Most often people do look out for profits or losses in a bank’s results, but there is often a lot of facts behind the figures that go unmentioned. What are some of the key highlights about your 2019 results that are worth celebrating?

It is true that our performance reflects healthy growth in net profit by 33% between 2018 and 2019. However, our financial performance reflects much more – growth, resilience, and sustainable banking. We increased our financial services intermediation as reflected in our credit book growth by 15%. This growth was largely driven by additional credit facilities to small and medium enterprises (SMEs), especially in the Education sector. Our increased focus on responsible financing was demonstrated by our low ratio of non-performing loans to total loans (at 2%). The bank has consistently maintained one of the cleanest credit portfolios in the country. Consequently, our cost of credit risk has thankfully been quite low (at less than 1%). We also invested nearly UGX 1billion in software and hardware capital expenditure to optimize our channels. Consequently, more than 70% of the Bank’s transactions are undertaken on alternative channels such as the Mobile Wallet, internet banking, cards, and agent banking, thus contributing to a more convenient, less costly mode of financial services delivery.

Bank of Africa is known for its focus on SMEs in Education, Education, and Trade-specifically, how did the bank support these sectors in 2019?

Our financial intermediation to the SMEs increased by an amazing 52% in 2019. Our interest was particularly drawn to the Education sector owing to the young demographic in the country that needs to be educated so as to create an intellectual competitive advantage for Uganda. Realising the shortfalls in infrastructure in the Education sector, we invested more than UGX40bn in financing to this sector. This has resulted in an Education sector contribution to our credit portfolio of 10% compared to the industry level of just 2.4%. As part of our social responsibility, we also delivered 25 pro bono (free) business clinics to more than 800 players in the Education sector in 2019, to facilitate financial literacy and better management of these institutions.

We also upheld our consistency in providing easy and affordable trade financing solutions to our clientele. Our guarantee and documentary credit book increased by 46%, one of the highest jumps in the industry. Furthermore, Uganda’s total trade (import and export) volume in 2019 was USD 10bn (according to the Bank of Uganda). We facilitated 8% of this trade through our trade finance offering. This contribution is expected to further increase as we now have one of our affiliates – BMCE Bank of Africa open in Shanghai, China. Our global presence is now in 32 countries on 4 continents. Regionally, our presence covers Kenya, Tanzania, DRC, Rwanda, and Burundi.

SMEs by their very nature are delicate – and are therefore more likely to take the full brunt of COVID-19. How is the bank preparing or how has it prepared to cushion them both during and post-COVID-19 recovery?

The COVID-19 pandemic is a first and foremost a health crisis. This has placed severe pressure on national health systems and resulted into several restrictions that have had severe adverse impacts on economic activity. The United Nations Conference on Trade and Development (UNCTAD) estimates that cross border investment flows will plunge by as much as 30-40% in 2020-2021. The International Labour Organization estimates that the crisis has caused a decline in aggregate working hours of 6.7% in the second quarter of 2020, equivalent to the loss of 195 million full-time jobs. The IMF has estimates Uganda’s 2020 GDP to decline from 6.5% to 3.3%.

The combination of the health crisis and an abrupt economic slowdown has been devastating on businesses. On the supply side, businesses are facing movement restrictions on workers or a constricted supply of inputs due to supply chain disruptions. On the demand side, businesses are facing weak consumer demand and confidence, and government-imposed restrictions have cut off access to customers.

SMEs have been particularly hit hard because they are overrepresented in sectors that have faced the brunt of crisis such as transport, manufacturing, construction, trade, tourism, hospitality, real estate, and professional and personal services. They have fewer assets and less cash while finding it more difficult to access credit, resulting in liquidity crunches. They also hardly invest in technologies required to continue operations during a lockdown such as offsite working and videoconferencing. Consequently, the Organisation for Economic Co-operation and Development (OECD) has predicted that more than 50% of the SMEs will not survive the next three to six months.

