To begin with, the licence downgrade was not the result of weak performance or regulatory distress. Rather, it stemmed from structural shifts in Uganda’s banking regulatory framework.

In recent years, the Bank of Uganda significantly increased minimum capital requirements for Tier I commercial banks, lifting the threshold to UGX 150 billion.

This policy move—designed to strengthen systemic resilience and reduce risk in the banking sector—forced several otherwise sound institutions to reassess their strategic positioning, capital efficiency, and long-term focus.

Finance Trust Bank’s transition must therefore be understood within this broader regulatory and policy context, rather than as a reflection of institutional weakness.

Finance Trust Bank’s strong performance and growing balance sheet had, in fact, attracted the interest of a credible strategic partner—Access Bank of Nigeria.

Discussions around a potential transaction reflected confidence in FTB’s fundamentals and franchise value.

However, the deal ultimately fell through, which CEO East Africa Magazine understands was largely due to developments outside Uganda.

Nigeria’s regulator, the Central Bank of Nigeria, significantly raised capital requirements for Nigerian banks with international and cross-border footprints, compelling institutions such as Access Bank to prioritise domestic capital consolidation over regional expansion.

Against this backdrop, Finance Trust Bank opted for a strategic repositioning—aligning its licence category with its capital structure and core customer focus, rather than pursuing costly capital raising in a tightening regulatory environment.

A Credit Institution (Tier II) is a fully licensed, deposit-taking financial institution regulated and supervised by the Bank of Uganda.

Like a Tier I commercial bank, it is authorised to mobilise deposits, extend credit, provide payment services, and conduct foreign exchange transactions, and it operates under the same prudential supervision and reporting standards.

The key difference lies not in safety or regulation, but in scope and scale.

Tier I commercial banks are permitted to offer the widest range of banking services, including current accounts, overdrafts, and certain interbank and corporate treasury activities.

Tier II Credit Institutions, by contrast, operate with a more focused product set, concentrating on savings, deposits, lending, trade-related guarantees, payments, and foreign exchange—without engaging in some higher-risk or capital-intensive activities that are reserved for Tier I banks.

Crucially, both Tier I and Tier II institutions are fully regulated, supervised, and examined by the Bank of Uganda, and both are required to meet strict standards on capital adequacy, liquidity, governance, and risk management.

For customers, this means the core banking relationship—saving, borrowing, transacting, and accessing financial services—remains secure and uninterrupted.

In practice, the Tier II model allows institutions such as Finance Trust Bank to align capital more efficiently with their core customers—particularly retail clients, SMEs, and women-led enterprises—while maintaining regulatory discipline and financial stability.

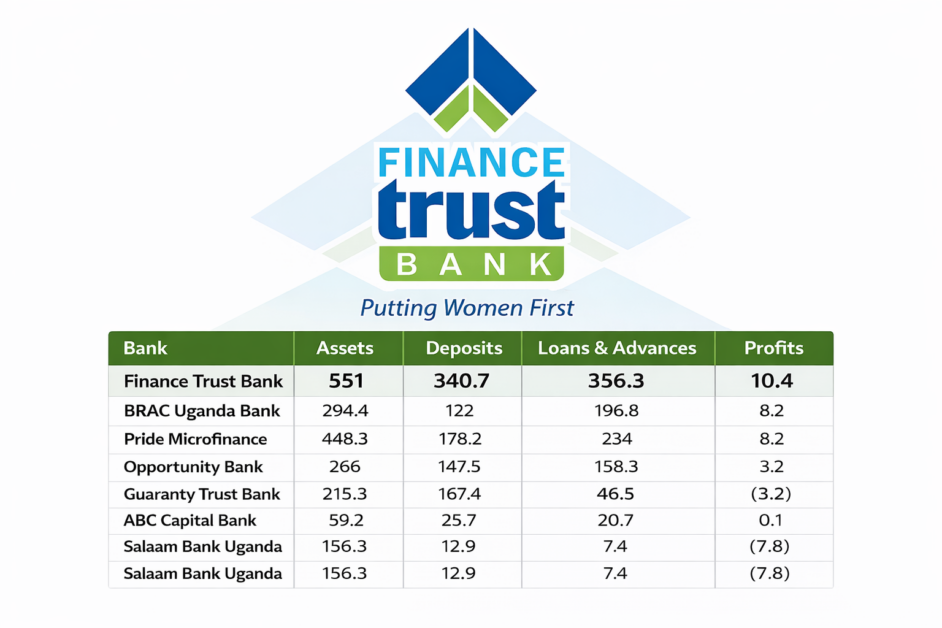

Finance Trust Bank now operates in this category alongside other credible, regulated institutions such as BRAC Uganda Bank, Pride Microfinance Bank, and Guaranty Trust Bank Uganda.

