In a 2007 pre-opening interview with the CEO East Africa Magazine, Manz Denga, the then United Bank for Africa (UBA) Managing Director, spoke strongly about his bank’s ambitions in Uganda.

“Ugandan banking halls are characterised by long queues. I will crash those queues. I will reduce interest rates, improve customer services and be conveniently located and available,” he declared.

At the time, Denga was full of confidence and fire, determined to bring Nigeria’s banking revolution to East Africa. His bank, UBA, was entering Uganda as a greenfield operation and wanted to redefine customer experience in a sector then dominated by traditional incumbents.

“There are 43 different levels of paying fees to the bank. When you withdraw, deposit etc., you pay fees. I prefer to change that and make it very affordable for the customer because in the current setting, all advantages are going to the bank with almost none for the customer,” he lamented.

“It is only the mad man that does things the same way and expects different results.”

He pledged to crush the status quo:

“I have come to do things differently. Having studied the market and having seen what’s happening, the only way I can have an impact on Ugandans and gain their trust is if I do things differently and better.”

Denga even promised a branch rollout strategy and a digital transformation that would push Uganda’s 27 million unbanked citizens into formal finance, boldly declaring:

“We have 29 million Ugandans, but only 1.4 million bank accounts. The rest keep their money under the pillow… Our desire and our primary focus is going to be those people who are not banked—we will go after them.”

But nearly two decades later, UBA and its compatriot Guaranty Trust Bank (GTBank), which entered in 2013 via the acquisition of Fina Bank, have not only failed to “shake down” the market—they have been shaken off it- almost.

A Tale of Unfulfilled Ambition

In March 2024, Guaranty Trust Bank Uganda quietly slipped into Tier II status—a sobering moment for a bank that once promised to be a serious contender in Uganda’s financial sector. The downgrade followed a decision by its shareholders not to inject additional capital in response to the Bank of Uganda’s revised capital requirements, which raised the minimum threshold for commercial banks sixfold—from UGX 25 billion to UGX 150 billion. Rather than meet this new benchmark, GTBank’s owners chose to scale down, effectively stepping back from the top-tier competition and underscoring the bank’s lack of long-term investment appetite in the Ugandan market.

This move was emblematic of a broader pattern of underachievement by Nigerian banks in Uganda. Both GTBank and United Bank for Africa (UBA), despite their confident market entries and Pan-African reputations, have consistently fallen short of expectations. While the sector has experienced tremendous growth over the last decade, these two banks remain anchored at the bottom of the performance tables.

