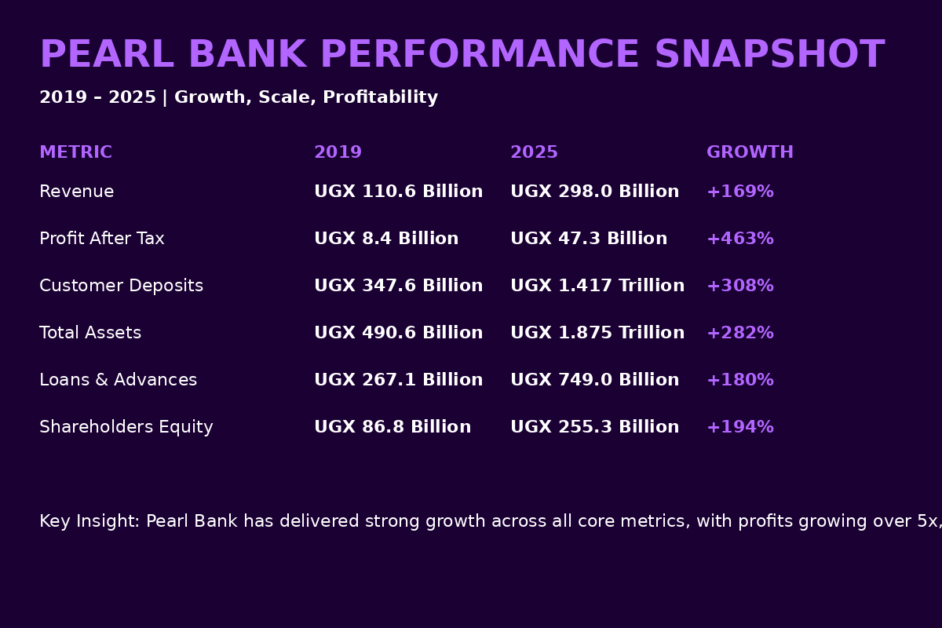

Pearl Bank Uganda has stepped into its new identity with both regulatory endorsement and strong financial muscle, posting a profit after tax (PAT) of UGX 47.3 billion for the year ended December 2025, cementing its transition from PostBank into what is fast emerging as a formidable indigenous commercial banking force.

The timing is strategic. On 24th November 2025, the Bank of Uganda (BoU) issued an operating license formally recognising the institution as Pearl Bank Uganda Limited, marking the culmination of a deliberate transformation journey.

The license, handed to Managing Director Julius Kakeeto by BoU Governor Dr. Michael Atingi-Ego, was more than regulatory compliance; it was a symbolic endorsement of a bank that has steadily evolved from a legacy savings institution into a modern, digitally driven, Tier 1 commercial bank.

That is part of what makes Pearl Bank’s broader evolution noteworthy. This is an institution with roots going back to 1926, first as a postal savings department and later as PostBank Uganda, before entering a new phase of accelerated transformation under Julius Kakeeto’s leadership from October 2019.

His appointment marked a turning point, catalysing reforms that drove measurable expansion across the bank’s operations, including a wider branch network, deeper digital transformation, a strengthened agency banking model and greater penetration into local enterprises.

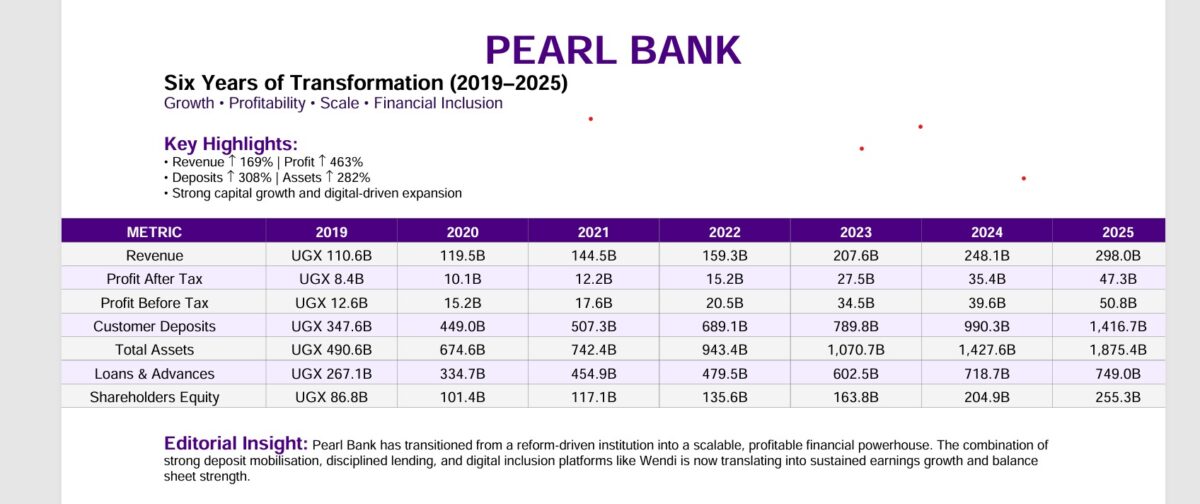

The milestones are now familiar: Tier 1 status in 2021, the launch of Wendi in 2023, and the official rebrand to Pearl Bank in 2025.

