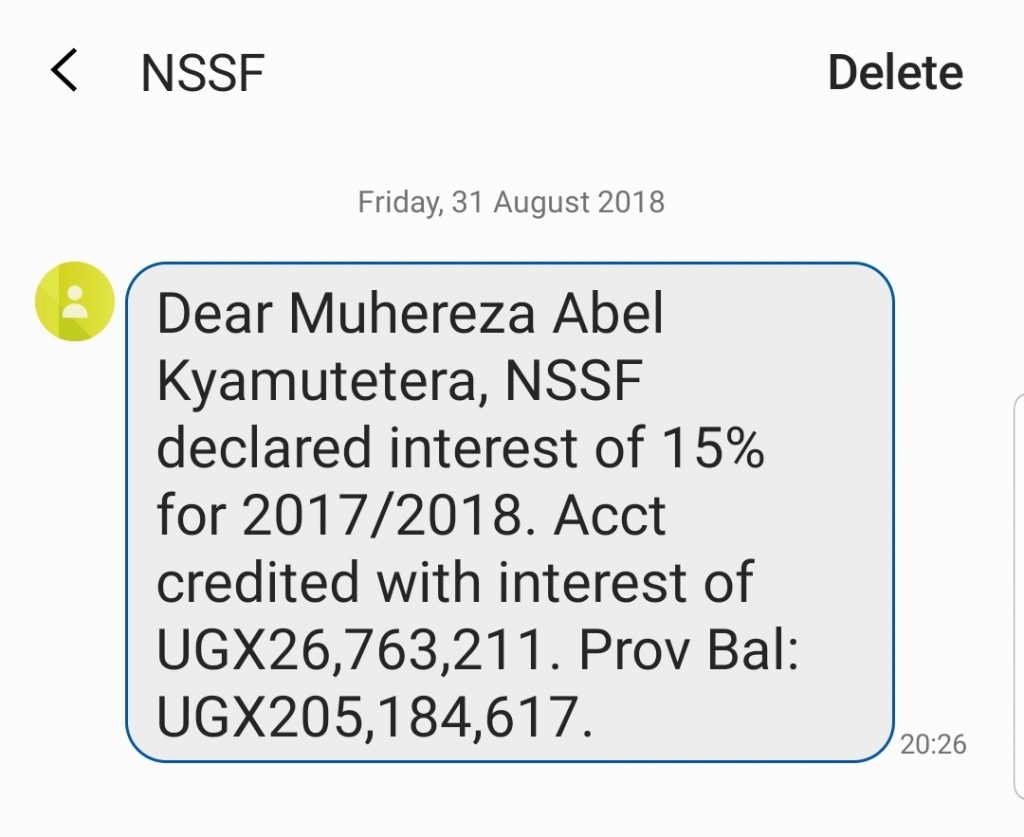

The Fund in 2012/13 declared 10% interest rate, 11.23% in 2013/14 and 11.50% in 2014/15. In 2015/16, the interest rate rose to 13%, then declined slightly to 12.30% in 2016/17 and 11.23% in 2017/18. In 2018/19 the fund paid a historic high of 15% in the Fund’s 34 years of existence.

To sustain this good return to their members, including myself, NSSF invests in and earns their main income from 3 major areas i.e. fixed income, equities/shares and real estate. The Fund as at June, 2019 held 79% of its investment portfolio in fixed income, 15% in equity and 6% in real estate.

Back to their mainstream income, NSSF registered a good year, with interest income (mainly from fixed income investments) growing by 19.3% from UGX978.1 billion in FY2017/18 to UGX1,167.2 billion in FY2018/19. This was despite drops in yields for long-term bonds where NSSF holds over 70% of its fixed income investments.

The Fund also realised a 45.3% growth- from UGX53 billion to UGX77 billion in dividend income as many of the listen companies in which it invests in the region recorded great growth. In fact, this year NSSF’s dividend income grew even more boldly – given that in 2017/18, it only grew by 1.3%, from UGX52 billion the previous year, to UGX53 billion.

Although rental income declined slightly by 1.8%, from UGX10.9 billion to UGX10.7 billion, overall, on the whole, NSSF’s total revenue from its main operations, registered a 20.4% growth, from UGX1,042 billion to UGX1,254.9 billion.

What is an unrealised loss and what caused the UGX402.8 billion unrealised loss?

The UGX402.8 billion in unrealised loss, came about because of two major reasons:

- Fair value loss on equity investments of UGX168.9 billion

- Foreign exchange loss of UGX319.4 billion

But first of all, what is a fair value loss and what is a foreign exchange loss?

Fair value loss/gain emerges from the term fair value which is an accounting term that basically means a potential value of an asset; it could be a product, stock or security. As such, fair value gains /losses refers to the changes in the potential value (what an asset could be sold for) of an asset over the course of the year. It is a fair value gain when the value goes up and a loss when value goes down. A fair value gain or loss is non-cash.

On the other hand, because different currencies have different values, foreign exchange gains/ losses is basically the losses or gains that a company will incur in the process of acquiring or owning assets and liabilities or as it transacts business in other currencies, other than their own or normal currency.