However, as SMEs represent more than 70% of employment, Uganda’s economy will depend on them to power its recovery process. Bank of Africa has therefore undertaken the following measures to support them:

Credit relief: All businesses facing liquidity crunches are encouraged by the Bank to apply for credit relief measures which include moratoriums on debt repayments of principal, interest, or both. All borrowing clients can apply between now and 31 March 2021. No costs are attached to these measures and such relief measures shall not affect the credit rating of borrowers with rating agencies.

Trade finance: Cash strapped businesses are encouraged to use our less costly, less risky, trade finance mechanisms that preserve liquidity such as letters of credit, guarantees, documentary collections, in place of payment on account. We are in position to further explain how this works to any business that is interested in this efficient and safe method of doing business.

Mobile banking: Businesses facing restrictions are encouraged to sign up for our mobile banking platforms – the Mobile Wallet, and Internet Banking platforms. Businesses should then find it easier to transact – receive and send funds, update business records at the convenience of their homes. In addition, existing and potential clients can arrange for videoconferences with us using their phones to facilitate better understanding of their needs.

Additional credit: We are considering granting credit to sectors that have been positively impacted by this crisis to support their investment and working capital requirements. For example, businesses that are involved in the production of personal protective equipment, food, cleaning, health facilities, and other essential goods and services are encouraged to speak to us.

Ruparelia Group Wins Key Entebbe Land Case, Clearing Path for the New Mega Speke Resort and Convention Centre, Entebbe

Ruparelia Group Wins Key Entebbe Land Case, Clearing Path for the New Mega Speke Resort and Convention Centre, EntebbeEducation support: Education institutions that may be required to implement additional health measures in order to operate as advised by the Ministry of Health are also encouraged to speak with us to assess their needs and how we can support them comply with such requirements.

Anyone interested in discussing any of these measures can contact us at toll free line 0800100140, WhatsApp line 0717800508, or email: feedback@boauganda.com.

In 2020, the Bank celebrates 35 years of existence in Uganda. Looking back, what are some of the proud moments that you are celebrating?