What gives those milestones weight now is that they are increasingly being matched by audited commercial performance with a positive profit trajectory from UGX 8.4 billion in 2019 to UGX 47.3 billion in 2025.

Pearl Bank’s 2024-2028 strategy itself remains centred on two high-impact goals: driving sustainable financial inclusion and stimulating entrepreneurship and service delivery, particularly in agriculture and SMEs.

This rebrand is not cosmetic. It sits on top of a balance sheet and income statement that tell a deeper story of scale, discipline, and ambition.

2025: A year of growth

Pearl Bank Uganda closed 2025 with strong earnings and balance-sheet expansion, posting profit after tax of UGX 47.3 billion, up from UGX 35.4 billion a year earlier, as total income climbed to UGX 298.0 billion and the bank deepened its funding base through a sharp rise in customer deposits.

The headline number matters because it shows the bank grew profit faster than revenue.

Profit before tax rose to UGX 50.8 billion from UGX 39.6 billion, while PAT increased by 33.8%, outpacing the 20.1% rise in total income. That suggests Pearl Bank was not merely getting bigger; it was also converting more of its revenue into bottom-line earnings. The tax charge also fell to UGX 3.5 billion from UGX 4.2 billion, helping lift net profit.

A close reading of the numbers shows this was, above all, a funding-led growth story. Customer deposits jumped to UGX 1.417 trillion from UGX 990.3 billion, a rise of roughly 43%, giving the bank a much larger funding base.

That matters for the broader narrative around the bank’s rise as an indigenous brand. A bank that is increasingly funded by its own customers is, in a very practical sense, becoming more deeply rooted in the market it serves.

In Pearl Bank’s case, that lines up with its stated ambition to be a homegrown institution delivering both profit and purpose, especially in financial inclusion and enterprise support.

At the same time, total assets expanded by about 31.4% to UGX 1.875 trillion. That scale-up was not matched by equally aggressive loan growth: net loans and advances rose only to UGX 749.0 billion from UGX 718.7 billion, about 4.2%.

Instead, Pearl Bank placed a much bigger share of its balance sheet into investment securities, which surged to UGX 614.6 billion from UGX 364.5 billion, a rise of about 68.6%.

That shift says a lot about management’s posture. The bank appears to have chosen a more defensive asset mix in 2025, leaning harder into securities while still keeping loan growth positive.

This helps explain why interest income from investment securities rose to UGX 76.7 billion from UGX 56.3 billion, while interest on loans and advances increased to UGX 172.3 billion from UGX 151.9 billion. Loans remained the single biggest revenue engine, but securities did more of the heavy lifting than in the prior year.

Revenue growth

Revenue growth was broad-based. Total income increased to UGX 298 billion from UGX 248.1 billion.

The largest line remained interest on loans and advances, but there were also gains in net fee and commission income, which rose to UGX 31.3 billion from UGX 29.3 billion, in foreign exchange income, which nearly tripled to UGX 3.0 billion from UGX 1.0 billion, and in other income, which rose to UGX 834.7 million from UGX 370.5 million.

This matters because it shows Pearl Bank’s growth was not solely dependent on lending spreads; fee income and treasury-related earnings also improved.

The pressure point was funding cost. Interest expense on deposits rose sharply to UGX 55.7 billion from UGX 35.5 billion, an increase of about 56.9%, reflecting both the much larger deposit base and a tighter interest rate environment.

As the bank attracted significantly more customer deposits, it inevitably had to pay more to retain and grow those balances, especially in a market where competition for deposits has intensified.

However, this increase in deposit costs needs to be viewed alongside a notable shift in the bank’s overall funding structure.

Interest expense on borrowings fell sharply to UGX 1.74 billion from UGX 7.63 billion, while borrowings on the balance sheet declined to UGX 38.2 billion from UGX 43.9 billion.

This indicates that Pearl Bank reduced its reliance on external or wholesale funding sources, which are typically more expensive and less stable than customer deposits.