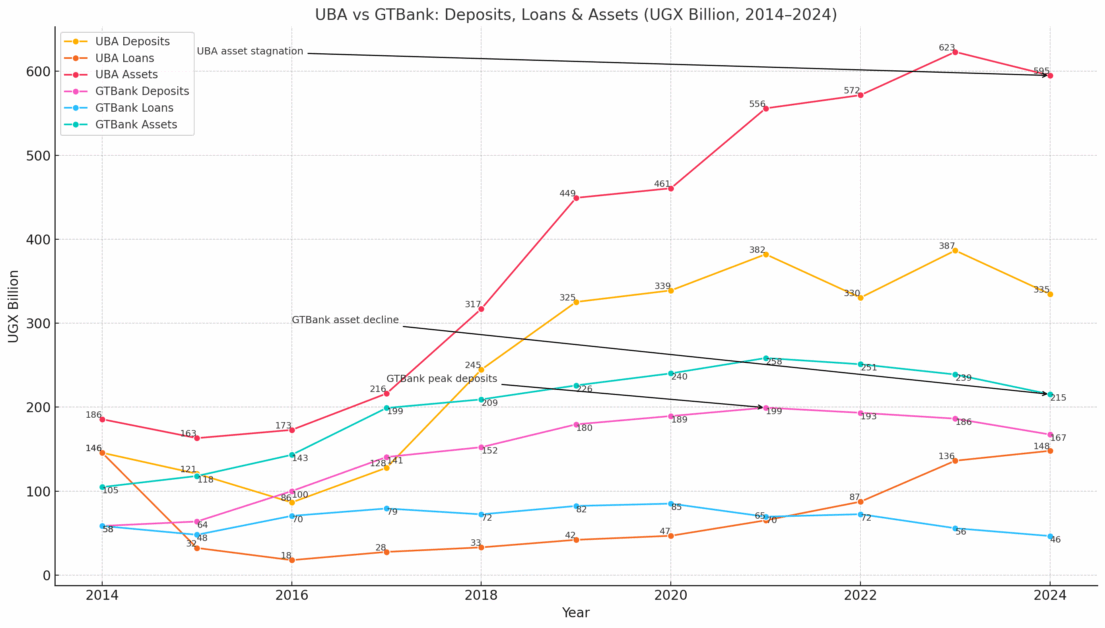

As of December 2024, UBA held customer deposits of UGX 334.6 billion, while GTBank managed UGX 167.4 billion—together accounting for a mere 1.4 percent of the industry’s UGX 35.6 trillion deposit base. In lending, their combined loan portfolio stood at just UGX 194.5 billion out of an industry-wide UGX 21.7 trillion, barely scratching 1 percent of total credit extended by Uganda’s commercial banking sector. Their asset base, too, remained marginal, with UBA at UGX 595.0 billion and GTBank at UGX 215.3 billion—representing a combined market share of only 1.5 percent of the sector’s UGX 53.8 trillion total assets.

Looking at the bigger picture, their performance over the past decade has been anything but transformative. UBA’s customer deposits have grown just 130 percent since 2014—well below the industry average growth of over 198.4 percent during the same period. GTBank, by contrast, has seen its deposit base rise from UGX58.5 billion in 2014, peaking at UGX199.4 billion in 2021 and have been dropping year on year, closing 2024 at UGX167.4 billion.

Between 2014 and 2024, UBA Uganda’s lending performance reflects a decade of volatility, stagnation, and modest recovery. After peaking at UGX 145.7 billion in 2014, the bank’s loan book sharply declined to UGX 17.8 billion by 2016, likely due to internal risk challenges or strategic retreat. Though lending gradually recovered from 2020, reaching UGX 148.0 billion by 2024, this represents only a UGX 2.3 billion net gain over ten years—well below peers who aggressively expanded. Despite a brief surge between 2020 and 2023, UBA’s lending slowed again in 2024, with a low loan-to-deposit ratio under 45%, indicating a liquidity-rich but credit-shy strategy that has left it trailing in Uganda’s competitive banking sector.

Guaranty Trust Bank (GTBank) Uganda has experienced a steady decline in lending over the past decade, with its loan book shrinking from UGX 58.5 billion in 2014 to just UGX 46.5 billion in 2024. After modest growth in the late 2010s, peaking at UGX 85.1 billion in 2020, the bank’s lending activity has consistently dropped year-on-year. This downward trend suggests a deliberate de-risking strategy or structural challenges limiting credit expansion. By 2024, GTBank’s loan-to-deposit ratio had fallen significantly, reinforcing its status as one of the least aggressive lenders among foreign banks in Uganda.

What’s more telling is how both banks appear to be surviving not by lending to customers, but by parking customer deposits into government securities. In 2024, UBA invested UGX 283.5 billion in government paper—an amount nearly equivalent to 85% of its customer deposits. GTBank was no different, with UGX 102.1 billion tied up in securities, representing over 60% of its total deposits. These trends confirm that both institutions are operating primarily as custodians of government debt rather than engines of private sector growth. It’s a model that delivers stability but not impact—and certainly not the transformation they once promised.

In a market where banks like Stanbic, Centenary, Absa, and Equity have multiplied their assets, deposits, and loan books many times over, the stagnation of UBA and GTBank is conspicuous. Their continued reliance on government securities, limited branch expansion, and cautious lending posture have contributed to their diminished relevance.

In contrast to the disruptive wave they once promised, the Nigerian banks now resemble static fixtures, overshadowed by more dynamic, better-capitalised, and locally attuned competitors. What was once marketed as a market shake-up has, over time, morphed into a slow fade.

