Diamond Trust Bank Uganda Limited (DTB Uganda) reported a mixed financial performance for the year ended December 31, 2024, marking a significant inflexion point in its decade-plus-long growth story. After more than ten years of uninterrupted growth, the bank’s key performance metrics dipped in 2024, coinciding with the leadership transition that saw Godfrey Sebaana take office as the new Managing Director and CEO in April 2024.

Customer Deposits: A Sharp Reversal from a Decade of Steady Growth

DTB Uganda’s customer deposits declined by 5.1% to UGX 2.094 trillion in 2024, down from UGX 2.207 trillion in 2023. This marks the first annual decline in the bank’s deposit base in over a decade and represents a sharp deviation from its long-standing growth trajectory. Between 2011 and 2023, DTB Uganda had expanded its deposits at an estimated Compound Annual Growth Rate (CAGR) of 17.23%, growing from an estimated UGX 327.5 billion in 2011 to UGX 2.207 trillion in 2023. The 2024 performance, therefore, signals a significant reversal of momentum—a clear break in what had been a consistent upward trend for more than ten years.

| Year | Customer Deposits (UGX Billion) | YoY Growth (%) |

| 2011 | 327.5 | – |

| 2012 | 529.4 | 61.6% |

| 2013 | 633.7 | 19.7% |

| 2014 | 849.1 | 34.0% |

| 2015 | 1,048.4 | 23.5% |

| 2016 | 1,102.3 | 5.1% |

| 2017 | 1,168.6 | 6.0% |

| 2018 | 1,150.2 | -1.6% |

| 2019 | 1,321.2 | 14.8% |

| 2020 | 1,283.6 | -2.8% |

| 2021 | 1,500.6 | 17.0% |

| 2022 | 1,876.2 | 25.0% |

| 2023 | 2,207.3 | 17.7% |

| 2024 | 2,094.0 | -5.1% |

The UGX 113.3 billion decline in deposits in 2024 not only reduced the bank’s absolute funding base but also saw its market share in deposits shrink from 6.6% in 2023 to 5.9% in 2024. This loss of ground in a highly competitive banking landscape pushed DTB Uganda down from 7th to 8th place in the industry rankings for customer deposits. The shift underscores the intense competition for customer funds in Uganda’s banking sector, where market leaders like Stanbic, Centenary, and Absa continue to strengthen their hold, while new challengers aggressively target deposit growth.

The decline in deposits also carries deeper strategic implications given that deposits are the lifeblood of every bank’s operations—fueling lending, investment, and liquidity positions. A contraction in deposits not only limits the bank’s ability to grow its loan book and income streams but also raises concerns about its customer retention, market positioning, and overall competitiveness.