As already mentioned above, NSSF does invest in fixed income assets and stocks/shares in Uganda and in the region and in FY2018/19, the Fund did make good returns- but how come from the same investments where it earned good interest income and dividends, it also got exposed to fair value losses amounting to UGX168.9 billion loss, yet the year before, it registered a UGX212.2 billion fair value gain?

It is important to note that most, if not all of the companies where NSSF owns shares in the region are profitable- some like a Umeme and Safaricom registered significant profit growth, which is why NSSF saw a 45.3% growth in dividend income from UGX53 billion to UGX77 billion, much better than the previous year.

Related

I&M Bank Katogo Golf Series Returns to Entebbe with Innovative Format and High-Stakes Rewards

I&M Bank Katogo Golf Series Returns to Entebbe with Innovative Format and High-Stakes RewardsHowever, during 2018/19, stock exchanges in East Africa, were hit by external factors many of which NSSF has little control over. The markets saw a number of foreign investors exit massively due to uncertainties created by Brexit and the China-trade war and all of a sudden there was a lot of shares available for sale more than available demand, which led to a collapse in trading activity and share prices eventually.

As a result, the Nairobi Stock Exchange all share index lost 14%, the Uganda local share index shaded 10% while that of Tanzania plummeted by over 21%. In fact it was reported by Reuters on August 7, 2019 that that the sudden foreign investor outflows led the Nairobi Stock Exchange’s main index- the NSE-20 to hit a 10-year low. The index closed at 2,545.28 points, down from 2,552.19 a day earlier. The last time the index hit this low was in March 12, 2009, when it closed at 2,453.36.

Consequently, this meant that share prices in stocks held by NSSF averagely closed below the prices registered at end of the previous financial year, which negatively impacted on the value of those shares on NSSF books.

But this is not to mean that the listed companies that NSSF has invested in like Umeme, Stanbic Bank in Uganda and Safaricom and Kenya Commercial Bank in Kenya are doing badly. These are some of the best performing companies in the region- but a sudden withdraw of foreign investors has seen a lull in the share prices of these companies.

This ultimately has meant that fair value (potential value) of NSSF’s investments in these companies has fallen- thus the fair value loss of UGX168.9 billion. But as markets stabilise and particular these companies continue the good performance, prices will bounce back and NSSF’s investment/wealth in these companies shall grow.

What is important to note is that NSSF is a long term investor and they are still holding onto these shares; it would have been a different scenario if the loss had been occasioned by a transfer of the shares at a loss.

Regarding the foreign exchange loss- because NSSF makes most of its money in Uganda, every time it has to invest outside Uganda and or make transactions in foreign currencies, it stands a fifty-fifty risk/opportunity to lose or make money, as it exchanges the Uganda Shilling into the currencies of those particular markets.

ALSO READ: NSSF PROMISES MEMBERS INTEREST ABOVE INFLATION, DESPITE EARNINGS COMING UNDER PRESSURE FROM MARKET VOLATILITIES https://www.ceo.co.ug/nssf-promises-members-interest-above-inflation-despite-earnings-coming-under-pressure-from-market-volatilities/

As a rule of thumb- when the Ugandan shilling is weaker than the Kenyan shilling, it means that the value of NSSF’s investments- be it stocks or currencies held in Kenya Shillings, is higher when converted to Ugandan shillings and this brings about a foreign exchange gain.

Equally, when the Ugandan shilling is stronger than the Kenyan Shilling, like has been the case in FY2018/19, it means the value of NSSF investments held in Kenyan Shillings reduces when converted to Ugandan shillings- especially for reporting purposes since NSSF is domiciled in Uganda.

In the period under review, averagely the Ugandan shilling appreciated 6.1% against the Kenya and Tanzania Shilling, thus putting pressure on the value of NSSF investments in those countries.

Again, let it be understood that NSSF has very little control on the currency markets and there is always a fifty-fifty risk/opportunity especially if the currencies are volatile. For example NSSF made a forex gain of UGX 319.4 billion in FY2017/18 but because of a stronger shilling, this time round it registered a forex loss of UGX247.4 billion.

But let me reemphasize that the so-called UGX402.8 billion is a paper loss, because NSSF has not sold the shares it holds. A paper loss is an unrealized capital loss in an investment- it is basically the difference between the current price and the purchase price. It is a reduction in value, no money has basically been lost. If NSSF had sold, then you could say it has lost money.

NSSF promises interest rate above inflation

Nevertheless, because NSSF registered a 13.1% increase in NSSF’s assets under management, from UGX 10.0 trillion to UGX 11.3 trillion as at 30th June 2019 and realized income grew by 20.4% from UGX 1.05 trillion in 2017/2018 to UGX 1.26 trillion in 2018/2019, the Fund’s management said it will still pay out a real return, at least 2 percentage points above the 10 year average rate of inflation.

Since the 10-year average inflation rate is about 8.7%, we can expect a rate above 10.7% as interest which will still be good- given that the economy grew at 6.1% and the average Treasury bill rate for 364 days during this period was 11.3%.