Patchy Profits: The Mixed Fortunes of UBA and GTBank

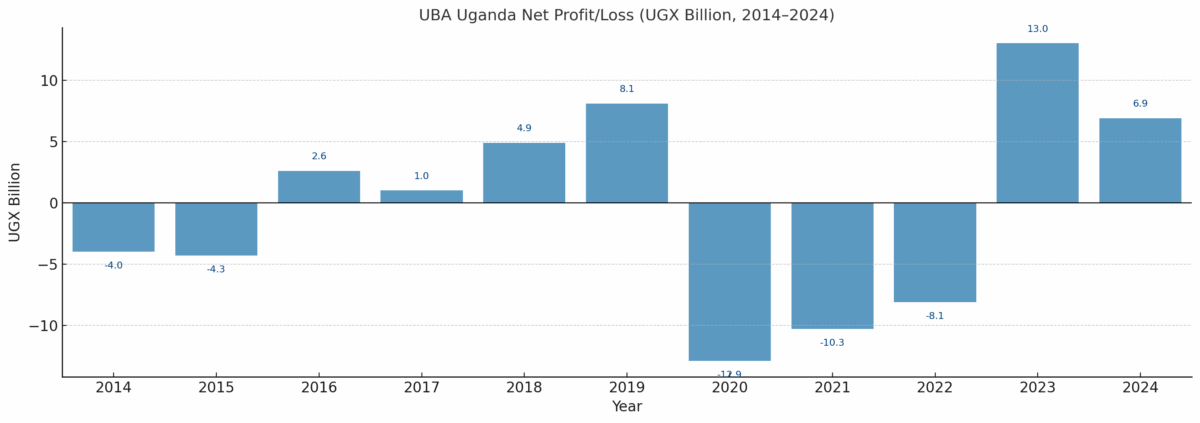

UBA Uganda’s profitability trend from 2014 to 2024 reveals a prolonged struggle to achieve sustainable earnings, marked by years of consecutive losses and only a modest return to profitability in the last two years. Between 2014 and 2021, the bank recorded largely annual losses—including a steep UGX 12.9 billion loss in 2021—largely reflecting weak lending, high operational costs, or impairments. It wasn’t until 2023 that UBA reported a profit of UGX 13.0 billion, followed by UGX 6.9 billion in 2024, signalling a fragile turnaround. However, this recovery remains shallow compared to its earlier losses, and the volatile earnings pattern over the decade highlights the bank’s ongoing difficulty in establishing a consistent and resilient profit base in Uganda’s highly competitive banking sector.

Stanbic’s Five-Year Scorecard: How Profit Growth, Deposits, Lending and Dividends Reshaped Performance

Stanbic’s Five-Year Scorecard: How Profit Growth, Deposits, Lending and Dividends Reshaped Performance

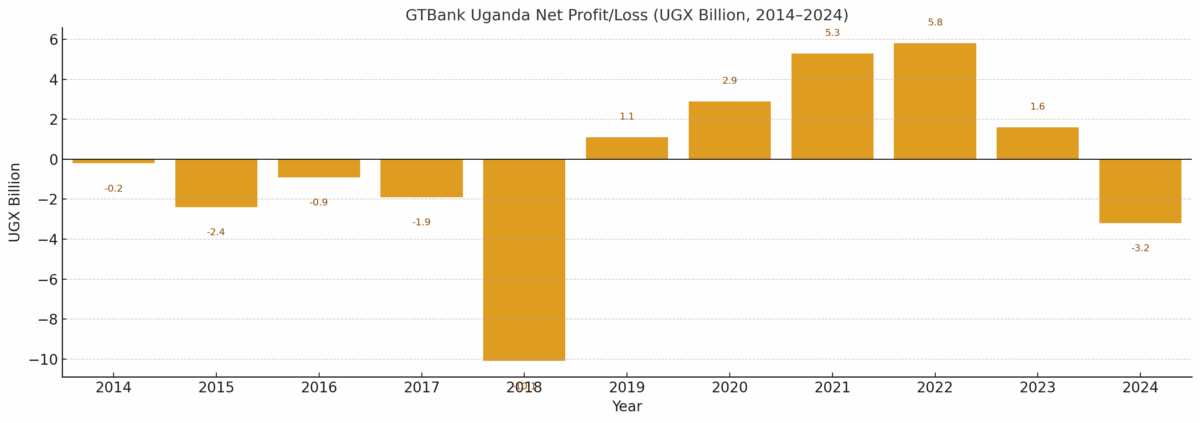

GTBank Uganda’s profit trajectory over the past decade has also been erratic and largely negative, underscoring ongoing operational and strategic challenges. From 2014 to 2020, the bank recorded repeated losses, including a UGX 10.1 billion loss in 2018—its worst performance in the period. A brief turnaround occurred in 2019 and 2023, with modest profits of UGX 1.1 billion, UGX2.9 billion, UGX5.3 billion and UGX 5.8 billion in 2019, 2020, 2021 and 2022 respectively, but this recovery proved unsustainable. By 2023, profits had dwindled to UGX 1.6 billion, and in 2024 the bank slipped back into the red with a UGX 3.2 billion loss. This volatile pattern suggests persistent issues with revenue generation, cost management, or asset quality, leaving GTBank among the least consistently profitable banks in Uganda despite being part of a well-capitalised Pan-African group.

