Citibank Uganda closed the 2024 financial year with a net profit after tax of UGX 71.9 billion, up from UGX 68.3 billion in 2023. This performance secured the bank’s position as the 6th most profitable bank in Uganda, underscoring Citi’s ability to consistently deliver bottom-line growth despite an increasingly competitive and evolving market.

However, beneath this surface of profitability lies a story of gradual decline in core banking operations—a story that has unfolded over the past two years and could define the future of Citi Uganda as its CEO, Sarah Arapta, approaches a decade at the helm in January 2026.

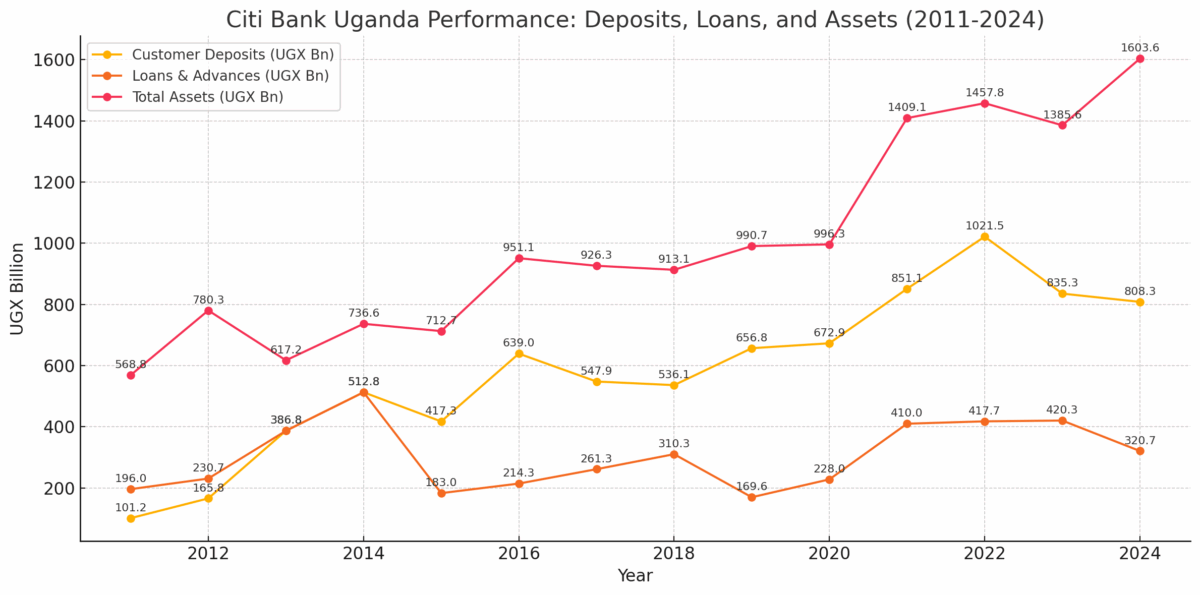

Shrinking Deposits Signal Loss of Market Confidence

A key concern for Citi is its shrinking deposit base, long considered the lifeblood of any commercial bank. In 2022, Citi’s customer deposits peaked at UGX 1.02 trillion, a landmark that propelled the bank into the top 10 banks by deposits—a major achievement reflecting years of steady growth under Arapta’s leadership.

Yet, 2024 marks the second consecutive year of decline, with deposits falling to UGX 808.3 billion—a drop of over 20% from the 2022 peak. This steady erosion has seen Citi slip to 13th position by deposits, down from 10th in 2022, raising serious questions about customer retention, market competitiveness, and product relevance in a banking sector where mid-tier players are aggressively expanding their deposit books through digital products, SME-focused solutions, and customer-centric innovations.

Lending Book Contracts, Weakening Citi’s Core Franchise

The contraction in Citi’s loan book is not a recent trend, but rather a long-standing pattern of stagnation and decline. Since 2014, when Citi’s lending portfolio peaked at UGX 512.8 billion, the bank has struggled to regain similar momentum. The closest Citi has come to that high was in 2023, when loans and advances reached UGX 420.3 billion, still a full 18% below its 2014 peak. In 2024, the situation worsened as Citi’s lending book shrank further to UGX 320.7 billion—a 24% year-on-year drop that underscores the bank’s cautious posture and reluctance to engage robustly in Uganda’s fast-growing credit market.