Collectively, these institutions account for about UGX 1.2 trillion in assets, UGX 872 billion in deposits, and over UGX 786 billion in lending.

Based on 2024 audited figures, Finance Trust Bank alone controls roughly 45% of segment assets, nearly 40% of deposits, and close to 50% of total lending, while also standing out as the most profitable institution in the segment.

Against that backdrop, here are 10 things customers and stakeholders should know.

1. Finance Trust Bank remains financially strong and profitable

As noted above, Finance Trust Bank enters the Tier II Credit Institution category as its clear market leader, not as a marginal player.

As of 2024, the bank reported UGX 551 billion in total assets, UGX 340.7 billion in customer deposits, UGX 356.3 billion in loans and advances, and a profit after tax of UGX 10.4 billion.

On these metrics, Finance Trust Bank accounts for about 45% of total Tier II assets, nearly 40% of deposits, and close to 50% of lending in the segment, while also standing out as the most profitable institution among its peers.

These are not the numbers of a bank under distress. They represent one of the strongest financial positions in the bank’s history and underscore the fact that the licence transition did not follow weakening performance, but rather preceded from sustained strength.

Notably, the bank’s loan book exceeds customer deposits, signalling active financial intermediation rather than passive liquidity holding.

Profitability has also strengthened in a challenging operating environment, reflecting disciplined growth and sound risk management.

In short, Finance Trust Bank is repositioning from a position of strength, with its core financial fundamentals firmly intact.

2. Growth has been consistent for more than a decade—not speculative

Beyond its current scale, what distinguishes Finance Trust Bank is the consistency of its growth over time.

Since 2011, the institution has expanded steadily across all its core balance-sheet lines—assets, deposits, and lending—over more than a decade, without the boom-and-bust cycles that have characterised parts of the sector.

Based on available historical performance trends:

- Total assets have grown from under UGX 100 billion in 2011 to UGX 551 billion in 2024, representing a compound annual growth rate (CAGR) of roughly 15–17%.

- Customer deposits have increased from under UGX 50 billion to UGX 340.7 billion, translating into a CAGR of approximately 18–20%.

- Loans and advances have expanded at a similar pace, reaching UGX 356.3 billion in 2024, with lending growth broadly tracking deposit mobilisation rather than outpacing it.

Crucially, this expansion has been achieved while:

- Avoiding sharp balance-sheet spikes or contractions

- Maintaining profitability across multiple economic cycles, including the COVID-19 period

- Preserving focus on core retail, SME, and women-led enterprise customers

The 2024 performance, therefore, is not a one-year anomaly or a late-cycle surge, but the latest point in a long, incremental growth trajectory built on discipline rather than speculation.

For stakeholders, this matters: institutions that grow steadily over a decade tend to manage transitions better than those built on short bursts of scale.

3. The transition is regulator-approved and fully supervised

The transition of Finance Trust Bank to a Tier II Credit Institution was approved by—and remains under the full supervision of—the Bank of Uganda.

This distinction is critical. The licence change was not accompanied by statutory management, not triggered by regulatory intervention, and did not involve any suspension of operations.

Finance Trust Bank continues to operate normally under Uganda’s financial laws, subject to the same prudential oversight, reporting requirements, and on-site examinations that govern all licensed deposit-taking institutions.

In regulatory terms, this was a structured, orderly transition, not a corrective action.

For customers and counterparties, that means business continuity, legal certainty, and uninterrupted access to banking services.

Simply put, the regulator remains fully engaged—and fully confident—in the institution’s ongoing operations.

4. Customer deposits remain safe and fully accessible

For customers, the most important question is a simple one: Is my money safe?

The answer is yes.

Customer deposits at Finance Trust Bank remain fully protected under Uganda’s financial regulatory framework and continue to be held within a licensed, supervised deposit-taking institution.

The transition to a Tier II Credit Institution has not altered customers’ rights or access to their funds.

All customer accounts remain open and fully accessible, with existing deposit, loan, and contractual agreements continuing unchanged.

Branches across the country remain operational, while digital banking channels—including electronic payments and mobile platforms—continue to function normally.

Importantly, customers are not required to close, transfer, or renegotiate their accounts as a result of the licence change.

Day-to-day banking activities—saving, transacting, borrowing, and accessing funds—continue without interruption.

5. Most products continue—some are simply more focused

Under the Tier II Credit Institution licence, Finance Trust Bank continues to offer the core banking products that serve the vast majority of its customers.