Modest Gains in Lending Growth

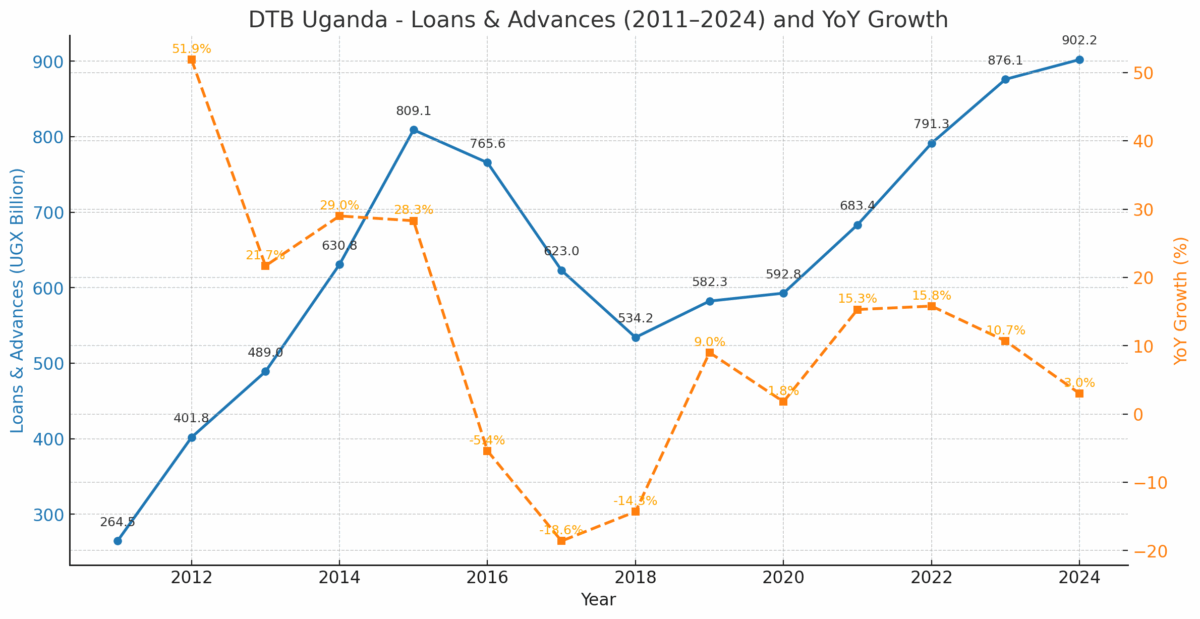

DTB Uganda’s loans and advances also grew modestly by 3.0% in 2024, rising from UGX 876.1 billion in 2023 to UGX 902.2 billion. While this increase represents continued expansion of the bank’s credit portfolio, it falls short of the bank’s historical growth trend. Between 2011 and 2023, DTB Uganda had grown its loan book at an estimated Compound Annual Growth Rate (CAGR) of 10.5%, nearly triple the 2024 rate. The decade-long average had seen the bank’s loans and advances rise from approximately UGX 264.5 billion in 2011 to UGX 876.1 billion by 2023, fueled by consistent deposit growth and an aggressive push into the SME and retail markets.

The slowdown in lending growth during 2024 is closely tied to the contraction in the bank’s customer deposit base, given that deposits are the primary source of funding for loans in a commercial bank’s model.

The bank dropped from the 9th to the 10th position in loan market rankings, but this static position reflects a cautious lending stance, likely influenced by both liquidity pressures and a recalibrated risk appetite under new leadership.

The 2024 slowdown in lending highlights a critical risk: without sustained deposit growth, DTB Uganda’s ability to finance loan expansion remains constrained.

Assets Contraction Limits Income Growth Potential

DTB Uganda’s total assets declined by 4.8% in 2024, falling from UGX 3.008 trillion in 2023 to UGX 2.863 trillion. This decline, equivalent to UGX 145.0 billion, marks the first contraction in the bank’s balance sheet after more than a decade of continuous growth. The reduction was primarily driven by a 32.2% decrease in marketable (trading) securities, which fell from UGX 1.352 trillion to UGX 917.3 billion. Additionally, the bank saw a 43.3% drop in balances due from parent/group companies and a 5.1% decline in customer deposits, further contributing to the asset shrinkage.

While loans and advances grew modestly by 3.0%, from UGX 876.1 billion to UGX 902.2 billion, this increase was insufficient to offset the overall asset contraction, reflecting liquidity pressures linked to the deposit decline.

This shrinking asset base directly constrained the bank’s ability to grow income, particularly from interest-earning assets like securities and loans. Although DTB Uganda reported an 8% growth in total income in 2024, from UGX 307.7 billion to UGX 332.1 billion, this was significantly below the bank’s decade-long ncome growth trajectory.

Between 2015 and 2023, DTB Uganda had achieved an estimated Compound Annual Growth Rate (CAGR) of 9.5% in total income, expanding from approximately UGX 160.1 billion in 2015 to UGX 307.7 billion in 2023. This relatively strong was largely underpinned by the steady expansion of the bank’s asset base, which grew at a compound annual growth rate (CAGR) of 18.4% during the same period. The relationship is clear: as assets grew, so did income, driven by increased lending, investment in securities, and diversified revenue streams.

