For much of Uganda’s post-independence history, NIC Holdings occupied a privileged position in the country’s insurance landscape.

Established in 1964 as National Insurance Corporation, NIC was once the dominant underwriter by virtue of scale, state backing, and first-mover advantage.

That legacy, however, has not translated into market leadership for more than two decades.

Today, despite being one of Uganda’s oldest, if not the oldest, insurance institutions, NIC operates largely as a mid-tier player in general insurance and remains at the bottom of the rankings in life insurance, with market shares that have struggled to break beyond low single digits.

This long erosion of competitive position now forms the backdrop against which Elias Edu must deliver results.

Edu formally assumed the role of managing director of NIC Holdings on May 1, 2025, having previously served within the group in senior legal and executive capacities.

His elevation came at a moment when the group was showing signs of operational stability, but still facing deep structural and capital constraints.

A legacy brand without a legacy premium

In general insurance, NIC has spent years competing in the middle of the market, without the scale advantages of the top-tier insurers or the cost flexibility of smaller niche players.

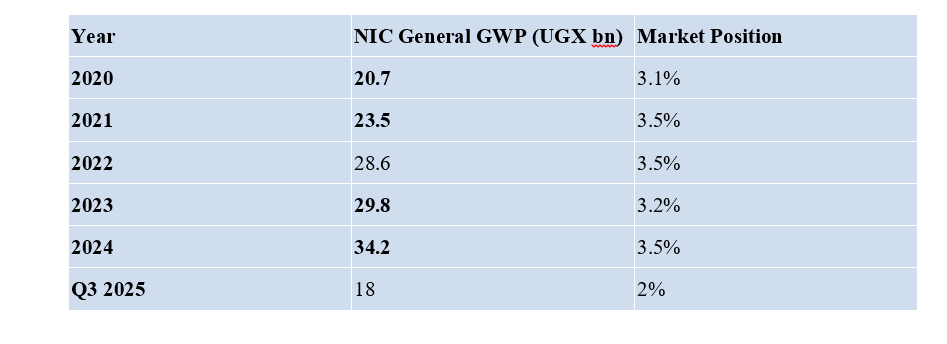

NIC General Insurance’s Gross Written Premiums (GWP) grew from UGX 20.7 billion in 2020 to UGX 34.2 billion in 2024, lifting market share to about 3.5% at its recent peak.

Yet, this position has remained fragile. Market share slipped to 3.2% in 2023, recovered in 2024, and early indicators from Q3 2025 show GWP of UGX 18 billion, translating to an estimated 2% market share, compared to UGX 21.7 billion and 2.7% in the same period of 2024.

The volatility underscores how NIC’s non-life business, while capable of growth, has struggled to compound gains consistently.

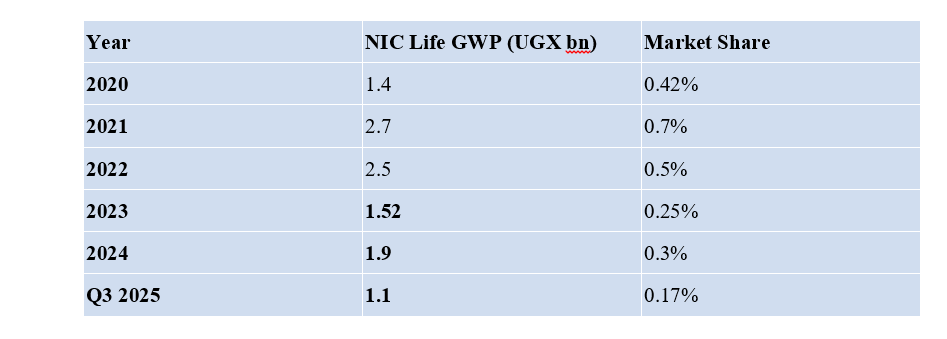

The picture is more challenging in life insurance. NIC Life Assurance has, for much of the past decade, operated at the bottom of the market.

After reaching a high point of UGX 2.7 billion in GWP (0.7% market share) in 2021, premiums declined sharply to UGX 1.52 billion in 2023.

A modest recovery to UGX 1.9 billion in 2024 still left NIC Life with just 0.3% market share.

By Q3 2025, premiums stood at UGX 1.1 billion, with market share slipping further to 0.17%.

The result is a group whose historical brand strength no longer confers competitive advantage, particularly in the life segment where scale, distribution depth, and long-term savings products increasingly define success.

Operational improvement, structural limits

At the group level, NIC’s recent financials reflect measured operational recovery, but also highlight the limits of that progress.

Tax on Used Clothes to Increase to 30%

Tax on Used Clothes to Increase to 30%In the first half of 2025, insurance revenue rose 4.3% to UGX 16.5 billion, while the insurance service result returned to a profit of UGX 286 million.

Total assets edged up to UGX 92.5 billion, from UGX 91.4 billion at the end of 2024.

However, liabilities increased to UGX 52 billion, leading to a 3% decline in shareholders’ equity to UGX 40.5 billion.

The group still posted a net loss of UGX 1.06 billion, driven largely by a UGX 2.7 billion one-off loss on disposal of an investment property, pushing earnings per share to negative UGX 0.46, from UGX 0.95 a year earlier.

Gross Written Premium (Non-life)

Gross Written Premium (Life)

Cash flows were stronger, however. Net operating cash inflows of UGX 6.9 billion and investing inflows of UGX 7.9 billion lifted cash balances to UGX 10.6 billion by June 2025, up from UGX 1.1 billion at the start of the year.

Even so, the board opted not to declare an interim dividend, extending a period of limited shareholder returns.

The capital question that won’t go away

Hovering over Edu’s tenure is the delayed rights issue, first approved by shareholders in 2022 and repeatedly postponed.

The capital raise is widely viewed as essential to strengthening NIC’s balance sheet and enabling strategic repositioning.

While the majority shareholder has deposited UGX 1.915 billion toward future participation, the prolonged delay has weighed on investor sentiment.

NIC shares remain thinly traded, with average monthly liquidity of about UGX 2.41 million, reflecting sustained market caution following profit volatility and accounting disruptions under IFRS 17.

Why Edu’s task is unusually difficult

Edu inherited a group that is older than most of its competitors, yet no longer enjoys the advantages of incumbency.

NIC is neither a scale leader nor a niche disruptor. Its non-life business shows potential but remains exposed to swings in underwriting cycles, while its life arm has yet to achieve the critical mass needed to drive long-term value.

Four years after joining the top leadership and just months into his formal tenure as managing director of the holding company, Edu faces a defining test: can NIC convert operational stability into durable profitability, restore capital momentum, and arrest its long slide down the industry hierarchy?

Until those questions are answered, NIC’s long history will remain just that, a legacy, rather than a source of competitive strength, and its CEO will remain firmly in the hot seat.