This persistent underperformance has seen Citi’s ranking in loans and advances steadily slide. From being a mid-tier lender in the early 2010s, Citi has now fallen to 15th position in 2024, down from 13th in 2022, overtaken by more aggressive banks like I&M Bank and Finance Trust Bank. Citi’s shrinking loan book reflects a deliberate strategy to limit credit risk, but it also highlights a lost opportunity in a market where credit growth is a key driver of profitability and market relevance and by extension, deposits mobilisation. Without a bold turnaround, Citi risks further marginalisation in Uganda’s competitive lending landscape.

Asset Growth Masks Structural Fragility

Despite these setbacks, Citi has managed to hold onto its 10th position by total assets, with assets growing to UGX 1.60 trillion in 2024, up from UGX 1.39 trillion in 2023. This growth has been driven largely by a shift towards investment securities, which surged by 40% to UGX 859 billion in 2024, as Citi leaned more heavily on fixed income instruments and interbank placements to bolster its balance sheet.

While this strategy has preserved the bank’s profitability, it has also raised concerns about the quality and sustainability of earnings. Citi’s profitability increasingly rests on treasury activities rather than core lending and deposit mobilisation, a risky position in a volatile economic environment where interest rate fluctuations and market dynamics can quickly erode returns.

Related

Kenya Shilling Holds Firm as Remittances Rise and Markets Show Mixed Signals – Central Bank Report

Kenya Shilling Holds Firm as Remittances Rise and Markets Show Mixed Signals – Central Bank ReportSarah Arapta’s Legacy: Stability, But at What Cost?

Sarah Arapta’s leadership, since assuming the CEO role in January 2016, has been marked by stability, risk discipline, and strong governance. She has steered Citi through regulatory reforms, the COVID-19 pandemic, and the pressures of digital transformation, maintaining the bank’s reputation as a trusted partner for multinational clients. Yet, the last two years have exposed the limits of Citi’s cautious strategy.

While Arapta has ensured the bank remains profitable, with net profit growing from UGX 22.3 billion in 2011 to UGX 71.9 billion in 2024—a CAGR of 8.8% over 13 years—the bank has lost ground in market share in the core and foundational areas.

A Crossroads Moment: Will Citi Reignite Growth or Continue to Shrink?

Citi’s current market position underscores this paradox. It remains the 6th most profitable bank, but its core banking business is shrinking. The bank’s cost-to-income ratio has remained stable, but total operating expenses surged by 21% in 2024 to UGX 24.9 billion, reflecting inflationary pressures and rising operational costs. Meanwhile, trading income declined by over UGX 3.5 billion, highlighting the bank’s growing reliance on investment securities to sustain income streams. The balance sheet has bulked up, but the commercial engine—driven by deposits and lending—has weakened.

Looking at Citi’s longer-term trajectory, the story is clear: a bank that grew aggressively in the early years, with customer deposits rising from UGX 101.2 billion in 2011 to over a trillion shillings by 2022, but has since slowed down, retrenching into safe, low-risk assets. The pace of asset growth has moderated, with the CAGR for total assets declining from 11.3% between 2011 and 2016 to around 7.8% between 2016 and 2024. This deceleration mirrors a strategic conservatism that, while protecting capital, has eroded Citi’s position in a market where agility and customer-centric innovation are driving growth.

The Road Ahead: Can Arapta Engineer a Comeback?

As Sarah Arapta approaches her 10-year milestone at Citi, the stakes could not be higher. Will she marshal a turnaround strategy to restore Citi’s relevance and competitiveness, or will the bank continue its gradual slide toward irrelevance, surviving on a slim but profitable niche? The next 18 months could be pivotal: without decisive action to rebuild the deposit base, reignite lending, and reposition Citi’s value proposition in Uganda’s evolving financial ecosystem, the risk is that Citi could completely slip out of the top 10 league—not just in deposits and lending, but eventually in assets as well.

Citibank Uganda’s story is one of resilience, caution, and survival—but as the market changes, survival alone may not be enough. Arapta’s legacy will hinge on whether she can pivot from stability to strategic growth, ensuring that Citi remains not just profitable but relevant, competitive, and future-ready in Uganda’s dynamic banking landscape.