Profitability Dips for DTB Uganda in 2024, Ending a Decade of Steady Gains

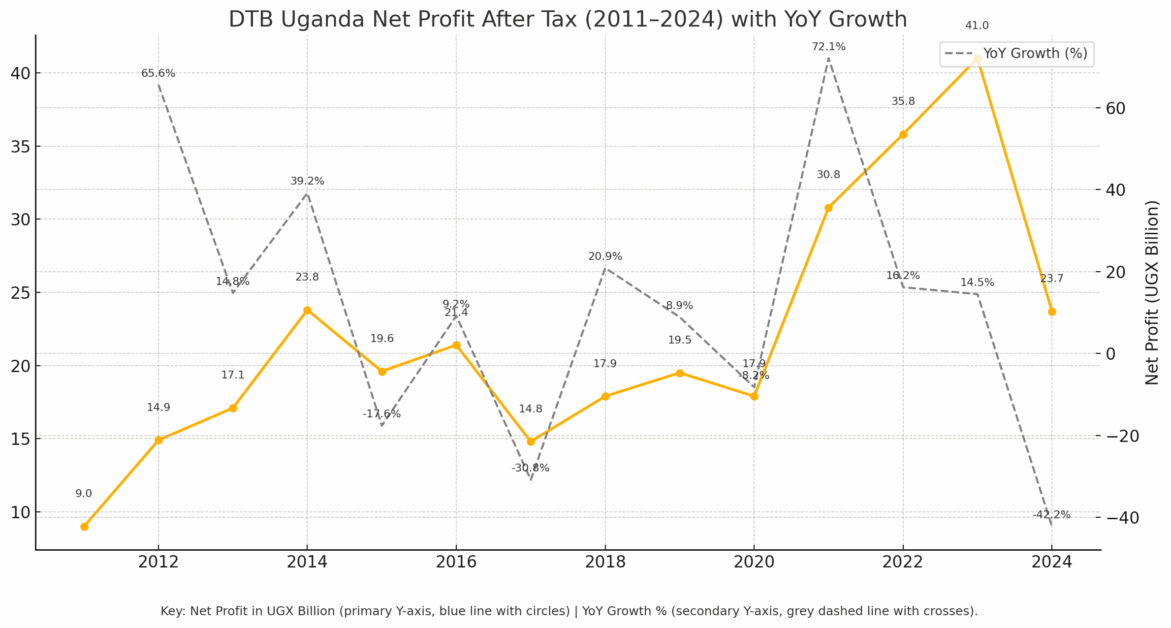

DTB Uganda’s profitability declined sharply in 2024, marking a significant departure from the consistent growth the bank had recorded over the past decade. Net profit after tax fell by 42.2%, dropping from UGX 41.0 billion in 2023 to UGX 23.7 billion in 2024. This decline reflects the combined impact of higher operating expenses, increased loan loss provisions, and a weakened balance sheet, as the bank’s customer deposits and total assets contracted during the year.

Between 2011 and 2023, DTB Uganda’s net profit grew at an estimated Compound Annual Growth Rate (CAGR) of 13.5%, increasing from approximately UGX 9.0 billion in 2011 to UGX 41.0 billion in 2023. This strong performance was driven by a steadily expanding asset base, consistent growth in lending and investments, and disciplined cost management. The growth momentum was particularly robust in the post-2018 recovery period, when the bank overcame earlier asset quality challenges to deliver a series of annual profit increases.

However, 2024 marked a turning point. Operating expenses rose by 10.5% to UGX 140.2 billion, up from UGX 126.9 billion in 2023, reflecting the costs of strategic investments in technology, digital infrastructure, staff development, and branch networks. Impairment losses on loans and advances increased to UGX 29.7 billion from UGX 7.7 billion the previous year, indicating a rise in credit risk. The decline in customer deposits by 5.1% to UGX 2.094 trillion further limited the bank’s capacity to fund new lending and investments, while total assets contracted by 4.8%, falling from UGX 3.006 trillion in 2023 to UGX 2.863 trillion. This reduction in the income-generating asset base placed additional strain on profitability.

Strong Foundation and Future Outlook

Despite the notable slowdown in 2024, DTB Uganda retains a fundamentally strong position, with solid capital buffers, a large customer base, a growing loan book, and one of the most expansive branch networks in the country. It still ranks within Uganda’s top 10 banks across most major indicators—customer deposits, loans, total assets, and income—but now hovers closer to the bottom tier of that elite league.

The top 10 is an unforgiving space, dominated by aggressive, well-capitalized banks like Stanbic, Centenary, Absa, Equity, and dfcu. Competition is fierce, and margins for error are narrow. Any sustained underperformance could see DTB edged out of the top tier. For incoming CEO Godfrey Ssebana, this reality raises the stakes. He must begin firing from all throttles—mobilizing deposits, reigniting lending, retooling customer experience, and accelerating the digital transformation agenda—to prevent slippage and reposition DTB firmly in the competitive vanguard.

On capital adequacy, DTB Uganda remains comfortably above regulatory thresholds. As of December 2024, the Core Capital to Risk Weighted Assets (RWA) stood at 21.2%, and the Total Qualifying Capital to RWA at 21.9%, only slightly down from 24.0% and 24.7% in 2023, respectively. The bank’s qualifying capital closed at UGX 257.1 billion, providing adequate headroom for risk absorption, strategic investment, and credit expansion.

Chairman Azim H. A. Kassam was keen to frame 2024 as a necessary recalibration: “These investments are already showing signs of bearing real fruit… [they] position us very well to seize future opportunities and to navigate the changing financial landscape with resilience and agility.” His message suggests the board’s long view is still intact—that the temporary dip in performance is a price worth paying for repositioning the bank for long-term relevance.

CEO Godfrey Ssebana, only months into his tenure, is already making it clear that he is aware of the magnitude of the task ahead. He remains optimistic, pointing to progress in digital transformation and customer reach: “The success achieved across our business in 2024, which includes growth in income, our customer base, customer advances, deepening of our digital transformation agenda and journey towards achieving sustainability excellence, is a testament to the robustness of the three strategic pillars that underpin our business growth strategy.”

He also reaffirmed DTB Uganda’s commitment to sustainable banking and ESG alignment, noting that the bank is preparing to meet global standards under the new IFRS S1 and S2 climate and sustainability reporting frameworks. This forward-looking agenda—anchored in customer-centricity, innovation, and governance—will be instrumental in securing investor confidence and stakeholder support going forward.

The bank’s immediate priority, however, must be to reverse the contraction in customer deposits and total assets, and restore profitability momentum. With most top-tier banks aggressively growing both their balance sheets and digital footprints, DTB cannot afford to remain in transition mode for long. The coming year will be a critical proving ground—not only for Ssebana’s leadership but also for the strategic bets being made today to secure DTB Uganda’s place in the upper echelon of the banking industry.