These include:

- Savings and fixed deposit accounts

- Loans to individuals, SMEs, and women-led enterprises

- Foreign exchange buying and selling

- Guarantees, including performance and bid bonds

- Digital banking, payments, and remittance services

The changes arising from the licence transition are limited and specific, and largely affect products reserved for Tier I commercial banks:

- No new current accounts

- No new overdrafts

- Certain Tier I-only interbank and treasury activities are phased out

Importantly, the Bank of Uganda has provided a three-month transition period to allow for an orderly adjustment.

During this period, existing arrangements are being wound down in line with regulatory guidance, ensuring customers experience no disruption and have adequate time to adjust where necessary.

#WomenFixingUganda: Q&A with Leadership Coach Eileen Walusimbi on Conscious Leadership That Builds Lasting Organisations

#WomenFixingUganda: Q&A with Leadership Coach Eileen Walusimbi on Conscious Leadership That Builds Lasting OrganisationsFor the majority of customers—particularly retail clients, SMEs, and women-led enterprises—day-to-day banking remains unchanged, with uninterrupted access to savings, credit, payments, and foreign exchange services.

6. Finance Trust Bank is still lending—at scale

One of the clearest indicators of institutional health in banking is lending activity, and on this measure, Finance Trust Bank remains firmly in expansion mode.

With UGX 356.3 billion in loans and advances outstanding as of 2024, Finance Trust Bank is the largest lender in the Tier II Credit Institution segment, accounting for nearly half of all lending within this peer group.

Its loan book exceeds that of several institutions operating under the same licence category and rivals those of some Tier I banks.

Crucially, this lending is concentrated in the real economy.

The bank continues to actively finance small and medium-sized enterprises, women-led businesses, and households, supporting trade, services, agriculture, and livelihoods across the country.

These numbers underscore an important point: this is not a bank retreating from its intermediation role.

On the contrary, Finance Trust Bank remains one of the most active credit providers in its category, continuing to deploy capital where it matters most.

7. Women remain at the centre of the business model

Finance Trust Bank’s identity as a women-first bank remains firmly intact, and the transition to a Tier II Credit Institution has not altered this core positioning.

Women account for more than half of the bank’s customer base, making them the single largest constituency Finance Trust Bank serves.

On the lending side, an estimated 45–50% of the loan portfolio is linked to women borrowers—either through women-owned enterprises, women-led SMEs, or individual lending to women across trade, services, agriculture, and small-scale manufacturing.

In absolute terms, this translates into well over UGX 150 billion of the bank’s UGX 356.3 billion loan book directly supporting women’s economic activity.

Over recent years, Finance Trust Bank has also channelled more than UGX 20 billion through structured women-focused financing programmes, reaching over 1,000 women entrepreneurs nationwide.

These are on-balance-sheet, commercially priced loans, not grants or CSR initiatives.

This focus is not incidental. It is rooted in the bank’s origins and ownership structure, with women’s economic empowerment embedded in its founding mandate and shareholder DNA.

That alignment has ensured continuity of purpose across regulatory transitions, economic cycles, and changes in licence category.

For women customers—who form the backbone of the bank’s retail and SME franchise—the message is clear: the licence has changed, but the bank’s commitment to financing women has not.

8. The bank is backed by strong, long-term shareholders

Finance Trust Bank continues to be owned by a group of mission-aligned, patient shareholders whose investment philosophy is centred on stability, inclusive finance, and long-term value creation, rather than short-term exits.

At the core of this ownership structure is Uganda Women’s Trust, the bank’s founding and anchor shareholder.

The Trust has been central to Finance Trust Bank’s journey from its microfinance origins to a regulated deposit-taking institution, embedding a long-standing commitment to women’s economic empowerment and local ownership.

The bank is also backed by several international development and impact investors with deep experience in building resilient financial institutions in emerging markets.

These include Oikocredit, a Netherlands-based global cooperative and one of the world’s largest social impact investors, known for its long-term support to inclusive finance institutions across Africa, Asia, and Latin America.

Other shareholders include Progression Eastern Africa Microfinance Equity Fund and RIF North 1, both of which are specialist investment vehicles focused on financial services in Africa.

These investors bring capital discipline, governance oversight, and regional banking expertise, reinforcing the bank’s prudential and risk-management culture.

Finance Trust Bank’s shareholder base is further complemented by Investisseurs & Partenaires, a pan-African investment group with a long track record of supporting SMEs and financial institutions that combine commercial sustainability with developmental impact.

Importantly, the collapse of the proposed transaction involving Nigeria’s Access Bank did not weaken Finance Trust Bank’s ownership base or destabilise governance.

The development reflected changes in capital requirements outside Uganda, rather than any deterioration in Finance Trust Bank’s fundamentals. Ownership remained intact, board oversight unchanged, and strategic direction consistent.

For customers and stakeholders, this ownership profile matters. Patient, mission-driven shareholders are a critical stabilising force in banking, particularly during regulatory transitions.