For the Nigerian banks, profitability has not been a result of productive lending or retail growth. Instead, their modest gains have largely been the outcome of conservative investment in government securities and tight cost controls—tactics that may preserve capital, but don’t inspire confidence in long-term market positioning.

The absence of strategic risk-taking, innovation, or aggressive lending not only constrains their income potential—it renders them largely irrelevant in shaping Uganda’s financial development agenda. At a time when other institutions are deeply embedded in sectors such as SME financing, agriculture, fintech, and housing, UBA and GTBank remain on the periphery.

In this light, the struggle for profitability is not just about the numbers—it reflects a deeper failure to build local relevance, institutional resilience, and customer trust.

Local, Kenyan, and South African Banks Are Winning

While Nigerian banks continue to struggle for relevance and profitability in Uganda, local and regional players are steadily strengthening their grip on the market. These banks have embraced Uganda’s financial dynamics, invested consistently, and grown with purpose—often in stark contrast to their Nigerian counterparts.

Stanbic Bank Uganda, backed by South Africa’s Standard Bank Group, remains the undisputed market leader. In 2024, it registered UGX 7.1 trillion in customer deposits, UGX 4.37 trillion in loans, and UGX 10.3 trillion in total assets. Its record UGX 486.8 billion net profit reflects deliberate investment in digital innovation, product depth, and customer relationships.

Among local banks, Centenary Bank stands out with UGX 4.2 trillion in deposits and UGX 3.72 trillion in loans. It posted a net profit of UGX 342.3 billion and grew total assets to UGX 7.1 trillion. Its success stems from rural outreach, agent banking, and strong credit management. Housing Finance Bank (HFB), once a modest performer, also registered impressive growth—UGX 1.6 trillion in deposits, UGX 1.08 trillion in loans, and a record UGX 71.1 billion profit in 2024—driven by a focus on housing finance and salaried lending.

Kenyan banks continue to post strong numbers. Equity Bank Uganda ended 2024 with UGX 2.8 trillion in deposits and UGX 20.1 billion in net profit. DTB Uganda earned UGX 23.7 billion, while KCB Uganda posted UGX 29.9 billion. These banks are lending aggressively and supporting Uganda’s economic sectors.

What sets them apart is their relevance—they lend, innovate, and serve. In contrast, Nigerian banks remain conservative, underperforming, and out of sync with the market’s needs.

A Path to Redemption?

All is not lost—but Nigerian banks must act fast. Their brand equity, Pan-African presence, and historical strength still hold weight. What’s missing is strategic recalibration and deep local execution.

To regain credibility and relevance in Uganda’s banking sector, UBA and GTBank must first aggressively rebuild their loan portfolios. That means re-entering the SME, agriculture, and consumer credit spaces where real economic transformation happens. Surviving on government securities is no longer sustainable—and certainly not competitive.

Second, they must invest boldly in digital transformation. Mobile and agent banking platforms are now the most effective vehicles for reaching underserved and unbanked populations. Regional competitors are deploying tech with precision; Nigerian banks must catch up and localize their digital delivery.

Third, they need to reconnect with their group strategy. Both UBA and GTBank are part of wider Pan-African ecosystems with expertise in cross-border trade, remittance flows, and diaspora banking. These strengths remain untapped in Uganda, where such solutions are sorely needed.

Finally, governance and leadership must evolve. It’s time for the boards and executive teams to align around a long-term view—one that prioritizes market development, customer intimacy, and cultural adaptation over headquarters-led cost containment.

The Thunder That Never Struck

The promise was loud. The ambition was real. In 2007, Manz Denga, then CEO of UBA Uganda, pledged to crash queues, lower interest rates, and shake the industry. But seventeen years on, those declarations remain unfulfilled.

Instead of shaking the market, UBA and GTBank have been quietly overtaken by banks that built trust, earned deposits, extended credit, and solved problems at the grassroots. They came to lead but fell behind—outpaced by those who chose substance over slogans.

Unless Nigerian banks urgently rediscover their purpose and adapt to the market realities around them, they risk becoming little more than a footnote in Uganda’s banking evolution—a cautionary tale of ambition unfulfilled and the thunder that never struck.