You recently cut your prime lending rate to 16 percent, for the second time this year. This is a rather unexpected move, given the probable likelihood of increased Non-Performing Loans and other Covid-19 related risks. What are the insights behind this decision?

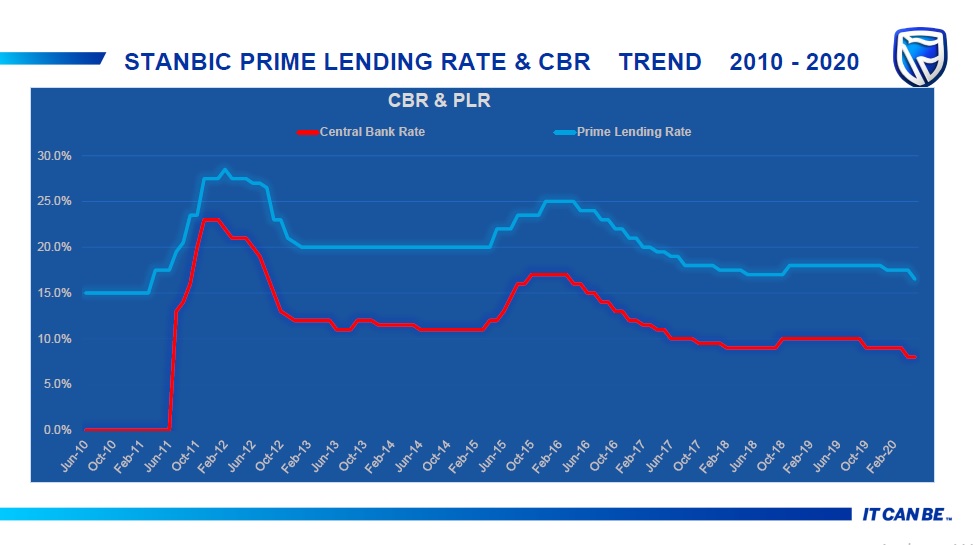

Stanbic has consistently re-priced our prime lending rate in response to every CBR movement by the Central Bank over the past 10 years and at present, Stanbic has one of the lowest prime lending rates of all active retail financial institutions in the country. We lowered our base lending rates in line with the CBR cut in April 2020 during the pandemic. The Central Bank has further revised CBR in June 2020 and effective 1st August 2020, we are reducing our prime lending rate to 16.0%. We aim to ensure our customers can benefit from more affordable lending rates as interest rates in the market are reviewed.

Beyond affordable interest rates, to support businesses during this Covid-19, we offered credit relief programmes to business and personal customers tailored to suit their circumstances. Our aim was to ensure that we see that their businesses are sustained and the impact on the economy is minimised. We also waived all charges on our digital banking platforms so that customers could transact free of charge on our platforms like online Banking and Mobile Banking systems to make day to day payments and account to mobile money transactions.

During Stanbic’s credit relief programme, how many loans or what percentage of your loans have been restructured?

The most recent reports from the BOU indicate that at an industry level, approximately 14% or UGX 2.02 trillion of the total banking loan portfolio of UGX 14.7 trillion, as at April 2020 has been restructured. Within Stanbic Bank, over 1,518 loans have been restructured and a majority are within the personal markets and SME sector.

Naturally, the SME sector, in the face of Covid-19 and with its inherent issues, is the most vulnerable. How have you supported the SME sector to make sure it stays aloft?

Stanbic has a portfolio of over 40,000 SME clients and a key step we took during the pandemic was to offer credit relief programmes. We encouraged all our SME customers whose incomes have been impacted as a result of Covid-19 to apply for a loan repayment holiday based on their unique circumstances. Over 60% of the loans restructured in the Stanbic’s portfolio have been SMEs.

Inside the Balance Sheet: CFO Doreen Kyomugisha on Building Capital Strength and Financial Discipline at SanlamAllianz General Uganda

Inside the Balance Sheet: CFO Doreen Kyomugisha on Building Capital Strength and Financial Discipline at SanlamAllianz General UgandaWe have encouraged Businesses to sign-up on to our Digital platforms specific for SMEs (Business Online & Enterprise Online) where we also waived some of the digital transactions. Other alternate platforms we provided include the Cash Deposit Machines (CDMs) and for larger clients the option of enrolling the services of Cash in transit (CIT).

But more important is the Stanbic Business Incubator, a key initiative that we drive that supports SMEs by providing training and capacity development. The trainings are free charge for SME’s and more importantly – you do not have to be a Stanbic client to apply and participate. We have also expanded this programme and successfully launched regional incubator centres in Hoima, Mbarara and Gulu to avail training and development opportunities to SME’s upcountry. To date, more than 1,489 entrepreneurs from over 650 SMEs have been successfully trained and graduated. So in summary during Covid-19 and even before Covid-19, Stanbic has supported SMEs with affordable loans and skills to fully and beneficially utilise those loans and now in the face of Covid-19, we are working with the SMEs to navigate the rough waters and emerge stronger.

Looking ahead and considering the Covid-19, how will the banking sector be affected?

The pandemic presents an opportunity for us to reshape the way we deliver financial services to our clients. A lot of work must be done working in close collaboration with the Government to ensure the right measures and policies are put in place to sustain the economy.

That said, the Impact of COVID-19 on the financial sector is going to be a lagged one. Unlike sectors such as tourism, media, consumer and commercial real-estate where the impact has been immediate and can easily be quantified, the impact on the Financial sector is always delayed and time for recovery is also expected to take longer (this can reach up to 2 years as witnessed through previous cycles). This is driven by the fact that we are cushioning businesses right now through waivers and credit restructures while following the central bank guidelines. Various sectors have different recovery times, and some could extend to over a year. Depending on how these recover, the banking sector may be forced to take in extra credit provisions which will impact non-performing loans ratios of the sector.

However, we remain optimistic given the relaxed measures put in by the government to reopen activities and business. We hope to see some business activity pick up over the coming months. As Stanbic, we are committed to our purpose, to drive Uganda’s growth and continue to take the necessary actions to support our clients and contribute to the growth of Uganda’s economy.