In Finance Trust Bank’s case, the shareholder base remains a source of continuity, credibility, and long-term confidence.

9. Leadership continuity—and institutional memory—provide stability

At a time of structural change in the banking sector, leadership continuity matters—and on this front, Finance Trust Bank enters its Tier II phase with a clear advantage.

A critical source of this stability has been continuity in leadership and governance, reinforced by the combined strength of a seasoned executive team, an experienced Board of Directors, and long-term, mission-aligned shareholders.

This alignment between management execution (ExCo), board-level oversight, and shareholder guidance has provided the institutional memory and strategic consistency required to navigate regulatory transitions, economic shocks, and periods of sustained balance-sheet expansion.

At the centre of this structure is Managing Director Annet Nakawunde Mulindwa, whose tenure spans more than a decade of sustained, measurable growth.

When Annet assumed leadership in the early 2010s, Finance Trust Bank was still a relatively small institution. In 2011, the bank reported UGX 46.1 billion in customer deposits, UGX 46.1 billion in loans, and UGX 92.2 billion in total assets.

By 2024, those figures had expanded significantly:

- Customer deposits: UGX 340.7 billion, up from UGX 46.1 billion

- Loans and advances: UGX 356.3 billion, up from UGX 46.1 billion

- Total assets: UGX 551.0 billion, up from UGX 92.2 billion

- Profit after tax: UGX 10.4 billion, compared to low single-digit billions in the early 2010s

Over the 13-year period from 2011 to 2024, this performance translates into consistent double-digit compound annual growth rates:

- Deposits: CAGR of approximately 17–18%

- Loans: CAGR of approximately 18–19%

- Assets: CAGR of approximately 15–16%

- Profitability: steady expansion, achieved without extreme volatility or sharp earnings swings

What makes this record particularly notable is when it was achieved. The growth spans several stress periods: the transition from MDI to Tier I commercial bank in 2013, the COVID-19 economic shock, and the recent capital-regulatory tightening that reshaped Uganda’s banking landscape.

Throughout these phases, Finance Trust Bank avoided boom-and-bust balance-sheet behaviour and remained profitable, even as some peers recorded losses.

This outcome is closely linked to institutional memory—the accumulated experience of leadership that has managed the bank across different regulatory regimes and economic cycles.

That continuity extends beyond the Managing Director to a stable Executive Committee (ExCo) overseeing credit, risk, and operations, and an experienced Board of Directorsproviding governance oversight, strategic direction, and regulatory engagement.

For regulators, customers, and shareholders, the implication is clear: Finance Trust Bank enters its Tier II phase guided by leadership that has already delivered sustained, data-verifiable growth over more than a decade—and understands the institution deeply enough to manage structural change without destabilising it.

10. This is strategic repositioning, not retreat

The transition to a Tier II Credit Institution reflects a deliberate strategic choice, not a withdrawal from the market. In a tightening regulatory environment—defined by higher capital thresholds and increased supervisory expectations—Finance Trust Bank has opted to realign its licence with its capital structure, risk appetite, and core customer base.

By prioritising financial sustainability, capital efficiency, and lending impact, the bank has sharpened its focus on the segments where it has built scale and expertise over more than a decade—retail customers, SMEs, and women-led enterprises.

This approach allows Finance Trust Bank to continue deploying capital actively into the real economy, while avoiding the balance-sheet strain and risk dilution that can accompany size-for-size’s-sake expansion.

Importantly, this repositioning preserves what matters most to customers: deposit safety, access to credit, and continuity of service. Rather than pursuing optics or rapid scale at any cost, the bank has chosen resilience, discipline, and long-term value creation.

In that sense, the licence change is but a refinement—one that positions Finance Trust Bank to remain strong, relevant, and impactful in its chosen markets.

The bottom line

Finance Trust Bank’s transition to a Tier II Credit Institution does not signal weakness. On the contrary, the evidence points to a profitable, well-capitalised, and actively lending institution that enters the Tier II space as its clear category leader by assets, deposits, lending, and profitability.

That strength is reflected not only in the numbers—UGX 551 billion in assets, UGX 340.7 billion in deposits, UGX 356.3 billion in lending, and UGX 10.4 billion in profit after tax—but also in external validation. Recognition under the Bank of Uganda’s Agricultural Credit Facility, strong performance in the Small Business Recovery Fund, attainment of ISO 27001:2022 certification, and sustained backing by development and impact investors all reinforce confidence in the bank’s governance, risk management, and institutional quality.

For customers and stakeholders, the message is therefore clear and unambiguous:

the licence has changed, but the strength, stability, and purpose of the institution have not.

In choosing focus, resilience, and long-term sustainability over optics, Finance Trust Bank has not stepped back—it has positioned itself to endure.