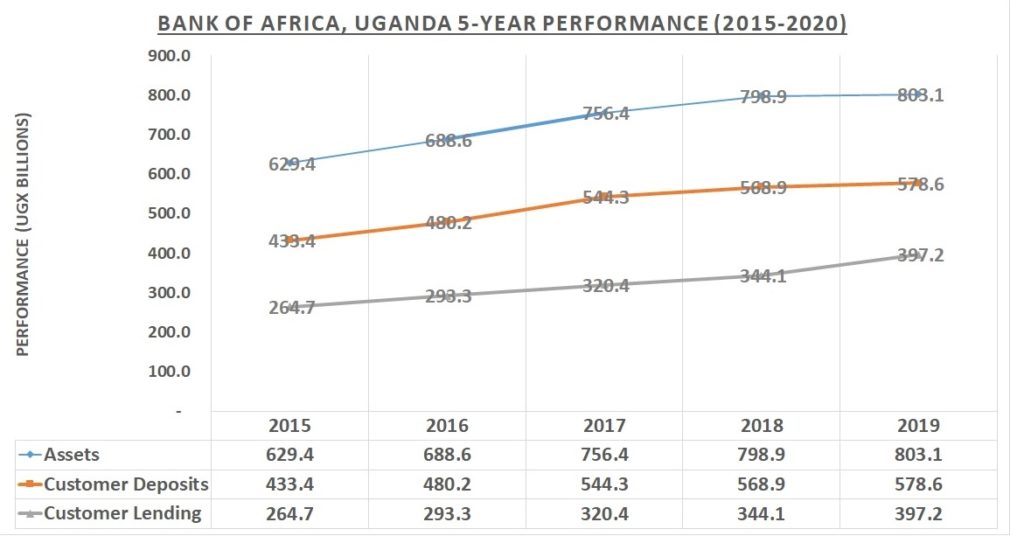

Bank of Africa started its operations in Uganda in 1985 as a small local bank owned by Ugandans. We are proud to have enriched the Bank’s DNA – attracting Belgian, Dutch, French, Moroccan investment while retaining our local roots. From an asset base of just UGX 10bn when we were granted a commercial banking license to now more than UGX800bn is a great achievement. Over the last three decades, we have delivered a cumulative annual growth rate of 20% in customer deposits, loans and advances, total assets, and shareholder equity. Only a few companies in Uganda, and indeed in the world, have achieved this feat. We started our operations with just 3 branches and we now have 34 branches supported by multiple other service delivery channels. We are also proud to have been the very first commercial bank to introduce a bank-led Mobile Wallet model in Uganda. Despite its longevity, our Mobile Wallet still offers one of the most compelling propositions to the public. We are also proud that we support more than 450 families through our employees from less than 80 three decades ago. We are also proud to be in the distinguished group of the top 100 tax payers in Uganda consistently for each of the last 10 years, a testament to our dedication to the development of our economy.

The bank, will itself certainly be affected by the COVID-19 pandemic itself. Are you confident that the 2019 results put you in a good place to withstand the shock on the Bank itself?

Definitely. By any measure of the CAMELS ratings model used by bank regulators, which assesses a bank’s performance with respect to capital adequacy, asset quality, management, earnings, liquidity, and market sensitivity, Bank of Africa stands strong and is way above the recommended minimums to ensure stability and going concern. The investments in technology that we have been making over the years have borne fruit and such technology is increasingly becoming essential in the way we operate, and communicate with employees, and with customers.

We have also already made investments in personal protective equipment and sanitization infrastructure that will allow for the protection of health of our customers and employees. Furthermore, we are a subsidiary of a strong banking group – BMCE Bank of Africa which boasts of a total asset base of more than USD 32 billion (which is in fact the size of Uganda’s economy) and shareholders’ equity of nearly USD 3 billion. This should provide assurance to the public that we have strong backing and we can withstand any local shock to Uganda.

Lastly, in your view as a key player in Uganda’s economy, what would you think are some of the key interventions that need to be taken by policymakers to jumpstart the post-COVID-19 economy?

Like any other country, Uganda’s economy will be adversely impacted as indicated earlier above. We commend the Government for having already taken various measures to provide relief to the public while preserving economic survival. Some additional interventions that may be of interest to policy makers include the following:

Information flow: The effective aggregation of collective views of business players on how best to revive the economy is critical to build consensus and offer well-informed policy recommendations. Government needs to leverage on the networks of the business community through business support organisations not only to gather, but to provide timely information about business continuity, teleworking, crisis leadership, and cash flow management. A good ecosystem of business support players should combine the public, quasi-autonomous, and the private sector organisations from a broad range of sectors to develop a robust country-wide response to this crisis that has the buy-in of all.

Trade barriers: Now, more than ever, policy makers in the East African Community need to empower businesses by reducing tariff and non-tariff trade barriers, and trade restrictions, to promote regional trade in response to global protectionist tendencies that have only been exacerbated by this crisis. The critical barriers to prioritise can be determined through the information flow mechanisms discussed above.

The digital economy: Business recovery will be quicker if policy makers enable the thriving of the digital economy – this implies making digital services cheaper, reliable, and easier to access across the country. This crisis has created an opportunity to shift efforts towards supporting digital innovations by Ugandans that will support business recovery without increasing the risk of further spreading the coronavirus. Furthermore, policy makers can spur the digitalization of trade documents and procedures in collaboration with the private sector – digital identification and clearance processes based on electronic documents or scanned versions of documents, e-certifications, and strengthening the legal basis of such kinds of documentations.

Access to trade finance: Declines in inter-firm trade credit which is now expected, can have drastic effects on economic growth, even faster than reduced credit from financial institutions. Several countries have announced new or expanded programmes to provide financial support to trade players in need of trade credit such as national exporters, vulnerable business groups (such as the women and youths), and SMEs. Other measures to consider could include setting up reinsurance mechanisms for trade credit insurers, enforcement of payment discipline by larger firms through better contract protection, and expedition of payments in the public procurement system.