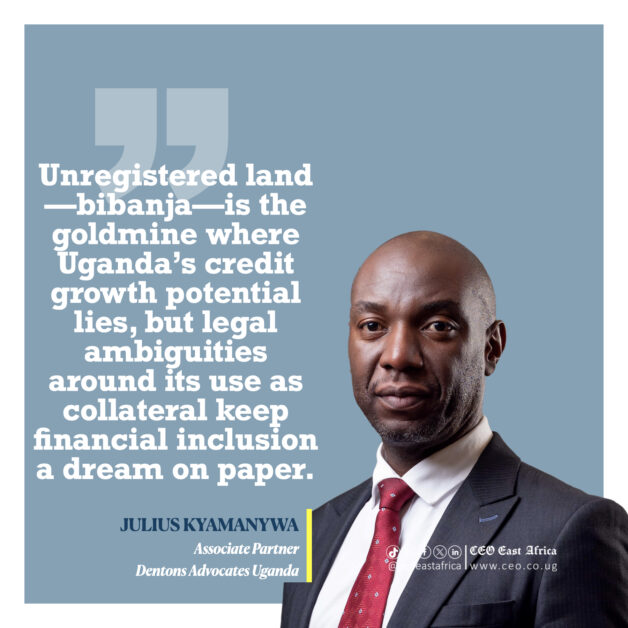

Over 50% of Uganda’s GDP is attributed to the informal sector (UBOS 2024 Census Report). It is therefore inevitable that financial institutions have to tap into it to sell their financial products (including loans). In fact, this is the goldmine in which most potential for credit growth and lending lies. However, a significant number of small and medium business owners in Uganda hold unregistered plots of land (bibanja in Central Uganda) which are tendered as collateral for loans.

For legal context, the Constitution of the Republic of Uganda recognises unregistered customary land as one of the four tenure systems. Article 237 provides that, “Land in Uganda belongs to the citizens of Uganda and vests in them in accordance with the following land tenure systems— (a) customary; (b) freehold; (c) mailo; and (d) leasehold”. The Land Act and Courts of Law have followed suit and affirmed this position as well.

In a bid to increase access to credit and to widen the bankable population, the World Bank and Bank of Uganda, under its Small Business Recovery Fund initiative, have already considered unregistered land (bibanja) as viable collateral for loans. The challenge now lies with Board Credit Committees supported by their Heads of Credit, Risk and Legal, with the guidance of experienced legal practitioners, to amend their Credit Policies to accommodate unregistered land as viable collateral. The relevant legislation governing the pledging of unregistered land has partly aligned with these developments. The question to determine is whether it is sufficient thus far.

Indeed, The Mortgage Act, as amended in 2009, introduced the novel concept of the ‘Informal Mortgage’ to facilitate pledging of unregistered plots of land as security for loans. Under Section 2 of the Mortgage Act, an ‘Informal Mortgage’ is defined to mean a written and witnessed undertaking, the clear intention of which is to charge the mortgagor’s land with the repayment of money and includes an equitable mortgage and a mortgage on unregistered customary land. The Act goes on to specifically state that nothing shall operate to prevent a borrower from offering and a lender from accepting a certificate of customary ownership or any other document which may be agreed upon, evidencing a right to an interest in land (under Section 3 (8)).

This is the written law. In practice, however, Financial Institutions are faced with numerous challenges before creating an interest in unregistered land. In summary, these include a lack of a registry to perfect and register the lenders’ interests as compared with ordinary Certificates of Title, fraudulent L.C officials, speculative valuation, consent issues, especially with landlords, dependent relatives and spouses (in a customary context) and lack of clarity on foreclosure procedures for unregistered plots of land.

In an attempt to provide for centralised registration, the Land Act provides for recorders and Area Land Committees. However, these have not been operationalised in all districts in Uganda. Therefore, there is currently no official “registry” at which other lenders can investigate prior or competing registered informal mortgage interests. Financial institutions have resorted to relying on L.C1 Chairpersons to ascertain whether other lenders have already taken the unregistered plots of land as security. Relying on the integrity of L.C. 1 officials has proved to be a credit risk. In addition, valuation of unregistered land is highly speculative compared to surveyed land that is clearly delineated with blueprints, mark stones and GPS coordinates. Financial institutions have been compelled to become creative and rely on neighbours to ascertain the boundaries of the unregistered plots of land. Area land brokers are also consulted to arrive at the economic value. To complicate matters, the Land Act stipulates that consent from spouse(s), children and dependent relatives should be obtained before pledging customary land. Given the potentially polygamous nature of customary marriages, this presents its unique challenges. Lenders have to rely on the integrity of the borrowing customer to disclose all spouses, children and dependents. Furthermore, some unregistered land, especially in Buganda, has absentee landlords to whom ‘busuulu (rent)’ has never been paid. This renders the legal requirement of consent from the landlord to pledge the unregistered land a cumbersome inconvenience, which bars access to credit.

She Walks: Purposeful Strides, Scaling Hills in Heels—and Why Women’s Progress Matters for Africa’s Future

She Walks: Purposeful Strides, Scaling Hills in Heels—and Why Women’s Progress Matters for Africa’s FutureFor all the above situations, the law remains ambiguous and unclear, which has resulted in haphazard credit risk assessments for these types of collateral. This situation is even less clear during foreclosure in the event of default. As a result, Financial Institutions have buffered themselves by charging higher interest rates for loans secured by unregistered land.

As long as this situation persists, the objective of the World Bank and the Bank of Uganda to promote access to credit for the informal business owners who are the backbone of the economy remains a dream on paper. More importantly, Financial institutions will not benefit from the lucrative and untapped potential of informal businesses in Uganda.

There is a solution to this dilemma. With the guidance of experienced legal practitioners on a case-by-case basis, the credit and regulatory risk flowing from these types of credit transactions can be significantly mitigated.

At Dentons Advocates, our Banking and Finance Practice Group is well-equipped to mitigate these risks by drafting watertight informal mortgages and required consents in compliance with the law, advising on underwriting and valuation best practices, and managing the foreclosure of unregistered plots of land.

We are committed to facilitating the exploitation of this potential, which will ultimately spur the development of the country’s banking sector to greater heights.