Costs did rise materially. Operating expenses increased to UGX 157.1 billion from UGX 129.8 billion, while other expenses rose to UGX 23.2 billion from UGX 21.5 billion.

#CEOOfTheWeek: Mumba Kalifungwa — Unlocking Stanbic’s Lending Power to Drive Uganda’s Growth

#CEOOfTheWeek: Mumba Kalifungwa — Unlocking Stanbic’s Lending Power to Drive Uganda’s GrowthStill, the bank got relief from a lower impairment charge: provisions for bad and doubtful debts fell to UGX 8.06 billion from UGX 12.64 billion.

That decline in credit provisioning was a major contributor to stronger profitability. It indicates the bank either saw fewer new problem loans, better recoveries, or a more stable risk environment in its book.

Asset quality improved, though not enough to remove all concern. Non-performing loans and other assets declined to UGX 37.9 billion from UGX 40.6 billion.

Against a larger loan book, that implies a ratio of roughly 5.1%, down from about 5.7% in 2024. That is a step in the right direction.

However, problem assets remain significant. Interest in suspense edged up to UGX 8.62 billion from UGX 8.25 billion, showing that some borrowers are still struggling to repay.

At the same time, the bank wrote off UGX 14.9 billion in bad debts, up from UGX 9.4 billion, as it continues to remove older, unrecoverable exposures from its books.

Capital is one of the clearest positives in the statement and provides an important layer of comfort around the bank’s growth.

Core capital rose to UGX 227.9 billion from UGX 184.3 billion, while total qualifying capital increased to UGX 239.8 billion from UGX 196.0 billion, reflecting retained earnings and shareholder support.

At the same time, risk-weighted assets (RWA), which measure the bank’s exposure to risk from lending and other activities, increased more modestly to UGX 964.1 billion from UGX 900.5 billion. Because capital grew faster than these risk exposures, the bank’s capital buffers strengthened.

As a result, the core capital to RWA ratio improved to 23.64% from 20.47%, while the total capital ratio rose to 24.87% from 21.77%.

These ratios are key regulatory indicators that show how much capital the bank has relative to the risks it is taking.

In practical terms, this means Pearl Bank is better positioned to absorb potential losses, support future lending growth and remain compliant with regulatory requirements.

It also suggests that the bank is expanding from a position of strength, with enough capital headroom to back its ambitions in SME financing, agriculture and broader financial inclusion.

Those are strong capital cushions and give Pearl Bank more room to absorb shocks and support future asset growth.

Shareholders’ equity also strengthened to UGX 255.3 billion from UGX 204.9 billion, driven mainly by higher share capital of UGX 203.5 billion and retained earnings of UGX 47.5 billion.

The decision by directors not to recommend a dividend means more earnings will stay in the business, supporting solvency and growth capacity. For a bank still expanding rapidly, that is a conservative but logical capital allocation decision.

Wendi wallet deposit growth

One of the clearest intersections between Pearl Bank’s commercial performance and its inclusion agenda is Wendi, whose wallet deposits surged to UGX 240.5 billion from UGX 45.5 billion.

Launched in 2023 as a digital financial platform to accelerate sustainable financial inclusion, Wendi has rapidly moved from innovation to impact. It brings banking into the daily lives of Ugandans, enabling users to save, send money, pay utilities, transact across borders and support SACCOs nationwide.

Wendi is no longer just a digital product. It is emerging as a meaningful deposit engine and a clear proof point that financial inclusion can translate into commercial scale. For a bank built around fostering prosperity, it is where purpose and profitability visibly converge.

The scale of Wendi adoption is already evident. The 2025 deposit figure signals strong customer uptake, positioning Wendi not just as an access channel, but as a growing funding base anchored in everyday financial activity.

Recognition has also followed performance.

In 2025, while still operating as PostBank, the institution was named Best Performing Bank under the Small Business Recovery Fund and Agricultural Credit Facility by Bank of Uganda, and it also received sustainability certification from the European Organisation for Sustainable Development.

Those details help locate the bank’s progress within a broader public-policy and development context, rather than as a purely internal financial story.

There are still areas to watch. The bank now has a much larger deposit base than loan book growth would suggest, which raises a fair question about deployment.

Can Pearl Bank translate that funding strength into faster, high-quality lending without reviving credit stress? Can it deepen SME and agricultural financing while holding the line on asset quality? Can Wendi keep scaling in a way that remains both accessible and economically productive?

Those are not criticisms of the 2025 result. They are the next tests implied by it. For now, the broad picture is clearer than ever. Pearl Bank entered 2026 better capitalised, more liquid, more deposit-funded and more profitable than it was a year earlier.